Revenue-Based Financing vs. Merchant Cash Advance: Choosing Your Growth Engine in 2026

Your next capital injection shouldn't feel like a predatory trap. While nearly 1 in 3 small business owners face rejection from traditional banks, the alternative market is booming with opportunities that don't require giving up a single point of equity. To win in 2026, you must master the debate of revenue based financing vs merchant cash advance to avoid the opaque fees that lead to cash flow strangulation. One option aligns with your business velocity. The other prioritizes speed at a potentially steep price.

You likely feel that rigid bank requirements are a relic of the past. We agree that modern founders need capital that moves at the speed of commerce without the friction of legacy institutions. This article promises to help you identify the fastest, most cost-effective funding path to secure immediate liquidity while protecting your margins. We will analyze factor rates, revenue share percentages, and the latest transparency regulations to help you choose the growth engine that preserves your bottom line.

Key Takeaways

- Define the core operational differences between growth-linked capital and the purchase of future receivables.

- Evaluate revenue based financing vs merchant cash advance to choose a structure that matches your specific business velocity.

- Uncover how factor rates and revenue share percentages impact your long term cash flow health and scaling potential.

- Determine which funding engine fits your business model, whether you rely on predictable recurring revenue or high daily transaction volume.

- Streamline your path to capital with a process that prioritizes real time performance over traditional credit scores to secure funding in 24-48 hours.

The Modern Funding Dilemma: Speed, Flexibility, and Growth

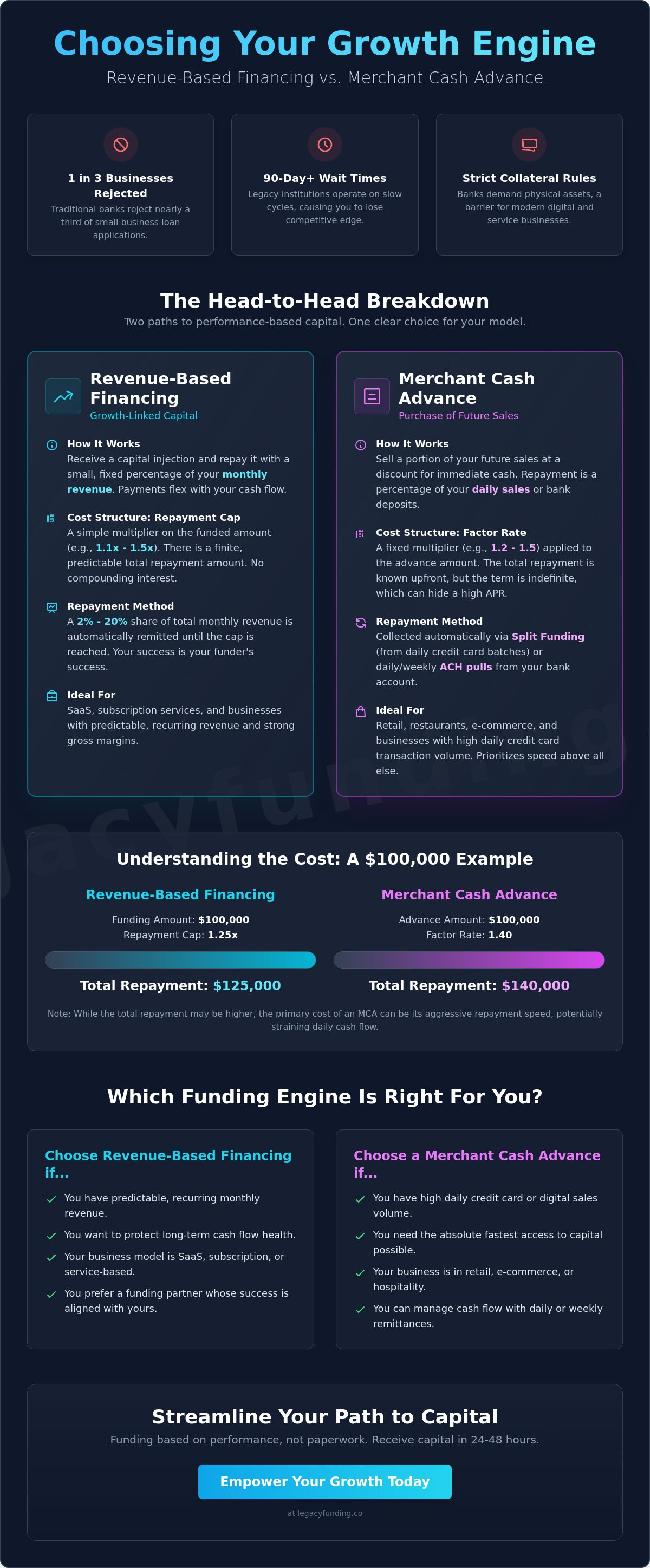

Scaling a business in 2026 requires more than just a vision. It demands a sophisticated capital strategy that moves at the speed of your next breakthrough. You aren't just looking for a loan; you're selecting a growth engine. The choice between revenue based financing vs merchant cash advance often determines whether you accelerate or stall. Revenue-based financing (RBF) acts as growth-linked capital, where repayment scales directly with your monthly income. Conversely, a Merchant Cash Advance (MCA) is technically the purchase of your future receivables. It provides a fast cash injection in exchange for a portion of your daily credit card sales or bank deposits. Modern founders prioritize momentum over everything else. They know that waiting months for a bank decision is the fastest way to lose a competitive edge.

Why Traditional Bank Loans Fail Modern SMBs

Legacy institutions operate on a foundation of friction. They demand high credit scores, deep collateral, and endless months of paperwork. This bureaucratic approach fails the modern founder who needs to move fast. Consider the following bottlenecks that stifle your expansion:

- Asset Prioritization: Banks prioritize personal assets; we prioritize business performance.

- Timeline Mismatch: Banks demand 90-day cycles; you need 24-hour funding.

- Collateral Requirements: Banks require physical collateral; you need capital for digital growth.

Asset-light companies, such as SaaS firms or e-commerce brands, often lack the heavy machinery or real estate banks crave. This mismatch creates a funding gap that stifles innovation. Stop waiting for a "yes" from a distant committee. Pivot to capital that respects your time and your trajectory.

The Shift Toward Performance-Based Capital

Performance-based capital flips the script on traditional lending by aligning your repayment obligations with your actual revenue velocity. When sales are high, you pay more. When things slow down, your payment adjusts downward. This built-in flexibility prevents the cash flow strangulation that often kills otherwise healthy businesses. Most importantly, these tools allow you to preserve your equity. You don't have to sell a piece of your company to fund your next inventory run or marketing blitz. We view financial support as a generational endeavor. It's a partnership designed to build lasting wealth, not just a simple transaction. By choosing correctly in the revenue based financing vs merchant cash advance debate, you secure the liquidity needed to scale without compromise. Empower your business. Protect your equity. Accelerate your growth.

Decoding the Mechanics: How RBF and MCA Actually Work

Master the machinery of your funding to ensure your growth remains sustainable. The core distinction in revenue based financing vs merchant cash advance lies in how the provider calculates and collects their return. Both options prioritize speed. Expect approval cycles within 24-48 hours. These products don't have fixed terms. Your payments breathe with your business performance. If your sales slow down, the amount you remit decreases. This flexibility keeps your operations fluid during seasonal dips.

The Anatomy of Revenue-Based Financing

Revenue-based financing providers underwrite based on your gross margins and recurring revenue metrics. They typically set a repayment cap, which often ranges from 1.1x to 1.5x of the total funding amount. You commit a fixed percentage of your monthly revenue to the provider, usually between 2% and 20%. This model is a favorite for SaaS and subscription-based companies. It rewards high-margin businesses with predictable income streams. Because the payment is a percentage of total revenue, the provider is personally invested in your ability to scale. They win when you win.

The Merchant Cash Advance Engine

A merchant cash advance operates as a purchase of future receivables. You sell a specific dollar amount of your future sales at a discount in exchange for immediate capital. The cost is expressed as a factor rate rather than an interest rate. For example, a 1.2 factor rate on a $100,000 advance means you repay $120,000. This is not a loan. There is no set calendar for repayment. Collection happens through one of two primary methods:

- Split Funding: The credit card processor automatically diverts a percentage of daily sales to the funder.

- ACH Pull: The funder withdraws a set percentage of daily or weekly bank deposits via the Automated Clearing House.

This "remittance" model is the secret to its popularity. Unlike a traditional bank loan with a rigid monthly bill, an MCA fluctuates with your daily transaction volume. If you have a zero-dollar sales day, you remit nothing. This protects your cash flow from the strangulation of fixed debt. If you need a partner who understands these nuances, speak with a consultant today to explore your options.

The Head-to-Head Breakdown: Costs, Speed, and Flexibility

Stop obsessing over your credit score. In the current 2026 landscape, your bank health and cash flow velocity matter more than a three-digit FICO number. Both revenue based financing vs merchant cash advance models prioritize the real-time performance of your business over legacy metrics. While traditional SBA loans often take weeks or months to process, these alternative engines deliver capital in as little as 24 hours. This speed is your competitive advantage. It allows you to seize inventory discounts, launch marketing blitzes, and outpace slower competitors. Approval rates for these products remain high, often between 70% and 85%, compared to the nearly 33% rejection rate at traditional banks. You aren't begging for a favor. You're securing a strategic fuel source for your scaling needs.

Cost Analysis: Factor Rates vs. Revenue Share

Understand your Total Cost of Capital (TCC) before you sign. Revenue-based financing typically uses a revenue share percentage, while merchant cash advances utilize a factor rate. A factor rate is a fixed multiplier of the principal. In 2026, as inflation fluctuates, a fixed factor rate offers cost certainty for high-volume businesses. If your margins are thin, a 1.2x factor rate might be more manageable than a variable 15% revenue share that eats into your gross profits during peak seasons. Match your funding to your margin to avoid debt traps. Calculate the dollar-for-dollar cost. Prioritize transparency. Choose the model that keeps your bottom line healthy as you grow.

Flexibility and the 'Slow Month' Test

Your capital should never strangle your cash flow. The true test of any funding engine occurs during a 30% sales dip. Revenue-based financing handles this naturally; your payment drops automatically because it's a fixed percentage of your actual sales. Merchant cash advances offer similar protection through a reconciliation process. If your daily volume decreases, you can request an adjustment to your remittance to reflect your current reality. This "breathing" mechanism is why these tools are superior to fixed-payment bank loans. Consider these flexibility factors:

- RBF: Payments scale perfectly with monthly income.

- MCA: Daily remittances adjust based on transaction volume.

- Bank Loans: Fixed bills remain due regardless of your revenue.

Don't let a slow month turn into a crisis. Select a growth engine that respects the natural ebbs and flows of entrepreneurship. Partner with a firm that values your long-term impact over a single transaction. Secure your liquidity. Protect your peace of mind. Scale with confidence.

Strategic Selection: When to Choose RBF vs. MCA

Choosing between revenue based financing vs merchant cash advance isn't a coin flip. It's a calculated decision based on your business's current velocity and your 2026 trajectory. You must apply a simple, high-impact triad: Evaluate your cash flow patterns; Decide on your primary growth lever; and Execute with a partner who understands the high stakes of entrepreneurship. Legacy Funding Advisors acts as your high-level consultant. We help you navigate these sophisticated financial waters to ensure you don't just get capital, but the specific engine required for your unique situation.

The RBF Growth Path: Best for Long-Term Scaling

Revenue-based financing is the premier choice for companies with predictable, recurring revenue. As the global RBF market is projected to reach $15.86 billion in 2026, more founders are utilizing this tool to fuel aggressive marketing spend and inventory expansion. This model is particularly effective for SaaS and subscription-based brands that want to avoid the dilution of venture capital. You keep your equity. You keep your seat at the head of the table. By matching the repayment cap to your projected exit strategy, you ensure your cost of capital remains a strategic investment rather than a burden. If your revenue is recurring or subject to high seasonality, RBF provides the breathing room necessary to scale without the fear of cash flow strangulation.

The MCA Tactical Move: Best for Immediate Needs

Merchant cash advances are built for speed and tactical execution. If you have high daily credit card volume and need immediate working capital, an MCA is your most efficient tool. It's the ideal solution for solving payroll gaps, handling emergency equipment repairs, or capturing bulk-buy discounts from suppliers that would otherwise vanish. Many savvy founders use an MCA as a strategic bridge to larger SBA loans or term loans. Because approval rates for MCAs currently sit between 70% and 85%, you can secure liquidity while traditional banks are still reviewing your initial application. This is about removing friction from your growth process. It turns a potential crisis into a competitive advantage.

Don't leave your business scaling to chance. You need a savvy ally who understands the speed of contemporary commerce better than legacy institutions. Contact our advisors today to determine which funding engine will drive your generational endeavor forward.

Empower Your Growth with Legacy Funding Advisors

Building a business is more than a career path. It's a generational endeavor. You aren't just paying bills; you're constructing a legacy that requires a steady, reliable fuel source. Choosing between revenue based financing vs merchant cash advance is a high-stakes decision that defines your scaling potential for years to come. At Legacy Funding Advisors, we move beyond the cold numbers of traditional institutions. We act as your savvy financial ally. We bridge the gap between where you are and where you intend to be. Our process eliminates the bureaucratic friction that stalls innovation. We focus on your cash flow health. We prioritize your business velocity. We invest in your future.

A Streamlined Process for the Modern Founder

Traditional banks are stuck in the past. They demand mountains of paperwork and weeks of your time. We offer a modern alternative designed for the speed of 2026 commerce. Our application is simple. Our impact is immediate. Our commitment is clear. Legacy Funding Advisors provides a 24-48 hour funding commitment to ensure you never miss a market opportunity. This streamlined approach allows you to focus on your core operations while we handle the capital logistics. Our advisors provide direct access to industry expertise. We serve founders across the United States, Puerto Rico, and Canada. We offer tailored solutions for those who value speed and accessibility over red tape.

- Immediate Liquidity: Access capital without giving up a single point of equity.

- Flexible Repayment: Align your financial obligations with your actual revenue performance.

- Rapid Execution: Move from application to funding in days; not months.

Take the Next Step Toward Financial Independence

Stop waiting for a distant committee to validate your vision. The modern founder knows that momentum is the ultimate competitive advantage. Whether you need the recurring-revenue alignment of RBF or the tactical speed of an MCA, the time to act is now. Join the thousands of small and medium-sized businesses that have abandoned legacy banking for a more efficient path. We understand that your business performance is the only metric that truly matters. We look past credit scores to see the real value in your bank deposits and sales volume. Secure your expansion. Protect your bottom line. Fuel your legacy. Apply for Funding in Minutes and discover the difference a true partner makes in your growth journey.

Fuel Your Generational Legacy Today

You now have the insider knowledge to navigate the revenue based financing vs merchant cash advance landscape with total confidence. Choosing the right engine depends on your specific revenue patterns. RBF excels for businesses with predictable recurring income; while an MCA offers the tactical speed needed for immediate operational gaps. Both models prioritize your real-time performance over outdated credit scores. This strategic shift ensures your cash flow remains fluid while you scale toward financial independence. You aren't just borrowing capital. You're selecting a partner invested in your trajectory.

Don't let bureaucratic delays stall your momentum. We serve ambitious founders across the US, Canada, and Puerto Rico with a commitment to speed and transparency. Most of our products require no collateral. We deliver funds in as little as 24-48 hours. You've built the vision. Now, secure the fuel to make it permanent. Your growth is our priority. Let's build something that lasts.

Secure Your Business Funding Now

Frequently Asked Questions

Is revenue-based financing better than a merchant cash advance?

The "better" choice depends entirely on your revenue architecture. Revenue-based financing is superior for SaaS or subscription models with predictable monthly recurring revenue. Merchant cash advances are the strategic choice for retail or restaurants with high-volume daily credit card transactions. Evaluate your sales frequency and choose the engine that aligns with your cash flow velocity. Both options provide the speed traditional banks lack.

Does an MCA or RBF affect my personal credit score?

Most alternative funding solutions prioritize your business bank health over your FICO score. While some providers may perform a soft credit pull, these products typically don't affect your personal credit score or appear on your personal credit report. We focus on your revenue consistency and growth potential. This approach allows you to secure capital without the fear of damaging your personal financial standing.

How quickly can I receive funds from Legacy Funding Advisors?

We maintain a strict 24-48 hour funding commitment for qualified applicants. Our streamlined digital process removes the bureaucratic friction found in traditional institutions. Once you submit your bank statements and complete the application; our advisors work rapidly to finalize your offer. You can move from application to capital in your account in less than two business days. Stop waiting for bank committees; start fueling your expansion today.

What are the minimum requirements for revenue-based funding in 2026?

Qualification for revenue based financing vs merchant cash advance depends on your specific business type. RBF providers in 2026 typically require at least $250,000 in annual revenue and healthy SaaS metrics like low churn. MCA funders often accept businesses with $10,000 in average monthly deposits. Both models require at least six months in business. Focus on maintaining clean bank statements to ensure a seamless approval process.

Can I have both an MCA and a business line of credit simultaneously?

You can absolutely leverage both an MCA and a business line of credit to maximize your liquidity. Many savvy founders use a line of credit for recurring operational costs while using an MCA for one-time tactical moves like inventory bulk-buys. This "stacking" strategy provides a robust financial cushion. Ensure your total daily remittances don't strangulate your cash flow. Consult with our advisors to balance these tools effectively.

What is a factor rate, and how is it different from APR?

A factor rate is a fixed multiplier used to determine the total repayment amount on an advance. Unlike an APR, which calculates interest over time, a factor rate is applied to the principal upfront. For example, a 1.2 factor rate on $100,000 means you repay exactly $120,000 regardless of how long it takes. This provides total cost transparency. It is the standard metric for non-loan commercial transactions in 2026.

Is revenue-based financing considered debt or equity?

Revenue-based financing is structured as a purchase of future receivables, not a traditional debt or equity play. It allows you to access six-figure capital without giving up ownership or a seat on your board. Because it's not a loan, it doesn't carry a traditional interest rate. It's a hybrid tool that provides the flexibility of equity with the control of debt. Secure your scaling needs while preserving your long-term legacy.

What happens if my business has a slow month with an MCA?

Your payments breathe with your sales through a process called reconciliation. If your business experiences a slow month, you can request an adjustment to your daily or weekly remittance. The funder reviews your actual sales and reduces the payment to match your current cash flow. This built-in safety net prevents the cash flow strangulation common with fixed-payment bank loans. It ensures your funding remains a growth engine, not a burden.