What Is a Fair Interest Rate for a Business Loan in 2026?

A low interest rate is worthless if the capital arrives three months after your biggest opportunity has passed. With the U.S. Prime Rate holding at 6.75 percent, chasing the absolute lowest percentage often means sacrificing the speed and flexibility your growth demands. You want to scale. You want to move fast. You don't want to get bogged down in a swamp of confusing APRs, factor rates, and bureaucratic delays. Determining what is a fair interest rate for a business loan in 2026 requires looking past the headline number and focusing on the total return on your investment.

We understand the pressure of needing fast capital without the fear of getting ripped off by hidden fees. This guide provides the definitive 2026 benchmarks for everything from SBA 7(a) variables to revenue-based financing. You'll learn how to evaluate the true cost of capital, calculate your potential ROI, and navigate the new 100 percent U.S. citizenship requirements for federal programs. We are moving you from confusion to a clear strategy for financial independence. Let's break down the current rates and find the right fuel for your expansion.

Key Takeaways

- Benchmark your expectations against 2026 market averages to identify what is a fair interest rate for a business loan across bank, SBA, and online channels.

- Master the math behind APR and factor rates to calculate the true cost of capital and protect your bottom line from hidden expenses.

- Shift your perspective from the cost of interest to the ROI of speed, ensuring you don't miss high-stakes opportunities while waiting for legacy approvals.

- Expose hidden origination fees and cash flow drains that can turn a seemingly cheap loan into a growth-stifling burden.

- Leverage streamlined alternatives like Revenue-Based Financing to secure capital in as little as 24 hours and maintain your competitive momentum.

The 2026 Benchmark: What Defines a Fair Business Loan Rate Today?

Fairness in finance isn't a fixed point on a graph. It's a calculated balance between your risk profile, your growth potential, and your deadline. If you're asking what is a fair interest rate for a business loan in June 2026, you must look at your clock as much as your credit score. A rate is fair if the return on that capital exceeds the cost of the debt. For a high-growth founder, waiting sixty days for a 7 percent bank loan is often more expensive than accepting a 15 percent rate that hits the account in 24 hours. Speed is a line item, and in 2026, it carries a premium.

The 2026 lending environment remains defined by a steady-rate posture from the Federal Reserve. With the U.S. Prime Rate holding at 6.75 percent, the floor for commercial capital is firmly set. Understanding what an interest rate is helps you see that these percentages aren't arbitrary. They are a reflection of market risk, inflation expectations, and the lender's cost of funds. What is fair for a Fortune 500 enterprise with decades of audited financials will never be the same as what is fair for a scaling startup. You aren't just buying money; you're buying the ability to move faster than your competition.

Current Market Ranges by Lender Type

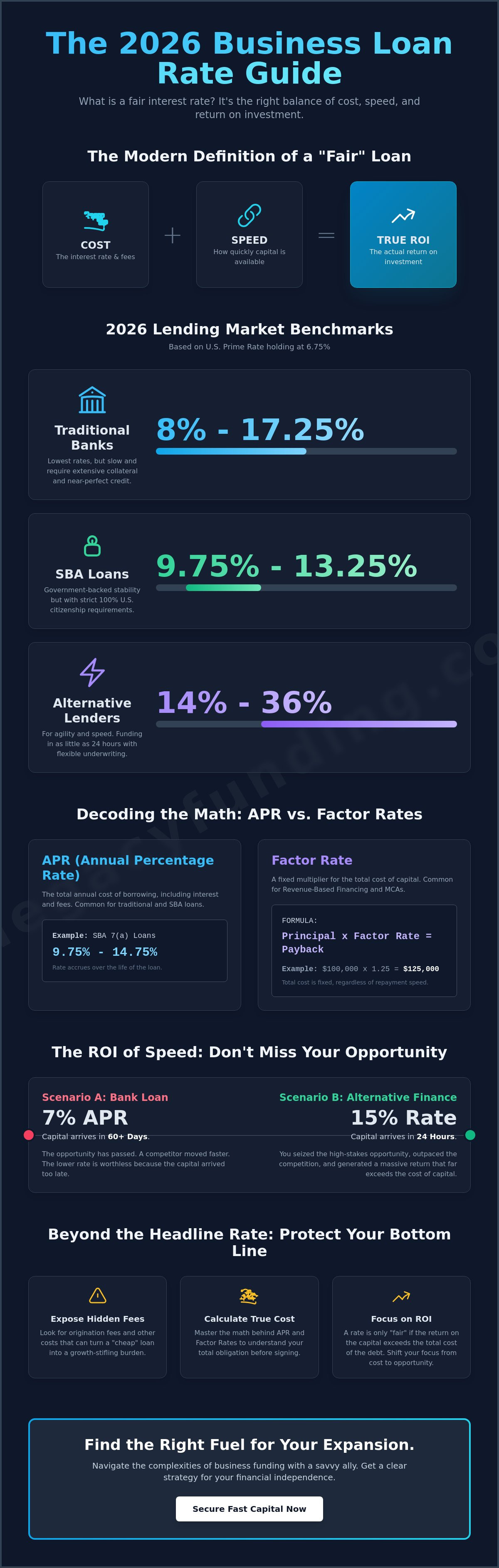

- Traditional Banks: These offer the lowest rates, typically ranging from 8 percent to 17.25 percent. However, they demand near-perfect credit and extensive collateral. Expect a high barrier to entry and a slow approval process.

- SBA Loans: Government-backed options like the 7(a) program offer variable rates between 9.75 percent and 13.25 percent. They provide stability but come with strict new 100 percent U.S. citizenship ownership requirements.

- Alternative Lenders: Online term loans and revenue-based financing fill the gap for businesses that need agility. Rates here typically range from 14 percent to 36 percent, justified by rapid 24-hour funding and flexible underwriting.

Why Rates Haven't Dropped in 2026

Expectations for a rate cut in early 2026 were sidelined by the Federal Reserve's commitment to long-term stability. New Fed leadership has prioritized a "higher for longer" strategy to ensure inflationary pressures don't resurface. Additionally, ongoing global supply chain disruptions have increased the risk premiums that lenders charge. When the cost of doing business rises globally, lenders protect their downside by maintaining higher benchmarks. To determine what is a fair interest rate for a business loan today, you must accept this baseline. Don't wait for a market shift that isn't coming; instead, focus on the ROI of the capital you can secure right now.

Decoding the Math: APR vs. Factor Rates

Confusion is the enemy of growth. When you're trying to figure out what is a fair interest rate for a business loan, you'll likely encounter two different mathematical systems: APR and factor rates. Traditional banks and government programs focus on Annual Percentage Rate (APR). This represents the total annual cost of borrowing, including interest and fees, expressed as a percentage. For instance, current SBA loan rates for 7(a) programs currently range from 9.75 percent to 14.75 percent. This is a solid benchmark for long-term debt, but it doesn't tell the whole story for modern, fast-moving alternative capital.

Alternative financing, such as Merchant Cash Advances (MCAs) and Revenue-Based Financing, typically uses factor rates. Instead of a percentage that accrues over time, a factor rate is a fixed multiplier. If you're quoted a 1.2 factor on $100,000, you owe $120,000. The math is simple, transparent, and predictable. This structure is ideal for businesses that prioritize speed and accessibility over the multi-year commitments of a traditional term loan. If you need a savvy ally to help you navigate these numbers, reach out for a consultation to see which structure fits your cash flow.

Understanding the Factor Rate Formula

Calculating your obligation is straightforward: Principal x Factor Rate = Total Payback. In 2026, typical Revenue-Based Financing factor rates hover between 1.20 and 1.45. While this might look high compared to an annual interest rate, remember that factor rates are not annualized. They represent the total cost of the capital regardless of how quickly you repay it. Because the cost is fixed, early repayment usually doesn't reduce the total amount owed. This provides a level of certainty that traditional variable-rate loans lack. You know exactly what you owe from day one, allowing you to plan your expansion with surgical precision.

When to Use APR vs. Factor Rates

The choice depends on your objective. Use APR for long-term investments like real estate or heavy machinery where you have years to amortize the cost. Use Factor Rates for short-term opportunities like inventory spikes or urgent repairs. Consider this comparison: a 10 percent APR loan for $100,000 over five years might cost you over $27,000 in interest alone. A 1.2 factor rate for the same amount repaid in six months costs exactly $20,000. On paper, the APR is lower, but the total dollar cost of the factor-rate product is actually less. Understanding this nuance is the key to identifying what is a fair interest rate for a business loan for your specific situation.

- APR: Best for 3 to 10 year terms, real estate, and major equipment.

- Factor Rate: Best for 3 to 18 month terms, inventory, and bridge capital.

- Cash Flow Impact: Factor rate products often use daily or weekly micro-payments, which can be easier to manage than one large monthly bank payment.

Why Fair is Relative: The Risk-Reward Framework

Fairness is a subjective metric in the capital markets. Many founders fixate on the single digit rates offered by legacy banks while ignoring the hidden costs of their rigid requirements. If you're wondering what is a fair interest rate for a business loan in 2026, you have to look at the collateral you aren't pledging and the speed you are gaining. Traditional lenders demand personal guarantees and physical assets to secure their downside. Alternative capital often operates on an unsecured basis. This shift in risk from your personal balance sheet to the lender's books naturally carries a higher premium. You're paying for protection and agility. You're buying the freedom to grow without risking your home.

Context defines the value of every dollar you borrow. For example, SBA 7(a) loan interest rates currently range from 9.75 percent to 14.75 percent. These are excellent benchmarks for stability, but they come with a 60 to 90 day waiting period and mountains of paperwork. In contrast, online lenders provide funding within 24 to 48 hours. This speed allows you to capitalize on sudden market shifts. A higher rate is objectively fair when it solves an urgent liquidity crisis or secures a time-sensitive contract. Don't let a lower percentage blind you to the total utility of the funds.

The Value of Opportunity Cost

Waiting is an expense that doesn't show up on a loan offer. A 60-day bank approval cycle is a lifetime in the 2026 economy. If a cheap loan causes you to miss a bulk inventory discount or a strategic acquisition, that loan actually cost you the lost profit of the deal. Speed is a competitive advantage. A 20 percent cost of capital is fair if it allows you to capture a 50 percent margin opportunity that would otherwise vanish. Stop measuring the cost of the money. Start measuring the value of the time it buys you. Efficiency has a price, and it's usually worth paying.

Risk Factors Lenders Evaluate

Lenders in 2026 have moved beyond the simple credit score. While your personal history still matters, modern underwriters prioritize your real-time cash flow and revenue consistency. They look at your industry's volatility. A SaaS company with recurring revenue presents a different risk profile than a seasonal retail shop. They evaluate your debt-service-coverage ratio to ensure you can handle repayments without choking your operations. Understanding these variables helps you see what is a fair interest rate for a business loan for your specific situation. High-risk industries or younger companies will naturally see higher rates to offset the lender's exposure.

Beyond the Percentage: Calculating Your True Cost of Capital

Don't let a single-digit number deceive you. To accurately determine what is a fair interest rate for a business loan, you have to peel back the layers of the term sheet. A traditional lender might offer a 9 percent rate, but once you add a 3 percent origination fee, closing costs, and monthly maintenance charges, your effective cost of capital climbs. You must focus on the total dollar amount you will pay back. If the capital doesn't produce more value than it costs to carry, the rate isn't fair; it's a weight around your neck. You are looking for fuel, not a financial anchor.

Start your evaluation by identifying every fee before you sign. Once the total cost is clear, look at the repayment rhythm. A monthly payment is common for bank debt, but daily or weekly micro-payments often align better with the natural flow of modern commerce. This prevents the "payment shock" that can happen when a large chunk of cash leaves your account at the end of the month. Finally, measure the impact on your growth. If you can use a working capital loan to secure a major contract or a strategic asset, the interest becomes a secondary metric. Speak with our financial allies to run a custom ROI analysis for your next expansion project.

The ROI Test for Business Funding

Capital ROI is the net profit generated by the investment divided by the total cost of the funds. Consider the bulk inventory strategy. If using a short-term loan allows you to buy materials at a 20 percent discount, and the total cost of that capital is only 6 percent, you have created a 14 percent margin boost out of thin air. This is the ultimate litmus test for fairness. A high-rate loan that fuels 3x growth is objectively fairer than a low-rate loan that restricts your ability to scale. Focus on what the money does, not just what it costs.

Common Fees That Inflate the Rate

- Origination Fees: These are upfront administrative costs for processing the deal. They typically range from 1 percent to 5 percent of the total funding amount.

- Draw Fees: Common with a business line of credit, these are costs triggered every time you move funds into your operating account.

- Prepayment Penalties: These are hidden costs for being successful. Some legacy institutions charge you for paying back early to protect their interest income. Modern alternative lenders often remove these barriers, allowing you to settle the debt as soon as your cash flow allows.

To find what is a fair interest rate for a business loan in 2026, you must compare terms, not just percentages. Flexibility has a value. If one lender offers a lower rate but requires a blanket lien on all your assets, and another offers a slightly higher rate with no collateral, the second option is often the fairer choice for a founder who values their independence.

Securing Fast Capital with Legacy Funding Advisors

Traditional institutions remain trapped in a cycle of slow approvals and rigid structures. Legacy Funding Advisors breaks that cycle. We treat capital as a tool for expansion, not a burden of debt. When you evaluate what is a fair interest rate for a business loan, you are really evaluating the speed and flexibility of the partner behind it. Our 24 to 48 hour funding window ensures you never lose a strategic deal to a slow bank process. We prioritize your real-time cash flow over an arbitrary credit score cut-off. This is modern finance built for the speed of the 2026 economy.

Fairness is about alignment. A loan that demands a fixed payment during a seasonal dip isn't fair; it's dangerous. Our Revenue-Based Financing model solves this by scaling your payments with your actual revenue. When your sales are high, you pay more. When they lean out, your payments adjust accordingly. This preserves your operational breathing room and protects your bottom line. We provide the capital you need without the bureaucratic friction that slows down your competitors. Scale your operations. Protect your equity. Move with confidence.

Our Transparent Funding Solutions

- Revenue-Based Financing: Access capital based on your future sales. Keep your equity while you scale your operations.

- Merchant Cash Advances: Secure fast capital designed for high-volume businesses. Get the cash you need to bridge inventory gaps.

- SBA Loans: Leverage our expert guidance to secure long-term, low-cost capital through government-backed programs.

The Legacy Advantage: Partnership Over Transactions

We take a consultative approach to your growth. We don't just provide a list of numbers; we help you find your ideal cost of capital based on your specific ROI goals. Our application process is designed to remove ambiguity and lower the barrier to entry for modern founders. There are no hidden agendas and no wasted time. Every interaction is designed to move you one step closer to financial independence. Stop waiting for legacy institutions to catch up to your vision. Get a transparent funding quote in 24 hours and start your next phase of growth today.

Take Command of Your Capital Strategy

You now have the tools to look past the headline numbers and see the true value of your funding options. Determining what is a fair interest rate for a business loan in 2026 isn't just about a percentage; it's a strategic calculation of ROI and opportunity cost. We've decoded the difference between APR and factor rates, highlighted the cost of waiting for slow banks, and established a framework for measuring capital impact. Your focus should remain on growth metrics and cash flow sustainability.

We specialize in tailored solutions across the US, Puerto Rico, and Canada that prioritize your business health over restrictive credit scores. Our process is built for the modern founder who values speed, transparency, and results. With funding approved in as little as 24 hours, you can stop waiting for permission to scale. Secure your growth capital with a transparent quote from Legacy Funding Advisors today. Your expansion is the priority. Let's execute your vision with the efficiency it deserves.

Frequently Asked Questions

What is considered a good interest rate for a small business loan in 2026?

A good rate depends on the lender type, but for bank loans, 8 percent to 12 percent is currently competitive given the 6.75 percent prime rate. SBA 7(a) variable rates between 9.75 percent and 13.25 percent are also strong benchmarks. Determining what is a fair interest rate for a business loan requires balancing these percentages against the speed and collateral requirements of the lender.

Why are online business loan rates so much higher than bank rates?

Online lenders charge higher rates because they assume greater risk and provide capital significantly faster than traditional banks. While a bank might take 60 days to approve a loan, alternative lenders often fund within 24 to 48 hours. This premium covers the lack of physical collateral and the streamlined underwriting process that allows you to capitalize on urgent growth opportunities without bureaucratic delays.

How do factor rates compare to traditional APR?

Factor rates are fixed multipliers used for short-term financing, whereas APR is an annual percentage that can accrue over time. A 1.2 factor rate means you pay back $1.20 for every $1.00 borrowed, regardless of the repayment speed. APR includes interest and fees over a year. Factor rates offer total cost transparency upfront, making them ideal for rapid inventory turns or bridge capital where certainty is paramount.

Does my personal credit score affect my business loan interest rate?

Your personal credit score remains a secondary metric for most small business lenders in 2026. While alternative financing focuses heavily on real-time cash flow and revenue consistency, a strong personal score can unlock lower rates or higher funding limits. Traditional bank and SBA loans still maintain strict credit minimums, often requiring a 680 score or higher for the best terms and lowest cost of capital.

Are business loan interest rates fixed or variable?

Both structures are common, though variable rates are standard for SBA 7(a) loans and bank lines of credit. Variable rates often peg to the U.S. Prime Rate, which is 6.75 percent as of June 2026. Fixed rates provide payment stability and are typical for equipment financing and term loans. Choosing between them depends on your tolerance for market fluctuations and your specific long-term cash flow projections.

What happens if I want to pay off my business loan early?

Early repayment impact depends entirely on your loan agreement. Some traditional bank loans carry prepayment penalties to protect the lender's interest income. However, many modern alternative lenders allow you to settle the debt early without extra fees. In factor-rate financing, you generally pay the full agreed-upon amount even if you settle early, as the total cost is fixed at the start of the transaction.

Can I get a fair rate with a low credit score?

You can secure what is a fair interest rate for a business loan even with a sub-600 credit score by leveraging revenue-based financing. These lenders prioritize your daily and monthly bank deposits over your historical credit report. While the rate will be higher than a prime bank loan, it remains fair if the capital generates a high enough ROI to justify the cost of the expansion.

How much are typical origination fees for business financing?

Origination fees typically range from 1 percent to 5 percent of the total loan amount. These upfront costs cover the administrative work of underwriting and processing your application. Always ask for a full breakdown of fees before signing, as these charges can significantly increase your effective APR. Some lenders may also include closing costs or maintenance fees that further impact the total cost of capital for your business.