Revenue Based Financing for Startups: The 2026 Guide to Non-Dilutive Growth

You didn't build your company to hand over the keys to a board of directors just to keep the lights on. Scaling a startup often feels like a binary choice between stagnating or diluting your vision. You're likely tired of 6-month bank approval cycles and the crushing weight of rigid, fixed payments that ignore your volatile growth months. Our guide to revenue based financing for startups shows you how to unlock capital in as little as 24 to 48 hours while retaining 100% ownership.

We understand that traditional debt and venture capital move too slowly for the modern founder. You need a financial ally that speaks the language of growth metrics, not just financial obligations. This guide covers the mechanics of non-dilutive capital, the impact of AI-driven underwriting, and strategies to scale your revenue without sacrificing your equity or personal collateral. It's time to stop pitching for permission and start funding your own expansion on your own terms.

Key Takeaways

- Master the mechanics of repayment caps and revenue multiples to ensure your cost of capital remains predictable and transparent.

- See why revenue based financing for startups outperforms venture capital when speed and operational autonomy are your top priorities.

- Pinpoint the high-impact metrics, such as gross margins and recurring revenue trends, that drive successful underwriting in 2026.

- Discover how to access tailored capital injections from $10k to $5M to bridge the funding gap without the friction of legacy banking.

The Startup Funding Gap: Why Traditional Capital Fails Modern Founders

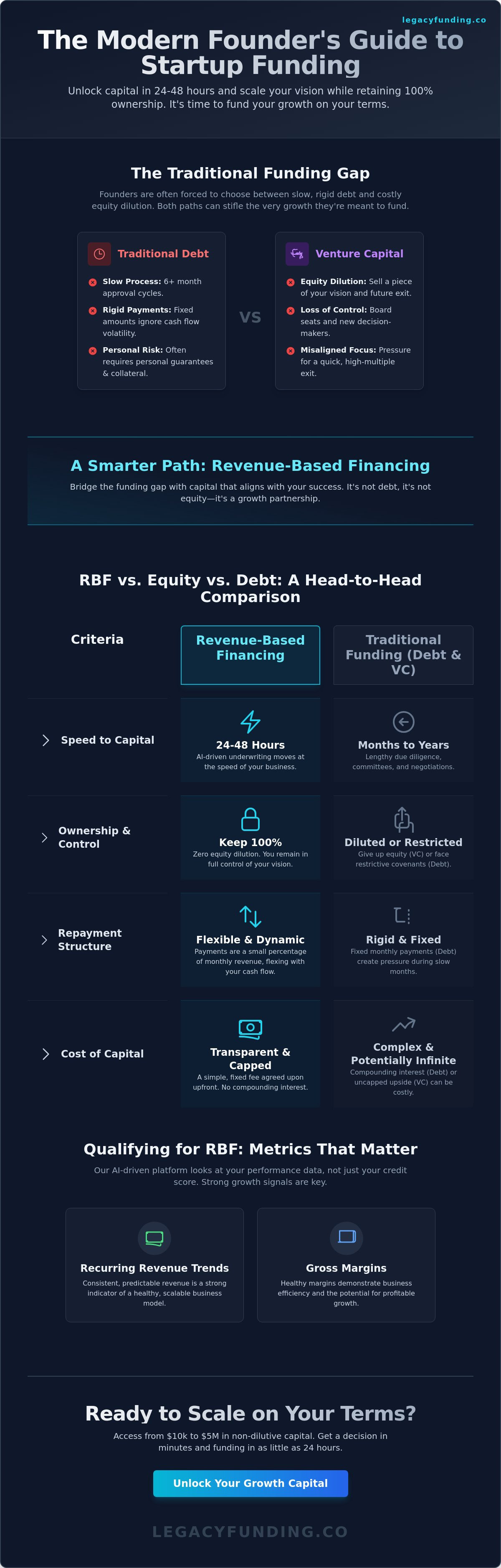

Traditional banking is broken for the modern founder. Legacy institutions demand collateral you don't have and history you haven't written yet. They prioritize credit scores over growth metrics. This creates a friction point that stalls innovation. You need capital that moves at the speed of your dashboard, not the speed of a loan committee. Waiting months for a "maybe" is a luxury your growth schedule can't afford.

Venture capital isn't always the answer either. Selling equity means selling a piece of your vision, your decision-making power, and your ultimate exit. For many, revenue based financing for startups has emerged as the strategic alternative. It bridges the gap between bootstrapping and the next major valuation milestone. It's about maintaining momentum without sacrificing your cap table. You get the capital you need today without compromising the wealth you're building for tomorrow.

The Limitations of Asset-Based Lending

Most software and service startups don't own warehouses or heavy machinery. Traditional lenders struggle to value intellectual property or recurring revenue streams. They often demand personal guarantees that put your personal assets on the line. This risk profile belongs to the old economy. Modern funding should focus on your performance data, not your personal mortgage. Shift your perspective from asset-backed constraints to revenue-backed opportunities. Stop risking your home to fund your server costs.

Equity vs. Non-Dilutive Capital

Preserving your equity is a long-term play for generational wealth. Every percentage point you give away today is a multiplier lost at exit. Using non-dilutive capital allows you to fund customer acquisition and inventory without adding new names to your board. Revenue-based financing functions as a high-performance bridge. It fuels your growth today so you can command a higher valuation tomorrow. You keep 100% control. You keep 100% of the upside. You keep 100% of the decision-making power.

We view funding as a partnership. It shouldn't be a bureaucratic hurdle or an equity grab. It should be a catalyst. In 2026, staying competitive requires liquid capital that scales with your success rather than restricting it. Stop letting traditional bottlenecks dictate your ceiling. Choose a path that aligns your cost of capital with your actual performance. Move fast. Scale responsibly. Retain your vision.

Decoding Revenue Based Financing: Mechanics for High-Growth Startups

Revenue based financing for startups isn't just another line of credit. It's a strategic capital injection that your business repays through a fixed percentage of future gross revenues. Unlike traditional debt, there are no rigid monthly deadlines that ignore your actual cash flow. If your revenue dips during a pivot or a slow season, your payment dips with it. This creates a symbiotic relationship between you and your capital provider. You get the fuel you need; they get a return based on your performance.

One of the most powerful features of this model is the 'No Fixed Term' advantage. Traditional loans have a maturity date that looms over your operations. RBF moves at the speed of your commerce. If it takes eighteen months to reach the repayment cap, the schedule adjusts. If you scale faster, you finish earlier. This flexibility allows you to focus on market share rather than calendar dates. As this funding model matures, understanding the Legal implications of RBF is essential for founders who want to scale safely in a regulated environment.

The Math Behind the Multiple

Traditional loans use compounding interest that can spiral if you aren't careful. Revenue based financing for startups uses a factor multiple instead. This means you know the exact cost of capital from day one. Startups prefer this because it offers total transparency. You don't have to worry about hidden fees or fluctuating rates. The repayment cap is the total ceiling of the obligation. This fixed total cost makes budgeting simple and predictable for your finance team.

Dynamic Repayment Structure

The percentage-of-revenue model creates a natural hedge for your business. Imagine a month where you hit a growth bottleneck or a seasonal slump. A bank would still demand a $10,000 fixed payment regardless of your performance. With RBF, a 5% revenue share simply scales down to match your actual income. This alignment of incentives is powerful. Your funder only sees a return when you succeed. It's a partnership built on growth, not just a transaction built on debt. This structure removes the stress of fixed overhead during volatile scaling phases.

Success in modern commerce requires a capital partner that understands your rhythm. Stop trying to fit your high-growth startup into a legacy banking box. Find out how these mechanics can fuel your specific growth trajectory by speaking with our team today.

RBF vs. Equity vs. Debt: Choosing the Right Fuel for Your Growth Engine

Speed is the ultimate competitive advantage in the startup world. Traditional SBA loans or venture capital rounds often drag on for six months or more. Revenue based financing for startups flips this timeline. You can secure a commitment and see funds in your account in as little as 48 hours. This allows you to capitalize on market opportunities while your competitors are still polishing pitch decks or waiting on bank committees.

Control remains the most significant differentiator. When you take venture capital, you often trade board seats and governance rights for cash. Debt often requires personal guarantees or liens on your intellectual property. RBF requires neither. Your revenue is the only security. You retain 100% autonomy over your daily operations and your long-term exit strategy. It's a professional partnership that respects your role as the primary driver of the business.

Analyzing the cost of capital requires looking beyond the immediate rate. While the effective rate of RBF might seem higher than a bank loan, it's significantly cheaper than giving away 10% of a company that could be worth $100 million. You're trading a small portion of future revenue for the ability to scale today. This preserves your cap table for the moments when equity is truly the only option, such as massive R&D phases or global infrastructure builds.

When to Choose Revenue-Based Funding

This model is built for businesses with high-velocity engines like SaaS and E-commerce. If you have a proven Customer Acquisition Cost (CAC) and high gross margins, RBF is your best tool. Use it for high-ROI activities like digital marketing spend or scaling a sales team. It's the ideal way to turn $1 of capital into $3 of revenue without losing a single share. However, for static needs like heavy machinery or long-term real estate, our other term loans or equipment financing products may offer better alignment.

When to Stick with Venture Capital

Equity is the right choice for R&D-heavy startups that haven't reached consistent revenue yet. If you're building deep tech or pharmaceutical solutions, you need the patient capital that only VC provides. Smart founders often use a hybrid approach. You can stack revenue based financing for startups on top of a seed or Series A round. This extends your runway and allows you to hit higher milestones before your next valuation. It keeps your strategic relationships with equity partners strong while using RBF to handle the heavy lifting of daily operations. Don't let your growth be an "either-or" decision; make it a strategic layer.

Qualifying for Startup RBF: Metrics That Actually Matter

Traditional lenders live in the past. They demand two years of tax returns and a pristine personal credit score before they even consider your business model. In the fast-paced world of revenue based financing for startups, your current performance carries more weight than your history. We prioritize six months of consistent revenue data over two years of stagnant records. If you're generating at least $10,000 in monthly online revenue, you're already in the conversation for meaningful capital. Qualifying for revenue based financing for startups is about showing us your trajectory, not just your balance sheet.

Underwriters look for specific health markers that prove your business is a scaling engine rather than a struggling treadmill. High gross margins are essential because they provide the cushion needed for a revenue-share model to work without choking your daily operations. We treat MRR and ARR as the gold standards for evaluation. Predictable recurring revenue proves that your growth isn't a fluke. We also analyze your customer retention rates. A low churn rate signals a strong product-market fit, which makes your startup a much safer bet for non-dilutive funding. It's about the quality of your income, not just the quantity.

The Modern Underwriting Process

Forget the stacks of paperwork and the weeks of waiting. Modern underwriting relies on direct data integrations with the tools you already use, such as Stripe, Plaid, or QuickBooks. This transparency allows for a 24-hour approval cycle because the numbers speak for themselves. Your real-time cash flow statement is the most important document in your arsenal. While some providers in the market accept credit scores as low as 500, your ability to demonstrate consistent inflows is what truly unlocks the highest funding tiers. Prepare your digital dashboards now to ensure a frictionless application process.

Red Flags to Avoid

Scaling requires discipline and a clear understanding of your risk profile. One major red flag is high customer concentration. If 80% of your revenue comes from a single client, your funding offer will likely reflect that increased risk. We also look for signs of over-leveraging. Taking on a revenue share that is too high can quickly become a bottleneck for your operational liquidity. Avoid inconsistent revenue spikes that lack a clear growth narrative. Stability is always more fundable than erratic surges that you can't explain with data. Ready to see where your metrics stand? Get a performance-based quote and skip the bank lines today.

Scaling at the Speed of Commerce: The Legacy Funding Approach

Growth doesn't wait for a loan committee. When a market opportunity or a sudden inventory need appears, you must move instantly. Legacy Funding Advisors provides a 24-48 hour funding commitment because we understand the high-stakes reality of entrepreneurship. We offer customized revenue based financing for startups that ranges from $10,000 to $5 million. This isn't a generic financial product. It's a capital solution tailored specifically to your Monthly Recurring Revenue (MRR) and your unique growth trajectory.

Our reach is as ambitious as your vision. We empower founders across the United States, Puerto Rico, and Canada with accessible, non-dilutive capital. We don't just look at a static balance sheet; we invest in where your business is going. You're building more than a company. You're building a legacy. We provide the insider knowledge and financial support to make that a reality without the bureaucratic friction of traditional institutions. We speak the language of the modern founder, focusing on your growth metrics rather than just your obligations.

Our Streamlined Application Experience

Scaling should be simple. Our application process involves three clear, actionable steps designed for efficiency. First, connect your real-time data through our secure integrations. Second, receive a transparent offer based on your actual performance. Third, receive your funds and start scaling. There are no hidden fees, no bureaucratic hurdles, and no wasted time. You get direct access to funding advisors who understand the startup grind. We remove the ambiguity and lower the barrier to entry so you can focus on your customers.

Beyond the Transaction: Long-Term Impact

We view financial support as a generational endeavor rather than a simple transaction. A single capital injection won't build a category-defining company. That's why Legacy grows with you. As your revenue scales, we increase your limits to match your new reality. This creates a rhythmic pulse of efficiency that fuels your business at every stage of its lifecycle. We are your tech-forward financial ally, providing the modern key to growth in an outdated financial landscape. Stop letting legacy banks hold you back. Scale your startup today with Legacy Funding Advisors and take the first step toward financial independence.

Take Control of Your Startup’s Future

Ownership is your most valuable asset. Don't sacrifice it to slow-moving institutions or equity-hungry investors when you can fuel growth on your own terms. We've explored how revenue based financing for startups aligns your capital costs with your actual performance. You've seen how non-dilutive funding preserves your cap table while providing the liquidity needed to scale customer acquisition and inventory. Traditional finance is a bottleneck; modern commerce is a race. By choosing a performance-based path, you ensure that your repayment schedule never chokes your cash flow during a pivot or a slow month. This is the strategic key to building generational wealth.

We deliver funds in as little as 24 to 48 hours. You keep 100% of your board seats and autonomy. Our team proudly serves visionary founders across the U.S., Puerto Rico, and Canada. Stop waiting for bank committees to validate your potential and start scaling with a partner that understands your metrics. Secure Your Non-Dilutive Growth Capital in 24 Hours. Your vision deserves a partner that moves as fast as you do. Let's build your legacy together.

Frequently Asked Questions

Is revenue-based financing considered debt or equity?

Revenue-based financing is a non-dilutive capital injection, not equity. You keep every share and board seat while accessing the growth capital you need. It's a performance-linked obligation that prioritizes your autonomy and long-term ownership. Unlike venture capital, there's no permanent loss of your company's future value.

How much does revenue-based financing typically cost startups?

The cost is determined by a fixed repayment multiple rather than a compounding interest rate. You'll know the total ceiling of your obligation before you sign any documents. This transparency helps you calculate the exact ROI on every dollar deployed. It removes the guesswork associated with fluctuating rates or hidden banking fees.

Can I get revenue-based funding if my startup isn't profitable yet?

Profitability isn't a requirement for revenue based financing for startups. We focus on your gross revenue and growth trajectory rather than your net bottom line. If your top-line data shows consistency and healthy gross margins, you can qualify regardless of your current burn rate. This is ideal for SaaS and e-commerce brands scaling toward their next milestone.

What happens to my payments if my startup has a bad sales month?

Your payments decrease automatically during slow months. Because the repayment is a fixed percentage of your actual sales, the burden lightens whenever your revenue dips. This structure provides a natural hedge and protects your cash flow during pivots or seasonal fluctuations. It's a flexible system that adapts to the reality of your business.

How fast can I actually receive funds for my startup?

You can receive funds in as little as 24 to 48 hours. Our streamlined digital process removes the bureaucratic delays and paperwork found at traditional banks. Connect your revenue data, review your customized offer, and fuel your growth initiatives immediately. Growth won't wait, and neither should your capital.

Do I need to provide a personal guarantee for RBF?

Most revenue based financing for startups does not require a personal guarantee. We secure the funding against your future revenue streams rather than your personal assets. This keeps your home and personal savings safe while you scale your vision. It's a professional partnership based on business performance, not personal liability.

Can I use RBF alongside an existing SBA loan or line of credit?

You can absolutely stack RBF with other financial products like SBA loans or business lines of credit. Many founders use it to fund high-ROI activities, such as digital marketing spend, that traditional lenders won't cover. It's a strategic way to bridge the gap between major funding rounds without adding more debt-service pressure.

Is there a prepayment penalty if I want to clear the obligation early?

There are typically no prepayment penalties because the total cost of capital is fixed from the start. Clearing the obligation early simply frees up your future revenue streams sooner. It's a flexible tool designed to match the speed of your success. You have the freedom to manage your capital structure as your revenue scales.