How to Get a Second Business Loan: The 2026 Strategic Blueprint

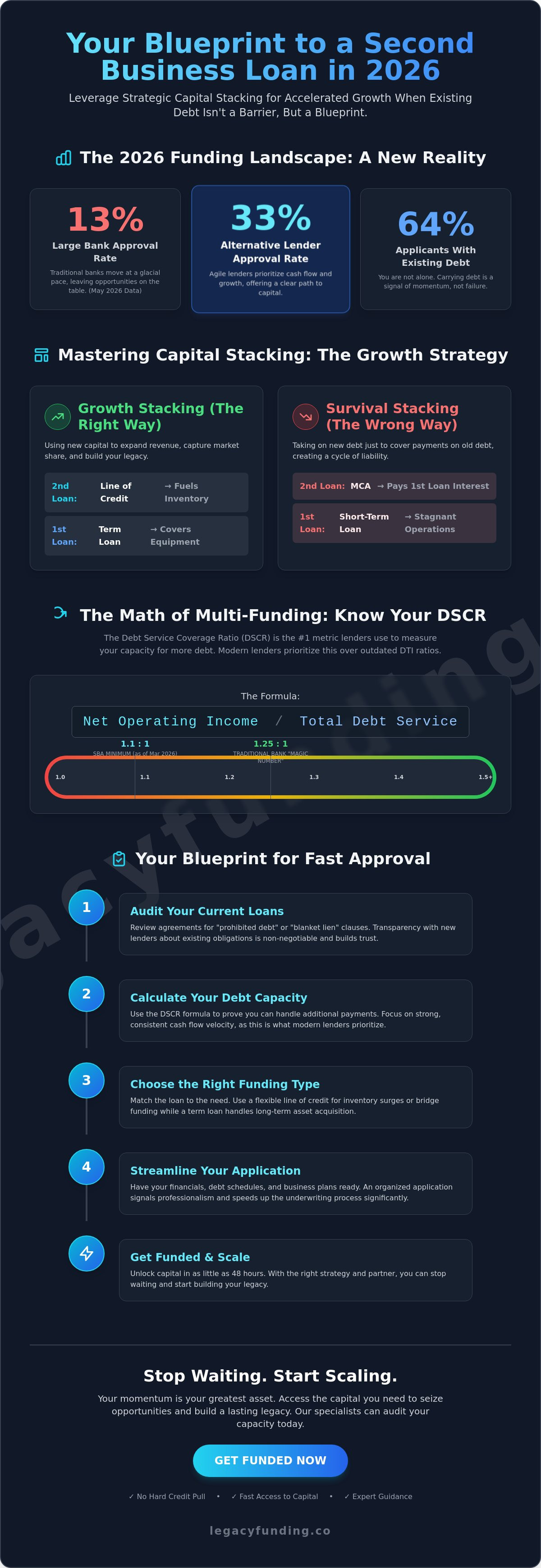

Your existing debt isn't a barrier; it is a blueprint for your next expansion. Most founders believe their first balance sheet obligation acts as a ceiling, yet the reality of 2026 proves that getting a second business loan is about cash flow velocity rather than debt avoidance. You know the frustration of watching traditional banks move at a glacial pace while your growth opportunities vanish. With large bank approval rates stalled at 13% as of May 2026, you're right to feel that the old system is broken.

You deserve a clear path to capital that respects your momentum. This strategic blueprint teaches you how to master capital stacking and qualify for additional funding even with current liabilities. You'll learn to use your revenue as leverage to secure fast access to capital with no hard credit pull. We will break down the new 1.1:1 debt service coverage ratios, explore how to navigate the March 1, 2026 SBA citizenship requirements, and show you exactly how to bypass the red tape. It's time to stop waiting and start scaling. Follow these steps to Get Funded and build your legacy.

Key Takeaways

- Leverage strategic capital stacking to accelerate your growth metrics instead of letting existing debt stall your momentum.

- Navigate the complexities of getting a second business loan by mastering the Debt Service Coverage Ratio (DSCR) lenders use to measure your capacity.

- Audit your current loan agreements for "prohibited debt" clauses to ensure your path to additional funding remains clear.

- Compare high-impact funding options like business lines of credit to find the most flexible layer for your operational needs.

- Streamline your approval process to unlock capital in under 48 hours and keep your scaling journey on track.

Can You Have Multiple Business Loans? Understanding the 2026 Landscape

Carrying debt is not a sign of failure. It is often a signal of momentum. Data shows that 64% of business loan applicants already have existing debt on their books. In the 2026 financial environment, the concept of "loan stacking" has evolved from a desperate survival tactic into a sophisticated growth strategy. Stacking is the intentional use of multiple types of business loans to accelerate your scaling timeline. It allows you to fuel different parts of your operation simultaneously without waiting years for a single balance to hit zero.

The 2026 landscape favors the agile. While large banks approved only 13% of applications in May 2026, alternative lenders have stepped in with approval rates closer to 33%. This shift away from rigid, one-and-done banking means getting a second business loan is now a standard move for high-growth firms. Your focus must remain on "growth stacking." This means using fresh capital to expand revenue or capture market share. This stands in contrast to "bad stacking," which involves taking new debt just to cover old interest payments. Real success is about building a legacy. It's about creating a business that outlasts its initial credit lines and generates generational wealth through smart leverage.

The Legality and Ethics of Second Loans

You can legally hold multiple loans, but you must navigate the hierarchy of repayment. Most initial lenders secure their interest with a "blanket lien" on your business assets. When you apply for additional capital, the new lender typically takes a "second position." This means they are second in line to get paid if the business dissolves. Transparency is your greatest asset here. Disclose all existing debt clearly. Hidden debt is the fastest way to get blacklisted by top-tier funding partners. Professional lenders respect a founder who understands their debt capacity and manages it with precision.

Common Scenarios for Additional Funding

Timing often dictates the need for more capital. Waiting for one loan to finish before starting the next can kill your momentum. Consider these three high-impact scenarios:

- Inventory Surges: Use a business line of credit to stock up for seasonal demand while your primary term loan handles long-term equipment costs.

- Opportunity Costs: Don't let a prime real estate deal or a competitor's liquidation pass you by because your current capital is already deployed.

- Bridge Funding: Secure fast working capital to maintain operations while you wait for the extensive 60-day underwriting process of a large SBA 7(a) loan.

Master these scenarios to keep your business moving at the speed of modern commerce. Unlock your potential and Get Funded today.

The Math of Multi-Funding: Calculating Your Debt Capacity

Numbers tell the ultimate story of your business scale. Lenders in 2026 don't just look at what you owe; they look at what you keep. When you're getting a second business loan, the most critical metric is your Capacity. This is one of the traditional 5 Cs of credit, and it measures your ability to handle additional debt without suffocating your operations. In a year where 31% of small business owners cite cash flow as their top concern, proving your capacity is the only way to secure a "yes" from a high-level funding partner.

Traditional institutions often rely on Debt-to-Income (DTI) ratios, but this is a legacy metric. Modern revenue-based lenders prioritize cash flow velocity. They want to see that your daily or weekly revenue can easily absorb a new payment. While historical programs like SBA second draw loans once provided a safety net, today's market requires you to prove your historical and projected performance. If you aren't sure where your numbers stand, you can speak with a specialist to audit your current capacity.

Calculating Your DSCR Like a Pro

The Debt Service Coverage Ratio (DSCR) is the primary lens through which lenders view your second application. The formula is simple: divide your Net Operating Income (NOI) by your Total Debt Service. As of March 1, 2026, the SBA requires a minimum DSCR of 1.1:1 for small 7(a) loans. However, traditional banks still hunt for the "magic number" of 1.25:1. If your ratio is lower, alternative lenders often use a different multiplier. They focus on your total monthly revenue to determine if you can handle a second layer of capital.

The Impact of Credit Scores on Second Applications

Expect your personal credit score to fluctuate after your first funding round. Increased utilization and recent inquiries often cause a temporary dip. While traditional banks demand a 680 or higher, the 2026 landscape is more flexible. Online lenders now accept scores as low as 550 if your cash flow is strong. Legacy Funding prioritizes your growth metrics over a hard credit pull. This protects your score while you shop for the capital you need to scale. Focus on maintaining a clean repayment history on your first loan; this is the strongest signal of reliability you can send to a second-position lender. Master your math, protect your score, and Get Funded.

Strategic Stacking: Comparing Your Second Loan Options

Choosing the right funding vehicle is as important as the capital itself. When you're getting a second business loan, you need a product that complements your existing debt rather than competing with it for oxygen. Strategic stacking isn't about reckless borrowing. It is about matching the right capital to the right growth metric. Traditional Term Loans offer solid long-term ROI, but they're often the hardest to stack due to restrictive covenants and slow bank approval rates that averaged only 13% to 18% in early 2026. In contrast, a Business Line of Credit acts as the ultimate flexible layer. It fills operational gaps without the commitment of a lump-sum payout.

For high-volume businesses, Merchant Cash Advances (MCAs) provide speed-focused capital. They bypass the slow underwriting of traditional banks. If your growth depends on immediate inventory or marketing spend, these tools are your leverage. They focus on your sales velocity rather than just your balance sheet. This allows you to scale without the friction of a legacy financial institution. Use these tools to bridge gaps and accelerate your timeline. It's about maintaining momentum while your competitors are stuck in a 60-day underwriting cycle.

When to Choose an SBA as a Second Loan

You can hold multiple SBA loans simultaneously. The aggregate limit remains $5 million. Many savvy founders use an SBA 504 for real estate while maintaining an SBA 7(a) for working capital. However, remember the timeline reality of 2026. With the prime rate sitting at 6.75% and SBA 7(a) variable rates reaching up to 13.25%, these are cost-effective but slow. They aren't built for market opportunities that expire in 48 hours. If you need immediate liquidity, an SBA loan is rarely the right second layer. It's a foundational tool, not a tactical one.

Revenue-Based Financing: The Modern Founder's Choice

Revenue-Based Financing (RBF) is the strategic blueprint for the modern entrepreneur. It stacks seamlessly because it ignores traditional debt-to-income ratios. Instead, it focuses on your daily sales velocity. Payments are flexible; they scale down if your revenue dips and accelerate when you win. This non-dilutive capital is the preferred choice for founders who want to pursue getting a second business loan without the friction of a hard credit pull. It's fast, accessible, and designed for the modern scaling journey. Unlock your next phase and Get Funded.

Your Blueprint for Approval: 5 Steps to Securing Additional Capital

Success in getting a second business loan depends on preparation, not persuasion. You need a tactical approach that proves your business can handle more weight. While 52% of small businesses receive the full amount they request, the remaining 48% often fail due to poor documentation or restrictive existing contracts. Follow this five-step blueprint to move from application to funding without the typical friction of traditional banking.

- Step 1: Audit your existing loan agreements. Look for "negative covenants" or "prohibited debt" clauses. Some traditional lenders forbid you from taking on "junior debt" or additional liens. Breaking these can trigger a technical default on your first loan.

- Step 2: Optimize your cash flow statements. Lenders in May 2026 are scrutinizing the last 90 days of activity more than your 2024 tax returns. Highlight your "excess capacity" by cleaning up non-essential overhead 30 days before you apply.

- Step 3: Define the ROI. Be specific about the "use of proceeds." Lenders love to fund a $150,000 inventory surge that has a guaranteed 20% margin increase. They are less likely to fund "general working capital" for a business already carrying debt.

- Step 4: Choose a specialized lender. Seek out partners who understand "second position" or revenue-based capital. These lenders focus on your growth metrics rather than trying to take the first lien away from your primary bank.

- Step 5: Prepare your Blueprint document. Create a concise, one-page growth plan. Show exactly how the new funds will accelerate your revenue and improve your debt service coverage ratio.

Documentation: Beyond the Basics

Banks are stuck in the past. They want tax returns that are 18 months old. Modern lenders want to see the pulse of your business today. Provide 4 to 6 months of recent bank statements to prove your current revenue velocity. Your Profit and Loss (P&L) statement must show a clear upward trajectory to justify the additional leverage. Over the last 180 days, my business has increased its gross monthly revenue by 22% through strategic client acquisition and optimized pricing models.

Avoiding the 'Hard Pull' Trap

Protect your score at all costs. Every hard inquiry can drop your personal credit score by 5 to 10 points. If you apply to multiple lenders simultaneously, you might disqualify yourself before you even see an offer. Look for lenders who offer "soft pull" pre-approvals. This allows you to see your funding capacity without damaging your credit profile. Legacy Funding provides a clear path to capital without the hard credit pull anxiety. Apply for your blueprint audit today and unlock your next stage of growth with confidence.

Unlock Growth and Get Funded with Legacy Funding Advisors

Legacy Funding is the savvy alternative to the red tape of traditional banking. Traditional institutions are stuck in the past. They see a balance sheet and think risk. We see a balance sheet and think leverage. If you're serious about getting a second business loan, you need a partner that moves at the speed of your ambition. We deliver capital in 24 to 48 hours. No waiting for 60-day underwriting cycles. No endless paperwork. We prioritize your future receivables and growth potential over historical credit scores. This is the modern key to capital.

Your business is a generational endeavor. It deserves a financial ally that understands the grit of entrepreneurship. We bridge the gap between high-stakes finance and your aspirational reality. By focusing on growth metrics rather than just debt obligations, we empower you to pursue market opportunities that your competitors can't reach. Our process is bold. It is transparent. It is disruptive. We provide the capital you need to accelerate your timeline and secure your market position. We speak the language of the modern founder.

The Legacy Difference: No Personal Guarantees

We believe in protecting your personal assets while you scale your business legacy. Our "No Personal Guarantee" policy ensures that your private life remains separate from your professional expansion. We structure revenue-based financing to match your specific industry cycle. Whether you're in retail, manufacturing, or tech, our capital fits your cash flow. We offer speed. We offer transparency. We offer entrepreneurial growth. Our commitment to a "No Hard Credit Pull" approach means you can explore your options without damaging your score.

Ready to Accelerate? Your Next Step

The path to your next capital injection is simple. Our online application takes minutes, not weeks. You won't face the red tape found in traditional banking. You'll consult with our advisors to build a custom funding blueprint designed for your specific scaling needs. In May 2026, 93% of small businesses expect growth. Don't let a lack of capital hold you back from being part of that statistic. While large banks only approve 13% of applications, we focus on the founders ready to win. Unlock your next round of capital—Get Funded today and build the legacy your hard work deserves.

Scale Your Vision with Strategic Capital

Your growth strategy shouldn't be limited by a single credit line. In May 2026, 93% of small businesses expect to expand. Getting a second business loan is the most efficient way to join them. You now have the blueprint to navigate this landscape. Focus on growth stacking rather than survival debt. Audit your existing contracts for restrictive covenants. Master your 1.1:1 debt service coverage ratio to prove your capacity. Don't let the 13% approval rate at large banks dictate your timeline. You have the tools to bypass the red tape and lead your industry.

Legacy Funding is your ally in this high-stakes environment. We provide the speed and transparency that traditional institutions lack. We offer a 24 to 48 hour funding process to keep your momentum high. You can explore your capital options with no hard credit pull for initial offers and no personal guarantee required for many products. We look at your future receivables because your potential is more important than your past. It is time to unlock your next level of success.

Get Funded: Apply for Your Second Business Loan in Minutes

Your business legacy is waiting. Take the first step toward total financial freedom today.

Frequently Asked Questions

Can I get a second business loan with the same lender?

Yes, many lenders allow you to secure additional funding once you have paid down a specific portion of your original balance. Typically, you must have cleared at least 50% of your current loan before a lender will consider an "add-on" or a renewal. This is often the fastest route because the institution already has your financial profile on file. If your growth has outpaced their internal lending limits, you may need to look toward a specialized second-position partner.

What is 'stacking' in business lending, and is it dangerous?

Stacking is the strategic use of multiple funding sources to accelerate your business growth. It is only dangerous when used for "bad stacking," which involves taking new debt to pay off old interest. If the new capital generates a higher ROI than the cost of the debt, it's a powerful tool for scaling. In 2026, savvy founders use stacking to capitalize on market opportunities that their first loan can't cover.

Will a second business loan hurt my personal credit score?

It depends on the lender's inquiry process and your repayment consistency. Traditional bank applications involve a hard credit pull that can drop your score by 5 to 10 points. Legacy Funding avoids this risk by offering initial funding assessments with no hard credit pull. While getting a second business loan increases your total debt, consistent on-time payments will eventually strengthen your credit profile and overall borrowing capacity.

How much can I borrow if I already have an existing business loan?

Your borrowing limit is determined by your Debt Service Coverage Ratio (DSCR) rather than a flat dollar amount. As of March 2026, most lenders require a DSCR of at least 1.1:1. This means your net operating income must be 110% of your total debt payments. If your cash flow supports the new obligation, you can often secure additional capital equivalent to 10% to 20% of your annual gross revenue.

Can I have two SBA loans at the same time?

Yes, you can hold multiple SBA loans as long as the total aggregate amount does not exceed $5 million. Many entrepreneurs hold an SBA 504 loan for real estate while utilizing an SBA 7(a) loan for working capital. Keep in mind that as of March 1, 2026, 100% of the business must be owned by U.S. citizens or nationals to remain eligible for these programs. Lawful Permanent Residents are no longer eligible for SBA ownership as of that date.

What happens if my existing loan has a blanket lien on my assets?

A blanket lien gives your first lender the primary right to your assets if you default. When getting a second business loan, the new lender typically takes a "second position" on those same assets. They understand they are second in line for repayment. Some traditional bank contracts contain "negative covenants" that prohibit additional liens, so you must audit your current agreements before signing for new capital.

How fast can I get a second loan through Legacy Funding Advisors?

We deliver funds in as little as 24 to 48 hours. Our tech-forward underwriting process prioritizes your recent revenue velocity over outdated tax returns. While large banks have approval rates as low as 13% as of May 2026, our streamlined system focuses on speed and accessibility. We help you move from application to capital injection without the friction of a legacy financial institution.

Is there a limit to how many business loans one company can have?

There is no legal limit to the number of loans a business can hold. The only real limit is your cash flow capacity and your ability to maintain a healthy debt-to-income ratio. If your business generates enough revenue to maintain a healthy DSCR, you can continue to stack capital layers. In 2026, 52% of businesses that apply for funding receive their full requested amount, proving that multiple loans are a standard part of modern scaling.