Working Capital Cycle Explained: How to Unlock Your Business Cash Flow

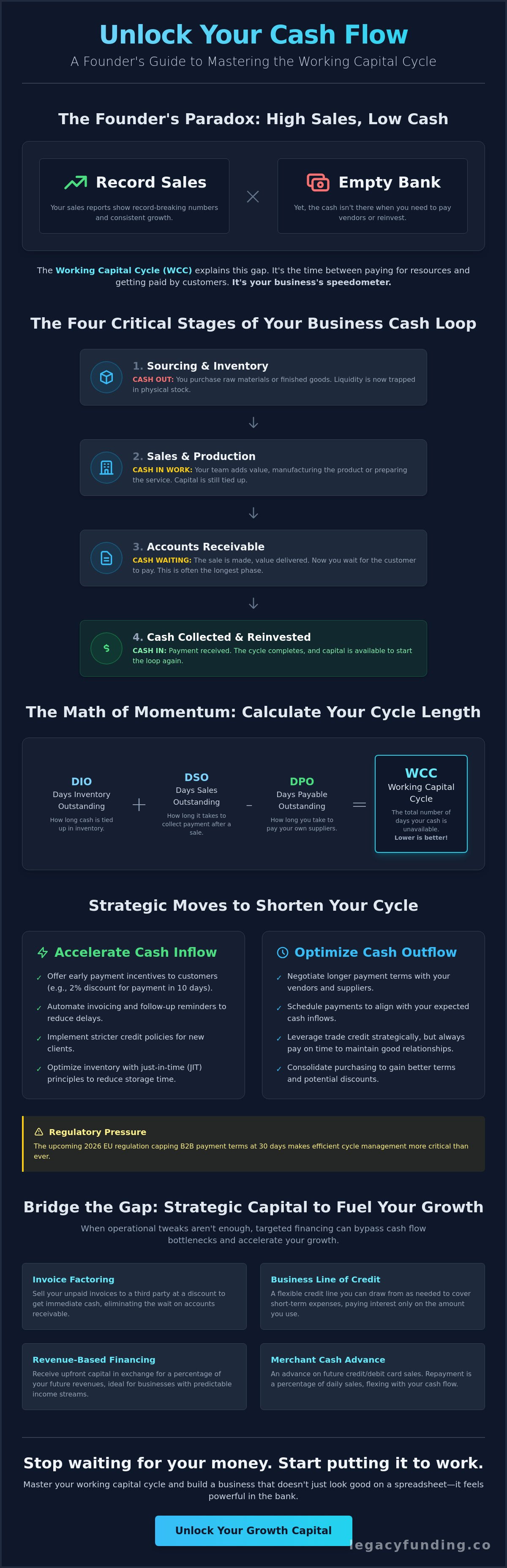

Why does your bank account feel empty when your sales reports show record-breaking numbers? It's a frustrating paradox that keeps many founders awake at night. You're moving product and closing deals, yet the cash isn't there when you need to reinvest. Having the working capital cycle explained is the first step to solving this puzzle and reclaiming your liquidity.

You likely know the feeling of watching capital sit trapped in unpaid invoices or slow-moving inventory while vendor deadlines approach. It's a common bottleneck that stalls momentum. With the 2026 EU regulation now capping B2B payment terms at 30 days, the pressure to manage your cash flow efficiently has never been higher. You need your money moving as fast as your sales team.

We're here to help you master these mechanics and turn your balance sheet into a growth engine. This guide will show you how to accelerate your business by shortening your cycle. We'll identify exactly where your cash is getting stuck, reveal how to speed up collections, and highlight financing options like invoice factoring or business lines of credit to bridge the gap. It's time to stop waiting for your money and start putting it to work.

Key Takeaways

- Identify the disconnect between your sales reports and bank balance by having the working capital cycle explained as a measure of business speed.

- Map the four critical stages of your cash loop to pinpoint exactly where capital gets trapped in inventory or production.

- Calculate your cycle length using a simple, three-part formula to establish a baseline for your operational efficiency.

- Shorten your cycle by leveraging early payment incentives for customers and negotiating longer windows for vendor obligations.

- Accelerate your growth using targeted tools like Revenue-Based Financing or Merchant Cash Advances to bypass traditional cash flow bottlenecks.

Demystifying the Working Capital Cycle: Why Your Cash Is Stuck

Your bank account doesn't care about your accounting software's "net income" line. It only cares about accessible cash. Having the working capital cycle explained is about understanding the velocity of your money. It's the time gap between paying for your inventory and finally receiving payment from your customers. If this gap is too wide, your business is effectively suffocating. You aren't just waiting for money; you're losing the ability to move. Most founders focus on top-line revenue, but revenue is a vanity metric if it's sitting in a customer's accounts payable department for ninety days.

Think of this cycle as your operational heartbeat. It measures how long your capital is "out in the wild" before it returns home with a profit. To scale fast, you must master three phases:

- Source: Secure your materials, inventory, and talent.

- Sell: Deliver your product or service value to the market.

- Succeed: Collect your revenue and reinvest the returns immediately.

The Difference Between Profit and Liquidity

Profitable businesses fail every day because they confuse paper gains with real liquidity. You can have a million-dollar contract on the books, but if you can't pay your team on Friday, that contract is a liability. This is the "cash gap." It's the period where your cash is trapped in unpaid invoices or warehouse shelves. The working capital cycle (WCC) quantifies this struggle. When capital is trapped, growth stops. You're forced to pass on new projects because you can't afford the upfront costs.

Why a Short Cycle Is Your Competitive Advantage

Speed is your greatest asset. A short cycle means your cash is agile. It allows you to pounce on bulk inventory discounts or hire talent before your competitors do. You stop relying on slow, bureaucratic bank debt that takes months to approve. Instead, you fuel growth with your own operational momentum. There's a psychological shift that happens when your cash flow is predictable. You move from a defensive posture to an offensive strategy. You aren't just surviving; you're engineering a scale-up.

Mastering this flow provides the independence to ignore predatory terms and wait for the right strategic partnerships. It’s about building a business that doesn't just look good on a spreadsheet but feels powerful in the bank. By tightening your cycle, you unlock the resources needed to dominate your niche without waiting for the next invoice to clear.

The Four Critical Stages of Your Business Cash Loop

Every dollar you spend undergoes a transformation before it returns to your pocket. This journey isn't a straight line; it's a loop with four distinct pressure points. To have the working capital cycle explained effectively, you must look at where your money lingers. Each stage represents a moment where your capital is either working for you or sitting idle. Efficient founders treat these stages like a relay race where every second counts toward the finish line.

- Stage 1: Sourcing and Inventory. This is the moment your cash goes out the door. You've purchased raw materials or finished goods. At this point, your liquidity has vanished, replaced by physical items sitting in a warehouse.

- Stage 2: Sales and Production. Your team adds value. You manufacture the product or prepare the service for delivery. Your capital is "in work," but you still haven't reached the point of recovery.

- Stage 3: Accounts Receivable. You've made the sale and delivered the value. Now, you wait. This is often the longest phase where your "paper profit" mocks your actual bank balance.

- Stage 4: Accounts Payable. This is your strategic lever. By managing when you pay your own bills, you can keep cash in your business longer. This stage is a vital part of the working capital cycle formula, acting as a buffer against your outflows.

Managing the Inventory Bottleneck

Carrying excess stock is a silent drain on your resources. Every pallet of unsold goods represents frozen cash that could be spent on marketing or talent. However, running too lean risks stockouts and lost revenue. You need to find the "Goldilocks zone" of inventory turnover. High turnover rates directly shorten your cycle and boost your agility. Consider just-in-time sourcing to keep your operations lean. If your inventory is currently draining your reserves, it might be time to explore strategic liquidity options to keep your momentum high.

The Accounts Receivable Waiting Game

Net-30 or net-60 terms are often the biggest growth killers for modern founders. You've done the work, but your customer is essentially using you as a zero-interest bank. This "dead time" between delivery and payment creates a massive cash gap. You can't pay your team with an invoice. Automated invoicing and aggressive follow-ups are no longer optional; they're survival requirements. Every day an invoice remains unpaid is a day your business's growth is voluntarily paused. Shortening this phase is the fastest way to accelerate your entire operation.

The goal is simple: minimize the time cash spends in stages one through three, and maximize the time it stays with you in stage four. When you master this loop, you aren't just managing money. You're engineering a faster, more resilient version of your company.

The Math of Momentum: Calculating Your Cycle Length

Numbers don't lie. They reveal the hidden friction in your operations. To have the working capital cycle explained in practical terms, you must move beyond abstract concepts and look at the hard data. The length of your cycle is the definitive metric of your business’s efficiency. A 90-day cycle means your money is only working four times a year. A 30-day cycle means it’s working twelve. Which version of your business scales faster?

Calculating this number requires three variables from your balance sheet. The standard formula is: Days Inventory Outstanding (DIO) + Days Sales Outstanding (DSO) – Days Payable Outstanding (DPO). This simple equation tells you exactly how many days your cash is out of reach. If you are a retailer holding stock for 40 days (DIO) and waiting 30 days for customer payments (DSO), but you pay your suppliers in 20 days (DPO), your cycle is 50 days. You are effectively financing your own growth gap for nearly two months.

Days Inventory Outstanding (DIO)

DIO measures the average time it takes to turn physical stock into a completed sale. It is the ultimate metric for warehouse efficiency and supply chain management. Every day your inventory sits on a shelf is a day it isn't earning a return. Lowering this number through better demand forecasting or leaner ordering frees up immediate capital. You don't need more sales to find this cash; you just need to move your existing stock faster.

Days Sales Outstanding (DSO)

DSO represents the average time it takes to collect payment after the sale is finalized. For service-based businesses without physical inventory, this is the primary lever for growth. If your industry benchmark is 30 days but your DSO is 45, you're losing two weeks of liquidity on every single transaction. A savvy founder monitors the operational efficiency of their collection process as closely as their sales funnel. Tightening this window is the fastest way to inject cash into your bank account without increasing your debt.

The "Holy Grail" of finance is Negative Working Capital. This happens when your DPO is longer than the sum of your DIO and DSO. In this scenario, your customers and vendors are essentially financing your growth. You receive cash from sales before you even have to pay for the inventory. While difficult to achieve, it’s the engine behind some of the world’s most aggressive scalers. Start looking at your balance sheet with new eyes. Identify the laggards in your DIO and DSO. When you have the working capital cycle explained through these metrics, you stop guessing and start engineering your expansion.

Strategic Moves to Tighten Your Working Capital Cycle

Knowledge is only half the battle. Once you have the working capital cycle explained through your own data, you must act to tighten the loop. Every day you shave off your cycle is a day you gain in liquidity. It is the difference between waiting for a check and writing one for a new opportunity. Shortening this cycle is not a one-time event; it's a continuous process of optimization. You are looking for friction points and eliminating them with clinical precision.

The Power of Vendor Negotiation

Your vendors are your partners in growth. If you have a solid payment history, use it as leverage to move from 30-day to 45-day terms. This 15-day extension is essentially an interest-free loan from your supplier. It keeps cash in your bank account longer without increasing your liabilities. Build a relationship based on transparency. When you prove your reliability, suppliers are more likely to grant you the flexibility you need to scale. This strategic delay in payables is the easiest way to maximize your "free" capital.

Incentivizing the Customer

The psychology of early payment is simple: people move faster when there's a clear benefit. Offering a "2/10 net 30" discount means the customer gets 2% off if they pay within ten days. While it sounds like you're losing money, it is often significantly cheaper than the cost of carrying debt. You're trading a small margin for immediate speed. Use a direct call-to-action on every invoice: "Save 2% by paying within 10 days; help us fuel your next project faster." This turns your accounts receivable from a waiting game into an active revenue stream.

Beyond negotiation and incentives, you must look at your internal operations. Audit your inventory for slow-moving items and liquidate them immediately. With the 2026 SEC inventory reporting guidelines requiring more transparency on valuation and obsolescence, there has never been a better time to clear the shelves. Slow stock is a graveyard for capital. Digitize your billing to remove mailing and processing delays. Every hour saved in the invoicing process is an hour closer to a deposit.

Finally, use your data to predict cash lulls before they happen. Identify your seasonal dips and prepare your reserves in advance. If your internal optimizations aren't enough to bridge the gap during a rapid expansion phase, you can apply for a business line of credit to maintain your momentum. Control the clock, and you control your company's future.

Leveraging Strategic Capital to Fuel Your Growth Cycle

Internal optimization only goes so far. When you land a contract that doubles your volume, you can't wait for your 45-day collection window to catch up. You need an immediate bridge. Having the working capital cycle explained earlier in this guide highlighted your liquidity gaps; now it is time to fill them. Strategic capital transforms your "waiting time" into "working time." It ensures your momentum never stalls because of a mismatch between sales and receipts.

Revenue-Based Financing: The Modern Bridge

Revenue-Based Financing solves the DSO bottleneck by providing capital based on your future receivables. You aren't taking on traditional, restrictive debt; you're accelerating your own success. Legacy Funding Advisors offers a 24-48 hour funding window to keep your projects moving forward. This is capital for rapid expansion, not just operational survival. It gives you the power to fulfill larger orders without draining your reserves.

Why Traditional Banks Fail the Growth Test

Traditional institutions move at a glacial pace that ignores the speed of your industry. They focus on lagging indicators like personal credit scores rather than your current cash flow metrics. Legacy Funding Advisors acts as a savvy, tech-forward ally that understands the modern founder's needs. We prioritize your growth velocity over bureaucratic red tape. Ready to accelerate your cycle? Apply in minutes.

Stop letting your working capital cycle dictate your growth rate. Whether you need a Merchant Cash Advance to cover an inventory surge or Working Capital Loans for ongoing flexibility, the right partner makes the difference. We provide the modern key to financial independence and scaling. Don't let your cycle stop your scale.

Master Your Momentum and Scale with Precision

You now have the working capital cycle explained as a dynamic engine for your expansion. By auditing your inventory, tightening your collection windows, and negotiating vendor terms, you turn idle time into active liquidity. Speed is your most valuable currency. Don't let your cash stay trapped in the gaps between production and payment. Mastering these metrics allows you to move from a defensive posture to a bold, offensive strategy.

Legacy Funding Advisors is your partner in this acceleration. We provide tailored solutions for various industries with a focus on your current cash flow rather than just a lagging credit score. You can secure the capital you need in as little as 24 to 48 hours. Get the capital you need to fuel your growth cycle; apply now at Legacy Funding Advisors.

Your expansion shouldn't wait for an invoice to clear. Take control of your liquidity and build the future of your business today. You have the tools and the data. Now, it's time to lead.

Frequently Asked Questions

What is a good working capital cycle length?

A good working capital cycle length is one that is shorter than your industry average and allows for continuous reinvestment. While a 30-day cycle is often a benchmark for retail, the specific number matters less than the trend. You want to see this number decreasing over time. High velocity means your money works harder. If your cycle is shrinking, your efficiency is rising.

Can a business have a negative working capital cycle?

A negative working capital cycle is entirely possible and represents the peak of operational efficiency. This happens when you collect cash from customers before your bills to suppliers come due. It creates a self-funding growth engine. Major retailers often achieve this by negotiating long payment terms with vendors while moving inventory quickly. It's a powerful way to scale without traditional debt.

How does the working capital cycle differ from the cash conversion cycle?

These two terms are functional synonyms in most business discussions. Both measure the time elapsed between spending a dollar on production and receiving it back from a sale. When you hear the working capital cycle explained by a consultant, they're likely looking at the same DIO, DSO, and DPO metrics used for the cash conversion cycle. Both focus on the speed of your liquidity.

What industries typically have the longest working capital cycles?

Industries like manufacturing, construction, and wholesale distribution typically endure the longest cycles. These sectors require massive upfront investments in raw materials and labor long before a finished product is sold. A construction firm might face a 120-day gap between sourcing materials and receiving a milestone payment. This creates a high-pressure environment where managing the cash gap is a daily survival requirement for the founder.

How much working capital should my business have on hand?

Aim for a current ratio of 1.2 to 2.0 to ensure your business remains resilient. This means your current assets should be at least twenty percent higher than your current liabilities. Having too little cash on hand leaves you vulnerable to market shifts. However, holding too much cash suggests you aren't reinvesting enough into growth. Balance your safety net with your need for aggressive expansion.

Does revenue-based financing affect my working capital cycle?

Revenue-based financing directly accelerates your cycle by turning your future receivables into immediate liquidity. It removes the friction of the collection stage by bypassing the standard wait time. Instead of waiting for a client to clear an invoice, you get that capital in 24 to 48 hours. This allows you to buy more inventory and start the next loop immediately. It's a tool for high-speed scaling.

What happens if my working capital cycle is too long?

A cycle that is too long traps your capital and can lead to insolvency despite high sales volume. This is often called "overtrading," where your growth outpaces your available cash. You may find yourself unable to pay vendors or meet payroll because your money is stuck in unpaid invoices. This stagnation forces you into a defensive posture. It ultimately limits your ability to pounce on new market opportunities.