Secured vs. Unsecured Business Line of Credit: Choosing the Right Growth Engine in 2026

In 2026, the gap between a market leader and a footnote isn't just your product; it's the speed of the capital behind it. You've felt the sting of a growth spurt stalled by a cash flow gap. You've likely hesitated at the thought of pledging personal assets just to keep the momentum alive. Deciding between a secured vs unsecured business line of credit is the most critical strategic move you'll make this quarter. It's the difference between playing defense with your assets and playing offense with your growth.

Scaling a business requires a partner that values speed as much as you do. You deserve a funding strategy that eliminates friction and honors the pace of modern commerce. This guide empowers you to master the nuances of collateral requirements and interest rate spreads so you can choose the right engine for your trajectory. We'll explore how to unlock immediate liquidity while keeping your risk profile lean. It's time to stop waiting on legacy institutions and start fueling your expansion with precision.

Key Takeaways

- Master the fundamental mechanics of a secured vs unsecured business line of credit to align your funding with your specific risk tolerance.

- Evaluate the critical trade-offs between lower interest rates and the speed of capital to ensure your financing matches your business velocity.

- Identify which assets can serve as leverage without compromising your long-term security or personal peace of mind.

- Apply a strategic framework to determine which credit line fits your specific scenario, from inventory spikes to long-term capital projects.

- Discover how Legacy Funding acts as a bridge, delivering the capital you need without the bureaucratic delays of traditional institutions.

Defining Secured and Unsecured Business Lines of Credit

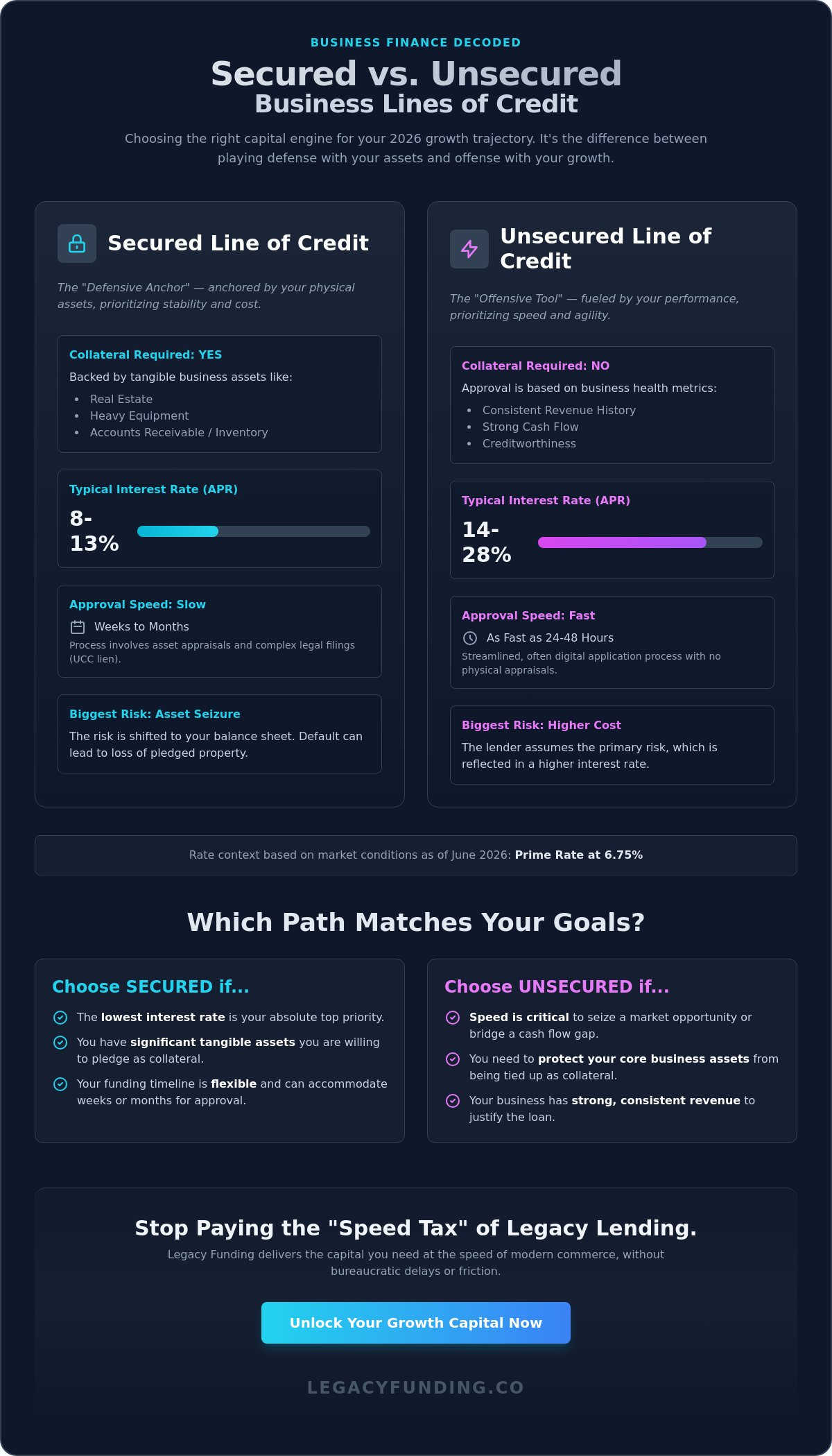

Scaling your business in 2026 requires more than just a good product; it requires a strategic choice in how you fuel that growth. When evaluating a secured vs unsecured business line of credit, the decision hinges on one factor: who carries the risk? A what is a line of credit search reveals that these financial tools are revolving, but their foundations differ significantly. A secured line is anchored by your physical assets, while an unsecured line relies on your operational performance and credit history. This choice dictates how fast you can pivot when a market opportunity appears.

The fundamental shift in this equation is the location of the risk. In a secured arrangement, you move the risk onto your own balance sheet by pledging collateral. In an unsecured arrangement, the lender assumes more risk, which is why they look closer at your revenue metrics. With the Prime Rate currently sitting at 6.75% as of June 2026, the cost of these lines is highly sensitive to how they're structured. Choosing the wrong engine can lead to stalled projects or the loss of critical business property.

How a Secured Line of Credit Works

Secured lines are the defensive anchors of business finance. They require you to pledge specific, tangible assets such as real estate, heavy equipment, or accounts receivable to back the loan. Because the lender has a safety net, they often offer lower interest rates, typically ranging from 8% to 13% APR for well-qualified borrowers. These lines are ideal for long-term stability and large-scale capital projects where the cost of capital is the primary concern.

- Borrowing Base: Your credit limit isn't static; it fluctuates based on the current value of your pledged inventory or receivables.

- Collateral Depth: Lenders may require a mix of assets to reach higher funding limits, sometimes exceeding $500,000 for established firms.

- Asset Risk: A UCC lien is a legal filing that gives the lender a priority claim on your business assets if you fail to meet your obligations.

The Mechanics of an Unsecured Line

Unsecured lines are offensive tools built for speed and agility. They don't require you to tie up your equipment or real estate as collateral. Instead, lenders weigh your creditworthiness and consistent revenue history. While rates can be higher, often reaching between 14% and 28% APR for those with good credit scores, the trade-off is accessibility. You won't spend weeks waiting for appraisals or complex legal filings.

These lines represent the modern approach to scaling. They allow founders to bridge cash flow gaps or jump on inventory spikes without the fear of losing their foundational assets. Because there's no physical collateral to value, the approval process is streamlined. You get a funding partner that understands the velocity of your industry rather than a bank that only sees the value of your machinery. Mastering the balance of a secured vs unsecured business line of credit ensures you always have the right fuel for your specific stage of growth.

Strategic Comparison: Risk, Speed, and Cost Trade-offs

Choosing between a secured vs unsecured business line of credit is a strategic calculation of math and timing. Traditional banks often lure founders with low teaser rates. However, they rarely mention the "speed tax," which is the hidden cost of the opportunities you lose while waiting for an approval. In 2026, market windows open and close in weeks, not months. If your funding takes ninety days to arrive, your competitive advantage is already gone.

Interest rate structures play a major role in this comparison. Secured lines typically offer variable rates tied to the Prime Rate, which currently stands at 6.75%. You'll likely see offers ranging from 8% to 13% APR for well-qualified businesses. Unsecured lines carry higher rates, sometimes reaching 28% APR for those with good credit, but they often provide fixed-cost certainty. This allows you to forecast your repayment without worrying about sudden market fluctuations or benchmark hikes.

The emotional weight of asset seizure cannot be ignored. Pledging your primary warehouse or critical machinery creates a high-stakes environment. If a market downturn hits, a secured lender has the legal right to seize those assets to satisfy the debt. Unsecured lines protect your foundational infrastructure. They prioritize your revenue and cash flow over your physical property. This keeps your business intact even during lean months, allowing you to pivot without losing the roof over your head.

The Speed Factor: Why Unsecured Wins for Rapid Response

Time is your most valuable asset. Unsecured alternative lending platforms frequently provide a 24-48 hour funding window from application to draw. Compare this to the 30-90 day marathon required for secured bank lines involving property valuations and title searches. A 2% difference in interest rate is irrelevant if the delay costs you a million-dollar contract or a critical inventory buy. Move fast, secure the deal, and outpace the competition before they even finish their paperwork.

The Cost of Collateral: Beyond the Interest Rate

Look past the headline APR. Secured lines come with a trail of soft costs that many founders overlook. You'll pay for third-party appraisals, environmental reports, and ongoing audits to maintain the borrowing base. These fees can add thousands to your initial draw. Unsecured lines offer a clean balance sheet. They don't clutter your filings with restrictive UCC liens, which keeps you attractive for future equity rounds or specialized equipment financing. Discuss your growth timeline with a specialist to see which model preserves your flexibility in a volatile market.

Common Collateral Types and Personal Guarantees

Understanding the architecture of a secured vs unsecured business line of credit requires a deep dive into what you're actually putting on the table. In a secured arrangement, lenders look for "hard" collateral. This typically includes commercial real estate, heavy machinery, or your accounts receivable. Traditional institutions often push for a "blanket lien." This legal claim covers every asset your business owns, from the laptop on your desk to the fleet in your warehouse. It's a total-capture strategy that limits your future borrowing power.

Modern founders are increasingly turning to performance-based models. Revenue-based financing offers a different path. It ignores hard collateral in favor of your actual monthly income. This approach treats your growth as the asset. It provides the liquidity you need without requiring you to risk the deed to your property or the keys to your equipment. It's a cleaner, faster way to scale without the bureaucratic weight of asset appraisals.

Hard Assets vs. Soft Assets

Lenders value assets based on liquidity. Real estate is a "hard" asset with high Loan-to-Value (LTV) ratios, often reaching 75% or 80%. Inventory is a "soft" asset and might only net you 50% of its value in credit. If your capital is tied up in unpaid invoices, invoice factoring can act as a strategic bridge. It turns your "soft" receivables into immediate "hard" cash. This allows you to maintain momentum without pledging your long-term fixed assets.

Understanding the Personal Guarantee

The term "unsecured" can be misleading. While you aren't pledging a specific tractor or building, most lenders still require a personal guarantee. This is your legal promise to repay the debt personally if the business cannot. In 2026, you'll encounter two main types: unlimited and limited. An unlimited guarantee puts your personal savings, vehicles, and home on the line. A limited guarantee caps your personal exposure at a specific dollar amount or percentage.

Negotiating these terms is a critical skill for the modern entrepreneur. Seek to include "burn-down" clauses that reduce your personal liability as the business hits specific revenue milestones. Always clarify if the guarantee is "joint and several," which could hold you responsible for the entire debt even if you have partners. Transparency is your best defense. By understanding the fine print of your secured vs unsecured business line of credit, you protect your personal future while fueling your professional one.

Decision Framework: Which Path Matches Your Goals?

Strategy is the bridge between a simple loan and a high-performance growth engine. Choosing a secured vs unsecured business line of credit depends entirely on your immediate objective and your tolerance for risk. You shouldn't just grab the first offer that hits your inbox. You need to align your funding with your specific business lifecycle and the nature of the opportunity in front of you. In 2026, the cost of capital is only one metric; the utility of that capital is what defines your success.

Consider these three high-impact scenarios to determine your best move:

- Scenario A: You're launching a long-term capital project or acquiring a massive equipment haul. A secured line is your defensive anchor here. With rates typically between 8% and 13% APR, the lower cost justifies the 30-day wait for appraisals.

- Scenario B: You've spotted a sudden inventory spike or a short-term marketing blitz that could double your revenue. An unsecured line is your offensive tool. You pay for the 24-hour speed, but the immediate ROI on that marketing spend far outweighs the interest expense.

- Scenario C: Your growth is explosive, but your credit score hasn't caught up to your revenue yet. Revenue-based financing is your bridge. It bypasses hard collateral and credit hurdles to fuel your momentum based on your current cash flow performance.

Before you commit, assess your current asset liquidity with this checklist. Do you have clear title to real estate or heavy machinery? Is your accounts receivable aging report healthy and predictable? Can your business survive a 60-day delay if an appraisal comes in lower than expected? If you answered "no" to these, the agility of an unsecured line is your safest path forward.

Evaluating Your Business Maturity

Startups and fast-growth companies rarely have three years of pristine tax returns or a warehouse full of paid-off equipment. They lean toward unsecured options because they value flexibility over a 2% rate difference. Established firms with heavy machinery or significant real estate holdings should leverage those assets. Your credit history remains a primary driver for your rate, but your business maturity dictates which door is actually open to you. Connect with a growth consultant today to map your maturity to the right credit product.

Matching Funding to the Use of Proceeds

The "Golden Rule" of finance is simple: match your debt duration to the life of the asset. Using a secured line backed by your building to cover next week's payroll is a strategic mistake that puts your foundation at risk. It's an inefficient use of long-term leverage. Instead, use working capital loans for immediate operational needs like payroll or small inventory buys. This keeps your "hard" collateral available for the massive, generational projects that actually require long-term, low-cost financing. Don't trap your best assets in short-term cycles.

Beyond Traditional Lines: Fast Capital with Legacy Funding Advisors

Traditional banking is often too slow for the modern founder. While you weigh the pros and cons of a secured vs unsecured business line of credit, your competition is already moving. Legacy Funding Advisors exists to bridge that gap. We provide the capital you need without the bureaucratic friction that stalls your momentum. We don't just look at a static credit score or a list of physical assets. We look at the heartbeat of your business: your revenue. This focus allows us to act as a savvy financial ally rather than a distant corporate entity.

Our revenue-based funding model offers a 24-hour approval process. This speed allows you to respond to market shifts in real time. You shouldn't have to choose between risking your property and missing an opportunity. We prioritize your current cash flow performance over rigid, outdated metrics. As new regulations like the CFPB's amended Regulation B take effect in June 2026, the lending environment is shifting. Legacy Funding Advisors stays ahead of these changes to ensure your access to capital remains frictionless and transparent. We understand the numbers, but we also understand the struggle of scaling without the right resources.

The Legacy Advantage: Speed and Flexibility

The application process is designed for the high-velocity entrepreneur. You provide minimal paperwork and receive maximum impact. Unlike traditional secured lines that require months of property inspections and legal filings, our approach is built for efficiency. Revenue-based financing naturally adapts to your monthly sales volume. It's a dynamic solution that breathes with your business. If sales dip, your obligation adjusts. If sales soar, your capital remains ready. Experience the Legacy Funding Advisors triad of benefits: our process is fast, our terms are tailored, and our mission is growth-oriented. We remove the barriers so you can focus on your long-term vision.

Taking the Next Step Toward Scalability

Success requires a growth-first mindset. Don't let your funding strategy become a bottleneck. Move from an applicant to a funded partner by following a streamlined path. First, share your basic revenue data through our secure portal. Second, review a customized offer that matches your specific trajectory and use of proceeds. Third, access the capital and start scaling. This isn't just a transaction; it's a strategic alliance for your generational success. Stop letting legacy institutions dictate your pace. Apply for fast business funding today and secure the engine your business deserves in 2026.

Take Command of Your Capital Strategy

Your capital strategy is the blueprint for your business's future. You've seen how the choice between a secured vs unsecured business line of credit dictates whether you play defense with assets or offense with speed. Mastering these nuances allows you to protect your foundation while aggressively pursuing market share. Whether you need the low-cost stability of a secured line for capital projects or the rapid liquidity of an unsecured line for inventory spikes, the right choice keeps you in the driver's seat.

Legacy Funding Advisors serves as your tech-forward ally in this journey. We prioritize your actual cash flow and revenue metrics over rigid, traditional credit scores. With national coverage across the United States and Canada, we deliver the capital you need to scale without the bureaucratic friction of legacy banks. Get the fuel your business requires with funding in as little as 24-48 hours. Don't let outdated requirements stall your momentum.

Secure your business growth with fast, flexible funding from Legacy Funding Advisors.

The market moves fast. Make sure your funding moves faster.

Frequently Asked Questions

Is it harder to get an unsecured business line of credit?

Unsecured lines require higher credit scores and consistent revenue because the lender lacks a physical safety net. While they're harder to qualify for at traditional banks, alternative lenders make them accessible for businesses with strong cash flow. The trade-off for this lack of collateral is usually a more rigorous look at your operational history rather than your physical assets.

What happens if I default on an unsecured business line of credit?

Defaulting triggers immediate collection efforts and potential legal proceedings against your business. Because most unsecured options require a personal guarantee, your personal bank accounts and property could still be targeted by the lender. This is a critical risk factor when weighing a secured vs unsecured business line of credit. Your professional and personal credit profiles will also face long-term damage.

Can I have both a secured and an unsecured line of credit at the same time?

You can absolutely maintain both to create a balanced and resilient capital structure. Use your secured line for predictable, low-cost capital projects like equipment upgrades or real estate. Reserve your unsecured line for rapid-response needs like seasonal inventory spikes or emergency repairs. This dual-track strategy ensures you never sacrifice operational speed for the cost of capital.

How much collateral do I need for a secured business line of credit?

The amount depends on the asset's liquidity and the lender's specific Loan-to-Value (LTV) ratios. Real estate often carries a 75% to 80% LTV, meaning $100,000 in equity might secure an $80,000 line. Inventory or equipment might only net 50% LTV because those assets are harder to liquidate. You must provide enough hard value to cover the lender's risk entirely.

Does a business line of credit affect my personal credit score?

It usually does, particularly during the initial application phase and if you sign a personal guarantee. Lenders typically perform a hard credit pull, which causes a temporary dip in your score. If the lender reports to personal bureaus, your utilization and payment history will impact your personal credit profile. This makes timely repayment essential for your long-term financial health.

What is the typical interest rate difference between secured and unsecured lines in 2026?

In 2026, secured lines typically hover between 8% and 13% APR for well-qualified borrowers. Unsecured lines carry more variance, ranging from 7% for elite credit to 28% for good-to-fair profiles. This spread accounts for the lender's lack of physical collateral. You're essentially paying a premium for speed, agility, and the absence of asset risk on your balance sheet.

Can I get an unsecured line of credit with bad credit?

Traditional banks will likely decline you, but tech-forward alternative lenders focus on your revenue performance instead. If your business shows consistent monthly sales and healthy cash flow, you can qualify for an unsecured line regardless of a low FICO score. These partners value your current growth trajectory and future potential more than your past credit challenges or mistakes.

How quickly can I access funds from an unsecured line of credit?

Funding often occurs within 24 to 48 hours of your initial application. This rapid turnaround is the hallmark of the unsecured model in the modern market. Since there are no property appraisals or title searches to conduct, the underwriting process is purely digital and focused on your real-time data. This speed is vital when you need to jump on a time-sensitive opportunity.