Working Capital for Seasonal Business: A Blueprint for Year-Round Growth in 2026

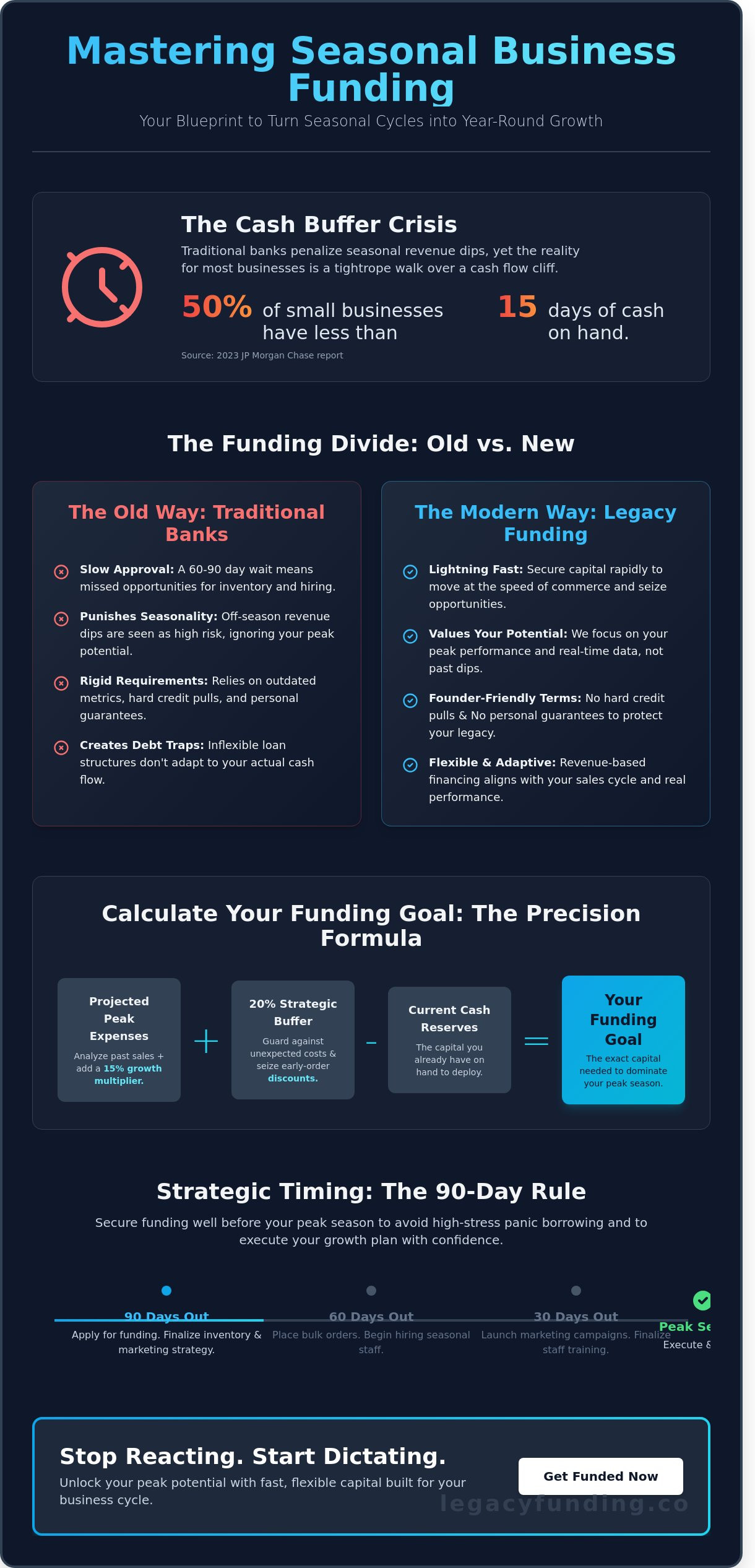

Traditional banks treat your seasonal revenue dips like a terminal illness, yet a 2023 JP Morgan Chase report reveals that 50% of small businesses operate with less than 15 days of cash buffer. You shouldn't be penalized for a business model that thrives on timing. You already understand the grit required to survive a six month drought. Securing the right working capital for seasonal business is the difference between a record breaking peak and a quiet closure. To scale in 2026, you need a financial ally that values your peak potential over your off-season floor.

This article is your blueprint to master seasonal cash flow and unlock your full trajectory. We will show you how to leverage flexible credit lines to accelerate your growth and dominate your market. You will learn to identify the exact moment to inject capital so you can stop reacting to the calendar and start dictating your results. We are diving into how to Get Funded fast, maintain your legacy, and secure your future with no personal guarantee and no hard credit pull. It's time to turn your seasonal cycle into a year-round engine for wealth.

Key Takeaways

- Bridge the gap between off-season expenses and peak revenue by mastering the "Inventory Ramp" strategy.

- Learn to project your off-season burn rate and secure the ideal working capital for seasonal business to avoid leaving money on the table.

- Align your capital with your sales cycle using flexible tools like revenue-based financing that adjust to your real-time performance.

- Apply the "90-Day Rule" to lock in funding well before your peak season begins, ensuring you never resort to high-stress panic borrowing.

- Unlock rapid scaling with a tech-forward partner that offers funding with no hard credit pulls and no personal guarantees.

Understanding the Seasonal Cash Flow Trap

Working capital for seasonal business is the liquidity bridge between your quiet months and your peak performance. It represents the cash flow required to cover operational expenses before your primary revenue stream activates. Working capital management ensures you don't stall out during the "Inventory Ramp." This is the critical period where your costs for stock, labor, and marketing peak just as your cash reserves hit their lowest point. Stop viewing capital as a last-resort survival tactic. Treat it as a strategic tool to unlock your next level of scale. Secure your inventory. Hire your team. Accelerate your growth.

Traditional banks often pull back when they see revenue dips. They view your off-season as a risk rather than a cycle. This creates a dangerous paradox. You need funds to prepare for your busiest months, but the lack of current revenue makes you look "unlendable" to legacy institutions. Legacy Funding changes this dynamic. We focus on your potential and your peak performance. We provide the blueprint to turn your seasonal surge into a year-round advantage. Get Funded and stop letting the calendar dictate your success.

The Anatomy of a Seasonal Revenue Cycle

Every seasonal business moves through three distinct phases. The Preparation phase requires heavy investment in inventory and staffing. The Peak phase is where you capture revenue and maximize margins. Finally, the Preservation phase involves managing the surplus to survive the lean months. Common drain points like off-season payroll and Q1 marketing can deplete your reserves quickly. If you lack capital during the Prep phase, you limit your Peak potential. You can't sell inventory you don't have. You can't serve customers with a skeleton crew. Use capital to bridge these gaps and maintain momentum.

Why Traditional Lending Fails Seasonal SMBs

Traditional lenders rely on outdated metrics that punish seasonal volatility. They often fall into the Credit Score Trap during your low-revenue months, ignoring the 300% revenue spike you expect in July or December. Approval times at big banks often stretch to 60 or 90 days. In a fast-moving industry, a 90-day wait is a death sentence. You need a partner that moves at the speed of commerce. Revenue-based models offer the flexibility that rigid bank loans lack. We prioritize your actual business health. Our process requires No Personal Guarantee and No Hard Credit Pull. This is the modern way to Get Funded.

Calculating Your Seasonal Working Capital Needs

Precision scales businesses. Guesswork kills them. To secure the right working capital for seasonal business, you must look beyond your bank balance. You need to master your cash flow rhythm. Stop obsessing over a static credit score. Traditional lenders look at where you were two years ago; modern growth requires looking at where your revenue will be in 90 days. Focus on your real-time data to build a bulletproof funding strategy.

Inventory and Staffing Projections

Data from 2025 shows that 42% of seasonal retailers lost revenue due to stockouts. Don't repeat their mistakes. Analyze your peak sales volume from the last two years and add a growth multiplier of at least 15% to account for 2026 demand shifts. Factor in your team early. Hiring and training seasonal staff 45 days before the rush ensures peak efficiency. Burn Rate is the total monthly cash outflow during non-peak months. Know this number to the penny. It dictates how long your runway lasts before the first peak-season dollar hits your account.

The Buffer Factor: Preparing for the Unexpected

The math of entrepreneurship is rarely linear. Always add a 20% cushion to your capital request. This isn't fluff; it's a strategic defense mechanism. A $4,000 equipment failure or a 12% spike in logistics costs can derail a lean season. Use this extra leverage to your advantage. Many suppliers offer 5% to 10% discounts for bulk orders placed three months early. While traditional routes like SBA 7(a) loans provide long-term structure, they often lack the speed needed to capture these immediate windows of opportunity. Accessing fast capital allows you to buy low and sell high when your competitors are still waiting on paperwork.

Calculate your target with this blueprint: (Projected Peak Expenses + 20% Buffer) - (Current Cash Reserves) = Your Funding Goal. This formula ensures you aren't just surviving the off-season, but actively positioning yourself to dominate the peak. If you're ready to stop waiting and start scaling, it's time to get funded and secure your market share. We prioritize your cash flow metrics over outdated credit metrics to accelerate your trajectory.

Comparing Funding Options: Traditional vs. Modern Capital

Traditional banks operate on a 20th-century mindset. They demand fixed monthly payments regardless of whether your storefront is packed or empty. This rigidity kills growth. Modern capital solutions offer the agility required for a working capital for seasonal business strategy in 2026. While an SBA 7(a) loan offers low rates for long-term infrastructure, the 60 to 90 day approval window is too slow for immediate inventory needs. You need speed. You need flexibility. Get Funded on your own terms.

Revenue-Based Financing: The Seasonal Ally

Revenue-based financing (RBF) is the gold standard for working capital for seasonal business because it mirrors your actual cash flow. Instead of a fixed dollar amount, your repayment is a small percentage of daily or weekly sales. If a summer storm keeps customers away, your payment drops automatically. This prevents the "fixed payment" stress that causes 82% of small business failures due to cash flow mismanagement. You don't just survive the slow months; you protect your peace of mind.

Legacy Funding prioritizes your protection. Our modern RBF products feature a No Personal Guarantee structure and No Hard Credit Pull during the initial phase. This keeps your personal assets safe while you scale. You get the capital you need based on your performance, not just a static credit score. Unlock your potential without the weight of traditional debt. Accelerate your expansion by leveraging your future success today.

Business Lines of Credit for Recurring Needs

A line of credit is your financial safety net. It follows a "Draw and Repay" model that allows you to access funds exactly when you need them. You only pay interest on the capital you actually use. This is the ultimate tool for managing ongoing seasonal cycles without taking on unnecessary debt.

- Proactive Setup: Secure your line at least 90 days before your peak season starts to ensure liquidity.

- Flexible Terms: Many modern lines offer interest-only periods for the first 6 months to keep costs low during ramp-up.

- Instant Access: Once your line is established, funds move to your account in under 24 hours.

Contrast this with Merchant Cash Advances (MCAs). MCAs provide immediate liquidity by purchasing a portion of your future credit card receipts. They are built for speed; approvals often happen in 4 hours or less. Use MCAs for short-term spikes and RBF for sustained seasonal shifts. Don't let red tape hold you back. Get Funded and build your legacy.

Strategic Timing: When to Secure Your Seasonal Capital

Timing determines your trajectory. Most founders wait until the peak hits to look for liquidity. This is panic borrowing. It leads to high costs, rushed decisions, and missed opportunities. Follow the 90-Day Rule. Secure your working capital for seasonal business three months before your peak demand arrives. This window allows you to deploy funds strategically rather than desperately. You need to be the predator in your market, not the prey.

Legacy Funding eliminates the friction of traditional lending. While banks stall for weeks with endless paperwork, modern alternative lenders provide capital within 24 to 48 hours. This speed allows you to pivot instantly. You can seize inventory deals or launch aggressive ad campaigns while your competition waits for a loan officer to return their call. Speed is your greatest competitive advantage in 2026.

The Pre-Peak Push

Early capital is your most powerful lever. Use it to lock in bulk inventory pricing before seasonal inflation hits. A 2023 U.S. Bank study found that 82% of small businesses fail because of cash flow mismanagement. Avoid this trap by securing your working capital for seasonal business early. Use your funding to "buy the off-season." Purchase your ad placements when they are cheaper. Build your brand awareness while your competitors are silent. Proactive funding is an investment; reactive funding is a cost.

When you have the capital ready, you reduce operational stress. You stop worrying about payroll and start focusing on execution. You focus on growth. You focus on your legacy. Leverage these three advantages of early funding:

- Negotiation Power: Cash in hand allows you to demand better terms from suppliers.

- Market Dominance: Outspend competitors on marketing before the season peaks.

- Operational Stability: Hire and train your seasonal staff before the rush begins.

Managing the Post-Peak Taper

The end of the season shouldn't mean the end of your momentum. Use your remaining capital to retain your top-tier staff. Replacing a trained employee costs 33% of their annual salary according to data from Employee Benefit News. Keep your core team intact through the quiet months to ensure a seamless transition into the next cycle.

Plan your exit strategy for the season with precision. Consolidate any high-interest seasonal tools into a single, manageable credit line. This keeps your debt-to-income ratio healthy and prepares your balance sheet for the next round of expansion. Maintain a cash reserve that covers at least 90 days of fixed costs. This ensures your cash flow remains healthy even when the revenue slows down. Secure your future now and Get Funded to accelerate your business growth today.

Unlock Your Growth with Legacy Funding Advisors

Traditional banks move at a glacial pace. Your seasonal peak won't wait for a committee to review your file. Legacy Funding Advisors understands that speed is your primary competitive advantage. We provide the capital you need to scale without the friction that kills momentum. Our signature approach includes a No Hard Credit Pull policy and a No Personal Guarantee requirement. This protects your personal assets and your credit score while you focus on expansion. We deliver funding in 24 to 48 hours. This speed ensures you never miss a narrow market window. We act as your high-level financial consultant. We help you transform a seasonal surge into a generational business legacy that stands the test of time.

The Legacy Funding Advantage

We prioritize your business's health over arbitrary credit scores. Our team evaluates your revenue and cash flow to determine your capacity for growth. This is the modern, data-driven way to secure working capital for seasonal business needs. We offer flexible products like Revenue-Based Financing and Merchant Cash Advances (MCAs) that align with your actual sales volume. Our digital application is built for founders who don't have hours to waste on paperwork. We focus on your growth metrics rather than just debt obligations. This allows you to:

- Access capital based on performance, not just credit history.

- Utilize scalable capital that expands alongside your peak revenue.

- Navigate a frictionless digital interface designed for 24/7 accessibility.

Get Funded: Your Next Steps

Success in 2026 requires a proactive stance. You shouldn't wait for your cash reserves to hit zero before seeking leverage. Our three-step process is designed to get you from application to deposit in record time. First, you complete our brief online form in under five minutes. Second, you connect your business accounts for a rapid revenue review. Third, you receive your offer and get funded. It's that simple. We don't just provide a transaction; we provide a partnership. Traditional lenders see a balance sheet; we see a founder's vision. By removing the red tape, we allow you to leverage your current success to fund your future dominance. This is about more than surviving the off-season. It's about building a foundation that lasts for decades. Unlock your business blueprint today. Bridge the gap between seasons with confidence.

Ready to accelerate? Get Funded with Legacy Funding Advisors

Secure Your 2026 Competitive Advantage

Don't let the 2026 off-season dictate your business trajectory. Success requires a proactive blueprint that bridges the gap between peak demand and quiet quarters. You've learned how to calculate your precise needs and why traditional banks often fail the modern founder. Securing the right working capital for seasonal business transforms a temporary cash flow trap into a permanent growth engine. Timing your capital injection ensures you're never caught off guard when inventory demands or staffing needs surge.

Legacy Funding provides the high-level leverage you need without the friction of outdated lending. We deliver funding in as little as 24-48 hours to keep your momentum high. Our process features No Hard Credit Pull and No Personal Guarantee options to protect your personal financial freedom. You'll benefit from flexible revenue-based repayment models that align with your actual sales volume. Stop reacting to the seasons and start commanding them.

Unlock your seasonal growth blueprint and Get Funded today

Your legacy starts with the right partner and the right capital at the right time. We're ready to help you scale.

Frequently Asked Questions

What is the best type of working capital for a seasonal business?

A business line of credit is the most effective tool for managing working capital for seasonal business because it provides on-demand liquidity. The 2023 Federal Reserve Small Business Credit Survey notes that 56% of small firms rely on these lines to smooth out cash flow. You only pay for what you use, which keeps your overhead low during the quiet months. Get Funded today to bridge your next gap.

Can I get a business loan if my revenue is currently low due to the off-season?

You can secure funding during the off-season by showcasing your peak performance through historical bank statements rather than just your current month. Most modern lenders review the previous 12 to 24 months of data to understand your specific business cycle. This approach ensures your off-season dip doesn't block your growth. We focus on your annual trajectory to unlock the capital you need to scale.

How much working capital should a seasonal business have on hand?

You should maintain a cash reserve equal to 3 to 6 months of your fixed operating expenses. The JPMorgan Chase Institute found that the median small business holds only 27 days of cash buffer, which often leads to failure during extended off-seasons. Having a robust strategy for working capital for seasonal business ensures you can cover payroll and rent without stress. Secure your blueprint for year-round stability.

What are the requirements for revenue-based financing for seasonal companies?

Revenue-based financing typically requires a minimum of $10,000 in monthly revenue and at least 6 months of active business history. Lenders analyze your average deposits rather than just a static credit score. You'll need to provide 4 to 6 months of recent bank statements to prove your seasonal spikes. This streamlined process bypasses the red tape of legacy institutions and accelerates your path to capital.

Is a personal guarantee required for seasonal business funding?

No, you don't necessarily need a personal guarantee to secure funding for your seasonal operations. We offer solutions with No Personal Guarantee to ensure your private assets aren't at risk while you scale your company. This modern approach focuses on your business's health and revenue history instead of your personal debt-to-income ratio. It's a professional partnership designed to help you build a lasting legacy.

How quickly can I receive funds for my seasonal business?

Our streamlined process allows you to receive funds in your account within 24 to 48 hours of approval. We utilize a No Hard Credit Pull system to evaluate your business, ensuring your score stays protected while you explore your options. Speed is critical when you're preparing for a peak season rush. Get Funded quickly so you can focus on execution rather than waiting on bank committees.

What happens to my payments if my seasonal sales are lower than expected?

Your payments decrease automatically if your sales volume drops, provided you use a revenue-based funding model. This structure ties your repayment to a percentage of your daily or weekly sales. If your revenue falls by 30% during a slow month, your payment obligation shrinks by that same 30% immediately. This flexibility protects your cash flow and ensures the debt doesn't become a burden during the off-season.

Can I use a merchant cash advance to prepare for my peak season?

Using a merchant cash advance is a strategic way to secure working capital for seasonal business needs before your peak demand arrives. You can leverage these funds to buy bulk inventory at a 15% discount or hire 10 additional staff members for the holiday rush. This proactive investment ensures you never turn away a customer due to lack of resources. It's a blueprint for maximizing your highest-earning months.