What Happens if You Default on an MCA? A Founder’s Guide to Recovery

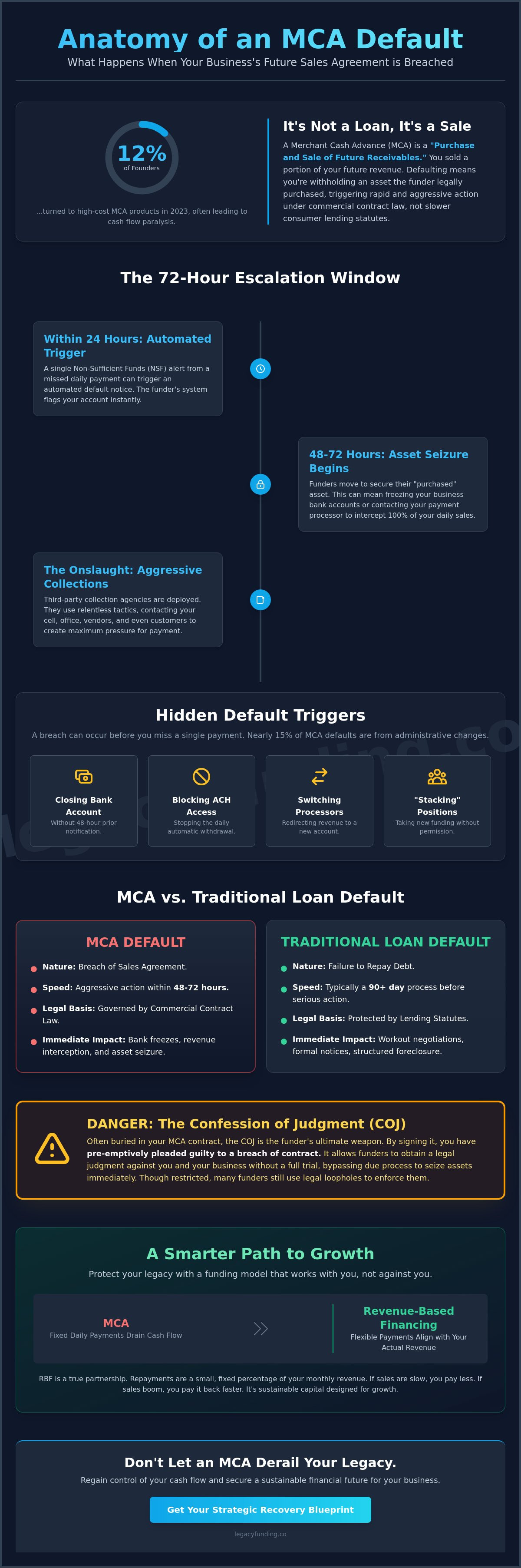

Your bank account triggers a low balance alert every morning at 9:01 AM as another aggressive ACH withdrawal clears. You signed a contract for a "purchase of future sales," but it feels like a weight pulling your business under. If you are reading this, you are likely asking what happens if you default on an mca and whether your personal assets are truly at risk. You aren't alone in this struggle. The 2023 Small Business Credit Survey revealed that 12 percent of founders turned to these high cost products, only to find their cash flow paralyzed by daily repayment cycles.

We understand that protecting the legacy you've built is your top priority. You deserve a partner who helps you regain leverage rather than draining your resources. This guide provides the strategic blueprint you need to stop the aggressive collections cycle and secure your business future. We will break down the legal reality of MCA contracts, show you how to shield your assets, and outline the path toward sustainable capital that actually fuels growth.

Key Takeaways

- Identify the technical triggers of a breach to understand why an MCA default differs fundamentally from a traditional bank loan failure.

- Understand exactly what happens if you default on an mca, from the immediate impact of UCC-1 filings to the risk of bank account freezes.

- Leverage the reconciliation clause to protect your operations and keep your daily payments aligned with actual revenue.

- Follow a strategic recovery blueprint to open proactive communication with funders and secure your business assets before a crisis hits.

- Unlock the benefits of Revenue-Based Financing as a smarter alternative to scale your business and protect your professional legacy.

What Does It Mean to Default on an MCA? Understanding the Breach

Defaulting on a Merchant Cash Advance (MCA) isn't the same as missing a standard bank loan payment. It's a breach of a "Purchase and Sale of Future Receivables" agreement. You didn't borrow money; you sold a portion of your future revenue at a discount. When you stop the flow of that revenue, you aren't just late. You're effectively withholding an asset the funder already legally owns. This distinction is critical for understanding what happens if you default on an mca. While a traditional bank might wait 90 days to initiate a workout, MCA funders often move within 72 hours. They use aggressive legal frameworks because the transaction is governed by commercial contract law rather than consumer lending statutes.

Technical Triggers Beyond Missed Payments

A breach often occurs before a payment is even missed. Funders monitor your activity with precision. If you close a bank account without 48 hours of prior notification, you've triggered a default. If you block ACH access or switch your merchant processor to bypass the daily pull, you've breached the contract. Even taking out "stacked" positions, where you secure additional funding from another source without written permission, can violate your agreement. These technicalities allow funders to accelerate the full balance immediately. In 2023, industry reports indicated that nearly 15% of MCA defaults were triggered by administrative changes rather than a total lack of funds. Don't let a technicality derail your business scaling efforts.

The 24-Hour Escalation Window

Speed is the funder's greatest leverage. Automated monitoring systems scan for Non-Sufficient Funds (NSF) alerts daily. A single NSF notification can trigger an automated default notice within 24 hours. Because these are sales of assets, funders don't follow the slow foreclosure paths of traditional banks. They move to secure your bank accounts or contact your credit card processor to intercept 100% of your daily sales. This rapid escalation is designed to protect their purchase before your cash flow dries up. Knowing what happens if you default on an mca helps you anticipate these moves before they paralyze your operations. Reach out to a professional ally to blueprint your recovery before the 24-hour window closes. Leverage your knowledge to protect your legacy.

The Immediate Repercussions: Bank Freezes and UCC Liens

Defaulting on a merchant cash advance (MCA) triggers a chain reaction that moves faster than traditional bank litigation. Within 48 to 72 hours of a missed payment, your business can be effectively paralyzed. This isn't a slow-moving lawsuit; it's a rapid-fire seizure of your operational capacity. Understanding what happens if you default on an mca starts with recognizing that these funders prioritize speed over due process. They don't wait for a court date to protect their interests.

The aggressive nature of third-party collection agencies in this space is unparalleled. These firms operate with a level of persistence that borders on harassment. They target your cell phone, your office line, and even your vendors. Their goal is simple: create enough friction that you pay just to stop the noise. You are no longer dealing with a financial partner; you are dealing with a recovery specialist trained to exploit every point of leverage in your contract.

UCC-1 Liens: The Invisible Credit Killer

A UCC-1 filing is a public red flag that sits on your business credit report. It tells every other financial institution that another entity has a claim on your assets. When a default occurs, this lien becomes a weapon. Funders often contact your customers or vendors directly. They issue letters demanding that payments meant for you be redirected to them. This destroys your professional reputation and cuts off your cash flow at the source.

- Capital Blockade: Traditional banks will not touch a business with an active UCC lien.

- Vendor Distrust: Suppliers may move you to "cash only" terms once they see a default record.

- Removal Difficulty: Clearing a lien requires a formal termination statement. Funders rarely sign these without a 100% settlement.

Confessions of Judgment (COJ) and Legal Fast-Tracks

The Confession of Judgment (COJ) is the most dangerous document in the MCA world. By signing it, you essentially pleaded guilty to a breach of contract before it ever happened. While New York passed legislation in 2019 to limit COJs against out-of-state businesses, many funders still utilize the "New York Loophole" by structuring contracts through specific jurisdictions. This allows them to obtain a legal judgment without a full trial or even notifying you beforehand.

Once they have this judgment, they issue a "Notice of Levy" to your bank. Your accounts are frozen instantly. You lose access to payroll, rent, and inventory funds. Even if you didn't sign a traditional personal guarantee, most contracts include a "Performance Guarantee" or "Validity Guarantee." If you stop the daily ACH pull, you've committed a "bad act" under the contract. This triggers personal liability for the entire balance, putting your personal savings and assets at risk. If you are facing these pressures, it is time to reclaim your financial narrative before the damage becomes permanent.

The system is designed to move fast. It's built to favor the funder. It's optimized for recovery. You need a blueprint that accounts for these aggressive tactics to protect your legacy and your future growth.

MCA Default vs. Traditional Loan Default: A Critical Comparison

Traditional bank loans and Merchant Cash Advances (MCAs) occupy opposite ends of the financial spectrum. A bank loan is debt; it's a fixed obligation that demands payment regardless of your performance. If you miss a payment on an SBA loan, the bank moves to seize your collateral, which often includes your home or equipment. An MCA is different. It's a purchase of future sales. This distinction changes everything when you analyze what happens if you default on an mca.

Traditional lenders report to personal credit bureaus within 30 days of a missed payment. This can tank a founder's score by 100 points or more instantly. Most MCAs are technically non-recourse. They don't require the same 100% collateralization seen in federal programs. Instead of taking your house, the funder takes a percentage of your daily sales. If those sales don't happen, the obligation shouldn't trigger a standard default. You're not failing to pay a debt; you're simply not generating the product they already bought.

The Reconciliation Clause: Your Secret Weapon

Reconciliation is the heart of a legitimate MCA contract. It's a mandatory adjustment process that keeps your payments in sync with your actual revenue. If your sales drop by 35% this month, your payment should drop by 35% as well. This mechanism prevents the "death spiral" common in traditional lending. It's the primary reason why a true MCA shouldn't technically default if your revenue hits zero.

Document your downturn. Use your monthly bank statements to prove that the lack of payment isn't a "willful" act of theft. It's a reflection of market reality. If a funder refuses to reconcile your account, they may be crossing a legal line. Courts in several jurisdictions have ruled that refusing to reconcile can turn an MCA into an "usurious loan." This gives you significant leverage during a restructuring. You aren't asking for a favor; you're demanding the contract be honored as written.

Regulatory Oversight and Your Rights

The regulatory world is catching up to the speed of alternative finance. By 2026, new disclosure laws in states like New York and California will force even more transparency on funders. This shift empowers you to negotiate from a position of strength. Don't let aggressive litigation tactics intimidate you. Most funders prefer "Good Faith" negotiations over expensive court battles that can last 12 to 18 months.

Protect your business reputation by staying proactive. Communication is your best asset when figuring out what happens if you default on an mca. Reach out before the bank account hits zero. Professional restructuring allows you to maintain your brand's integrity while you pivot your strategy. You can unlock new paths to growth once you move past the friction of old obligations. Focus on your blueprint for scaling, and don't let a temporary cash crunch define your legacy.

Strategic Recovery: How to Handle a Pending Default

Facing a cash crunch is a test of leadership. It isn't the time to disappear. If you want to control what happens if you default on an mca, you must act before the first ACH payment fails. Silence triggers litigation. Proactive communication triggers negotiation. You have the power to pivot before the situation spirals. Taking the lead now protects your business and your reputation.

Open a direct line with your funder immediately. Gather your last 180 days of bank statements to document the revenue dip. Data removes emotion from the conversation. Use these documents to request a formal restructuring or a 14 day payment pause. This isn't asking for a favor; it's protecting the funder’s asset by ensuring your business survives to pay another day. When you show the numbers, you shift the power dynamic back in your favor.

Consult with a financial advisor specializing in debt consolidation or reverse consolidation. These experts understand the blueprint of high speed funding better than a general accountant. They can help you leverage your remaining assets to secure a more sustainable path forward. Speed is your greatest asset in this phase. A 24 hour delay can be the difference between a workout plan and a frozen bank account. Our process at Legacy Funding emphasizes this speed, often helping founders see a path to Get Funded without the red tape of traditional banks.

The Power of Transparency

Hiding from a funder accelerates the legal process. They assume the worst when you go dark. Instead, draft a professional Hardship Letter that focuses on business continuity. Detail exactly why revenue dropped. Perhaps you faced a 22% supply chain price hike or a seasonal 38% dip in sales. Propose a settlement that protects your long term cash flow. Make it clear that a structured plan is the only path to a full recovery for both parties. Transparency builds the trust necessary to unlock better terms and protect your legacy.

Consolidation as a Path to Freedom

Daily withdrawals can suffocate a growing company. Reverse consolidation offers a blueprint for relief. This strategy provides a weekly deposit that covers your daily MCA obligations. It turns a jagged daily drain into a predictable weekly rhythm. You can also explore debt buyouts to clear high interest positions entirely. This move shifts your focus from survival back to scaling. It allows you to accelerate your growth without the weight of multiple daily debits. Understanding what happens if you default on an mca means knowing how to consolidate before the default occurs.

- Identify high interest daily positions immediately.

- Consult a specialist in debt consolidation to lower your daily burden.

- Switch from aggressive daily pulls to manageable weekly or monthly cycles.

Stop the cycle of predatory withdrawals. If you need a professional to review your current positions and help you regain leverage, connect with our team today.

Building Your Legacy with Revenue-Based Financing

Defaulting on a Merchant Cash Advance (MCA) often feels like a terminal diagnosis for a business. It doesn't have to be. Smart founders recognize that the predatory structure of traditional MCAs is the problem, not their business model. Revenue-Based Financing (RBF) serves as the modern alternative. It aligns your capital needs with your actual growth metrics. If your revenue dips, your payments adjust. This flexibility prevents the suffocating debt cycles that lead you to wonder what happens if you default on an mca in the first place.

Legacy Funding provides the leverage you need without the risks that keep you up at night. We prioritize your future potential over your past credit mistakes. Our model focuses on three core pillars: speed, transparency, and partnership. We don't just provide cash; we provide a foundation for generational scaling. By removing the friction of traditional lending, we help you pivot from defensive survival to aggressive expansion.

- No Personal Guarantee: Your personal assets remain yours. We bet on the business, not your home or personal savings.

- No Hard Credit Pull: We protect your credit score while we secure your funding, preventing unnecessary dings to your profile.

- Flexible Repayment: Payments scale with your daily revenue. This ensures your cash flow stays healthy even during slow months.

The Legacy Funding Blueprint

We unlock capital within 24 to 48 hours. Traditional banks take months; we take days. Our blueprint skips the predatory red tape that defines the MCA industry. We tailor solutions specifically for SMBs that generate consistent revenue but lack the perfect credit profile required by legacy institutions. We act as your high level consultant. We are invested in your scaling journey because our success is tied directly to your performance. This is how you stop worrying about what happens if you default on an mca and start focusing on your market share.

Accelerate Your Growth Today

Transitioning from high cost debt to flexible working capital is a strategic move for any serious founder. The application process is built for speed and accessibility. You provide the data, we provide the capital, and your business provides the growth. It is a simple, three step process designed for the modern founder who values time as much as money. Accessibility and transparency are our benchmarks. Don't let a bad financial instrument dictate your company's ceiling. Take control of your balance sheet and position your business for a generational moment. Get Funded and secure your legacy today.

Take Control of Your Business Legacy

Understanding what happens if you default on an mca is the first step toward building a more resilient capital structure. You've seen how bank freezes and UCC liens can stall your momentum. Unlike traditional banking that relies on rigid 700+ FICO scores, revenue-based financing prioritizes your actual cash flow. This shift in perspective allows you to leverage your daily performance rather than your past credit hurdles. You can protect your enterprise by choosing capital partners that offer transparency, speed, and professional impact.

Strategic recovery requires a partner who moves as fast as the market. We provide a blueprint to accelerate your growth without the friction of outdated institutional barriers. Our process ensures you get the capital you need in 24 to 48 hours. We perform no hard credit pull and focus entirely on your growth metrics. This approach keeps your credit intact while unlocking the liquidity necessary to scale. It's time to stop reacting to debt and start driving your expansion. Your business deserves a financial ally that values results and recognizes your grit.

Secure Your Business Legacy—Get Funded in 24 Hours

Your vision is too important to be sidelined by a temporary cash crunch. Take the next step toward financial freedom today.

Frequently Asked Questions

Can I go to jail for defaulting on a merchant cash advance?

You cannot go to jail for defaulting on a merchant cash advance because it's a civil contract dispute, not a criminal offense. Debtors' prisons were abolished in the United States in 1833. Unless you committed document fraud or intentional misrepresentation during the application, the funder's only recourse is through civil court or arbitration. Protect your business by understanding that this is a commercial transaction between two entities.

Will an MCA default ruin my personal credit score?

Defaulting won't necessarily ruin your personal credit score if the agreement was structured with No Personal Guarantee. Most funders only report to business bureaus like Dun & Bradstreet or Experian Business. However, if you signed a personal guarantee, the funder can pursue your personal assets. Statistics show that roughly 85% of MCA providers will attempt to file a UCC lien which appears on business credit reports rather than personal ones.

What is a Reconciliation Clause and how does it prevent default?

A Reconciliation Clause is a mandatory contract provision that adjusts your daily payment based on your actual sales volume. If your revenue drops by 20%, the funder must lower your withdrawal amount to match that percentage. This mechanism is your primary defense against a technical default. It ensures your cash flow remains sustainable while you scale. Use this blueprint to keep your capital working for you without draining your operating account.

Can an MCA funder sue me if I close my business?

A funder can sue you if they believe the business closure was a strategic move to avoid repayment or if you violated specific clauses. While an MCA is a purchase of future sales, closing the shop stops those sales entirely. This often triggers an immediate breach of contract. Legal data suggests that 1 in 5 defaulted MCA cases end up in some form of litigation or mediation to recover the remaining balance.

How long does it take for a funder to freeze my bank account after a missed payment?

Funders typically move to freeze accounts within 24 to 72 hours after three consecutive missed ACH payments. They often use a Confession of Judgment or a Pre-Judgment Attachment to secure funds quickly. This speed mirrors the fast-paced nature of the industry. You must act immediately to negotiate before the legal department files these documents with the clerk. Swift action is the only way to maintain your operational momentum and legacy.

Is it possible to settle an MCA debt for less than what I owe?

You can often settle an MCA debt for 40% to 60% of the outstanding balance through aggressive negotiation. Understanding what happens if you default on an mca allows you to approach the funder with a realistic lump-sum offer. Funders prefer a guaranteed 50% recovery today over a multi-year legal battle with zero certainty. This strategy helps you clear the path for future credit lines and business growth.

What is the difference between an MCA default and a business loan default?

The main difference is that an MCA default involves a breach of a purchase agreement rather than a promissory note. Business loans are subject to state usury laws and strict banking regulations. MCAs are commercial sales of assets. When you default on an MCA, the funder sues for breach of contract rather than non-payment of a loan. This distinction changes your legal strategy and your blueprint for recovery. Get Funded with clarity on these terms.

How can I stop daily ACH withdrawals if my revenue has dropped?

You can stop daily ACH withdrawals by invoking your right to a reconciliation or by notifying your bank 3 business days in advance. Under NACHA rules, you have the right to revoke authorization for electronic transfers at any time. However, doing this without notifying the funder usually triggers a default. Contact the funder 48 hours before the next pull to request a payment pause. This proactive move preserves your professional relationship and your capital.