How Does Revenue-Based Lending Work? The Modern Founder’s Guide

Giving away a chunk of your company just to bridge a temporary cash flow gap isn't a strategy; it's a sacrifice. Most founders reach a point where they need capital to scale, yet traditional options feel like a trap. You're either diluting your ownership for venture capital or suffocating under the rigid monthly payments of a legacy bank loan. If you've been asking how does revenue based lending work, you're already looking for a smarter, more agile path to growth.

You've worked too hard to build your brand to let a lender or investor dictate your future. You deserve a financial partner that understands the rhythm of your sales and rewards your performance. We promise to show you how to unlock fast capital that aligns with your revenue, ensuring you retain 100% ownership while accessing the fuel your business needs. This guide breaks down the mechanics of modern financing, from understanding factor rates to navigating the 2026 CFPB reporting changes, so you can scale with confidence and speed.

Key Takeaways

- Replace rigid credit scores with cash-flow-based funding that treats your future sales as a valuable asset.

- Master the technical mechanics of how does revenue based lending work to leverage factor rates instead of restrictive fixed interest.

- Bypass the 90-day SBA wait times and access capital in 48 hours while maintaining 100% ownership and control.

- Identify the specific revenue and time-in-business benchmarks required to qualify for a modern capital injection.

- Align with a tech-forward financial ally to bridge the gap between current operations and generational scaling.

The Evolution of Business Capital: What is Revenue-Based Lending?

Traditional finance was built for factories and physical inventory. It wasn't built for the speed of modern commerce. Most founders find themselves stuck between slow-moving banks and equity-hungry investors. If you're asking how does revenue based lending work, you're looking for a smarter way to scale. This model represents a fundamental shift from credit-score-based lending to cash-flow-based funding. It prioritizes your current momentum over your past history.

At its core, Revenue-based financing is the purchase of a specific amount of your future sales at a discount. You receive a lump sum of capital today in exchange for a percentage of your future revenue. This isn't a traditional loan; it's technically a 'purchase and sale' agreement. By selling a portion of your future receivables, you gain immediate access to the fuel your business needs. This model delivers a core triad of benefits: speed, flexibility, and empowerment. It puts you back in control of your company's trajectory.

Why Traditional Loans Fail Modern Founders

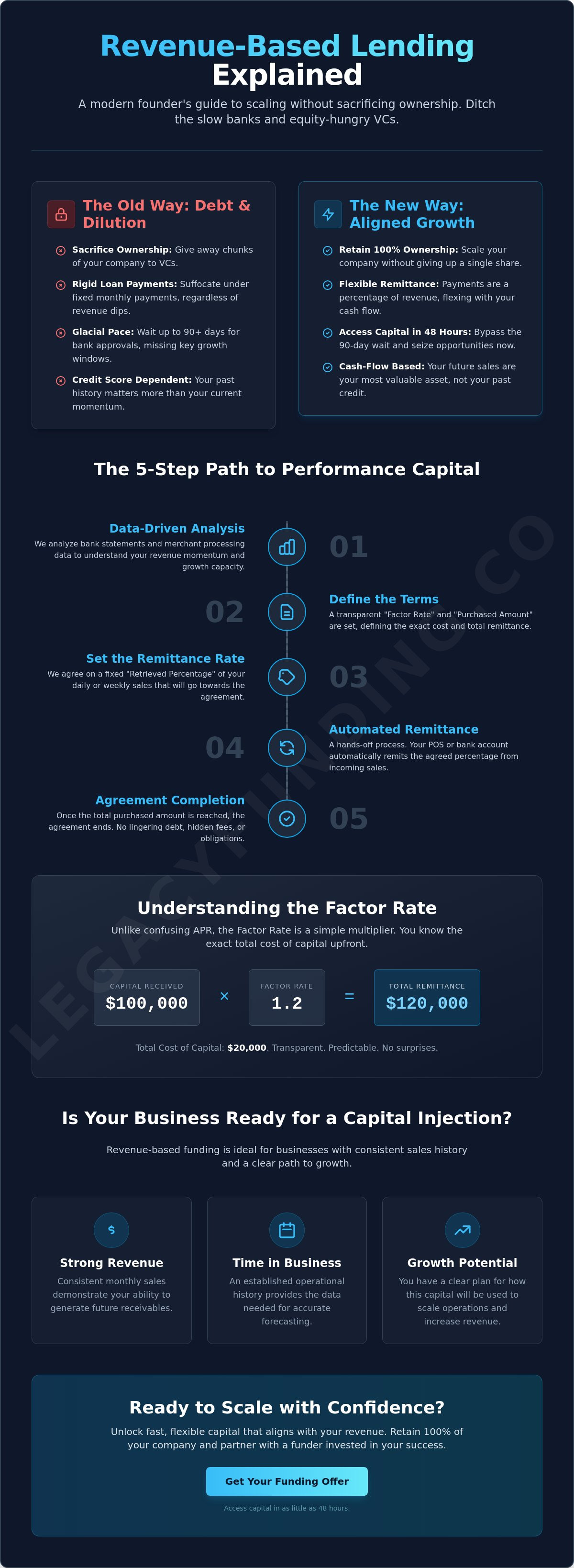

Legacy banks move at a glacial pace. Growth opportunities are often gone by the time a bank committee reaches a decision. Beyond the speed issue, banks rely on strict collateral requirements. They want to see buildings or equipment. This approach excludes asset-light, high-growth digital businesses that hold their value in intellectual property. Traditional debt also carries fixed monthly payments. These payments ignore the reality of fluctuating revenue. If you have a slow month, the bank still demands the same high payment. This creates unnecessary stress during natural business cycles.

The Core Philosophy: Aligned Interests

Understanding how does revenue based lending work is the first step toward financial independence. This model transforms the funder into a growth partner. The funder only succeeds when your business generates revenue. This alignment changes the dynamic from a distant creditor to a confident partner. Because there are no fixed maturity dates, the relationship is based entirely on your actual performance. If your sales dip, the amount you pay back that month dips too. It's a responsive system that protects your cash flow during lean times and accelerates during growth spurts.

Revenue-based financing is a performance-linked capital injection for businesses that want to scale without the friction of traditional debt or equity dilution.

The Mechanics of Momentum: How Revenue-Based Lending Works

Understanding the engine under the hood is vital for any founder looking to scale. You aren't just taking a loan; you're entering a performance-based partnership. To truly grasp how does revenue based lending work, you must look at the five-step journey from your initial application to the final remittance. It is a streamlined process designed for the speed of modern commerce.

- Step 1: Data-Driven Analysis. We don't just look at a credit score. We analyze your historical and projected revenue through bank statements and merchant processing data to determine your true capacity for growth.

- Step 2: Defining the Terms. We determine a "Factor Rate" and a total "Purchased Amount." This establishes exactly how much capital you receive and the total amount you will remit from future sales.

- Step 3: Setting the Remittance Rate. We agree on a "Retrieved Percentage," often called a remittance rate. This is the fixed percentage of your daily or weekly sales that will be used to fulfill the agreement.

- Step 4: Automated Remittance. The process is hands-off. Your point-of-sale system or bank account automatically remits the agreed percentage from your incoming sales.

- Step 5: Agreement Completion. Once the total purchased amount is reached, the agreement ends. There are no lingering obligations or hidden fees.

This model is gaining massive traction across the country. Even government entities like the Washington State Department of Commerce have recognized the value of revenue-based models for supporting seasonal and high-growth businesses. It provides a level of security that traditional debt cannot match.

Understanding the Factor Rate

Factor rates are not interest rates. They are simple multipliers. If you receive $100,000 with a 1.2 factor rate, your total remittance amount is $120,000. This provides total transparency. You know the exact cost of your capital before you sign. Contrast this with traditional APR, which can fluctuate or become confusing over long amortization schedules. With a factor rate, the math is clear and the cost is fixed. If you want to see how these numbers apply to your specific situation, speak with a growth advisor today.

The Remittance Process Explained

The "Retrieved Percentage" is what makes this model truly flexible. Imagine your remittance rate is 8%. On a day you do $10,000 in sales, you remit $800. If you have a slow day with zero sales, you remit zero dollars. This protects your cash flow during lean periods. The entire system relies on tech-forward integration. It connects directly to your bank account or payment processor. This removes the administrative burden of writing checks or managing manual transfers. It allows you to focus entirely on scaling your operations.

RBF vs. The Status Quo: Why Founders Are Ditching Traditional Debt

Traditional financing often forces you to choose between your ownership and your sanity. You either surrender a piece of your soul to venture capitalists or chain yourself to the rigid demands of a legacy bank. Understanding how does revenue based lending work reveals a third path. It's a path built on a triad of freedom: no dilution, no collateral, and no rigid terms. You keep your board seats. You keep your equity. Most importantly, you keep your peace of mind.

The psychological relief of this model is its greatest hidden asset. When you have a slow month, you don't have to panic about a fixed bank payment. Your remittance shrinks automatically with your sales. This flexibility allows you to breathe, pivot, and plan for the next growth spurt without a creditor breathing down your neck. It’s a partnership that respects the natural ebb and flow of entrepreneurship. You focus on the numbers that matter while we provide the liquidity that makes them possible.

Equity is the Most Expensive Capital

Giving away 10% of your company for a quick cash injection is a permanent loss. That equity is gone forever, along with all future dividends and exit value. Revenue-based financing acts as the perfect bridge. It provides the capital to reach your next milestone without sacrificing your cap table. You pay a one-time cost via a factor rate, and once the agreement is fulfilled, the obligation is gone. You retain 100% of your business and 100% of your future upside. It's a generational strategy, not just a transaction.

The Agility Factor: Speed as a Competitive Advantage

In the modern market, timing is everything. A 90-day wait for an SBA loan is an eternity when a competitor is moving in on your territory. Revenue-based options can put capital in your hands in as little as 48 hours. This speed allows for inventory bulk-buying, sudden marketing blitzes, or the ability to secure a major contract on short notice. Don't let a slow approval process kill your momentum. We move at the speed of your ambition.

Founders often worry about the higher factor rate compared to traditional interest. However, a slightly higher cost of capital is always cheaper than a lost contract or a missed market window. Speed is a feature, not a bug. It’s about the ROI on that capital, not just the price of the money itself. When the iron is hot, you need a partner who can help you strike immediately. Scale fast. Stay in control. Build your legacy on your own terms.

Qualifying for Capital: Is Your Business Ready for a Revenue-Based Advance?

Traditional banks focus on your past. We focus on your momentum. Qualifying for a revenue-based advance is about demonstrating consistent performance rather than just having a long history. Most funders look for at least six months of operating history to establish a baseline of reliability. If your business generates at least $10,000 in verifiable monthly revenue, you are already in the top tier of candidates for rapid funding. This model rewards your current success by giving you the tools to multiply it.

By mastering how does revenue based lending work, you'll realize that your sales data is your most valuable asset. While your personal credit score provides a baseline of trust, the true driver of the approval is your business's cash flow. This model is built for high-margin, high-volume, or seasonal businesses that need to move faster than a traditional bank allows. It turns your daily deposits into a bridge toward your next major milestone. You aren't just a credit score to us; you are a growth partner with a track record of results.

The Application Checklist

Our process removes the friction of traditional lending. You won't need to dig through years of tax returns or provide personal collateral like your home. To secure an offer, you generally need to provide three to six months of recent bank statements showing consistent deposits. You will also need basic business information, including your EIN and ownership details. Finally, have a clear objective for the capital, such as inventory purchase or marketing expansion.

Having a clear plan for how the capital will generate more revenue is essential. It proves you aren't just looking for a lifeline; you're looking for a launchpad. High-margin businesses like SaaS or professional services find this model exceptionally useful because the cost of capital is easily absorbed by their profit margins. It provides a safety net that traditional debt simply cannot offer. Your business performance is the collateral. Your future sales are the security.

The 24-48 Hour Approval Window

Legacy Funding Advisors leverages tech-forward integrations to bypass the red tape that slows down legacy institutions. You don't need a 50-page business plan or a complex pitch deck to get a decision. We connect directly to your merchant processing or bank data to verify your performance in real-time. This efficiency allows us to provide approvals within a 24 to 48-hour window, putting capital in your hands while the opportunity is still fresh.

Waiting for a cash flow crunch to occur is a common mistake. Proactive founders apply while their growth metrics are strong to ensure they always have the liquidity to strike when an opportunity arises. Secure your capital before you need it to maintain your competitive edge. Check your eligibility for a performance-based advance today.

Scaling with Legacy Funding Advisors: Your Partner in Rapid Growth

Legacy Funding Advisors serves as the ultimate bridge to your financial independence. We have dismantled the traditional barriers that keep founders from reaching their full potential. By now, you understand how does revenue based lending work as a tool for momentum rather than a burden of debt. Our role is to act as a high-level consultant and a savvy ally in your corner. We provide the insider knowledge necessary to bridge the gap between complex finance and your specific business goals.

We treat every engagement as a generational endeavor. This isn't about a single transaction; it's about building a foundation that lasts for decades. Our model ensures you retain 100% control of your vision while receiving the capital injection needed to scale. Because we respect the pace of your industry, we've optimized our systems to deliver funds within 24 to 48 hours. This speed is your competitive advantage in a market that never sleeps. You move fast, and we move faster to keep your trajectory climbing.

The Legacy Difference: Tech-Forward and Founder-First

Our process is built for the speed of modern commerce. We utilize tech-forward data analysis to see the true health of your business. While legacy banks are obsessed with collateral and credit history, Legacy Funding Advisors focuses on your growth metrics and cash flow. This founder-first mentality removes the ambiguity from the application process. Experience the relief of a partnership that scales with your success. As your revenue increases, your access to our suite of products becomes even more seamless.

Take the Next Step Toward Your Business Peak

Stop letting outdated banking requirements hold your business back. The modern founder knows that agility is the key to market dominance. Our application process is designed to be low-barrier and high-impact. We remove the friction, lower the barrier to entry, and provide a clear path to results. It's time to trade rigid payments for performance-aligned growth. Our impact is long-term, and our commitment to your expansion is absolute. Reach your peak performance without sacrificing the equity you've worked so hard to build.

Build your legacy. Scale your operations. Retain your freedom.

Apply for Revenue-Based Funding in Minutes

Claim Your Future and Scale on Your Own Terms

Scaling a business requires the right financial architecture. You've discovered how does revenue based lending work to protect your equity while fueling your momentum. This performance-aligned model ensures your payments scale with your sales. It provides the breathing room that traditional loans simply lack. You have the blueprint. Now, you need the ally.

Legacy Funding bridges the gap between your current operations and your ultimate business peak. We provide funds in as little as 24 to 48 hours. No equity dilution is required; your ownership remains 100% yours. Experience the relief of performance-based flexible payments that respect your cash flow. Retain your control. Build your legacy. Our commitment to your expansion is absolute.

The market moves fast. Your funding should move faster. Take the final step toward financial independence and secure the capital your ambition deserves. The iron is hot. Strike now and build the empire you envisioned.

Secure Your Growth Capital in 24 Hours

Frequently Asked Questions

How is revenue-based financing different from a traditional business loan?

Revenue-based financing is technically a purchase of future receivables rather than a standard loan. Traditional loans require fixed monthly payments regardless of your actual performance. If you are exploring how does revenue based lending work, the main difference is that this model aligns with your sales volume. It offers a flexible structure that adapts to your business cycle.

Will I lose equity in my company if I choose revenue-based lending?

You retain 100% of your equity and full control over your board seats. Revenue-based lending is a non-dilutive capital solution. It allows you to scale without giving up future dividends or exit value. You pay for the capital through a one-time factor rate instead of a permanent share of your company's future.

What happens to my payments if my business has a slow month?

Your payments decrease automatically if your revenue drops. Since the remittance is a fixed percentage of your daily or weekly sales, the dollar amount follows your sales curve. This protects your cash flow during seasonal dips or unexpected slow periods. If you have a zero-dollar day, you remit zero dollars.

How fast can I receive funds through revenue-based financing?

You can receive funds in your account within 24 to 48 hours. Our tech-forward application process bypasses the bureaucratic red tape found at legacy banks. By connecting directly to your bank data, we provide rapid decisions that match the speed of modern commerce. Speed is a competitive advantage in your growth strategy.

Do I need perfect credit to qualify for revenue-based funding?

You don't need a perfect credit score to qualify for a capital injection. While personal credit provides a baseline of trust, the primary driver is your verifiable monthly revenue. We prioritize your current momentum and cash flow over past credit history. This allows high-performing businesses to access capital that traditional institutions often deny.

Is there a personal guarantee required for revenue-based lending?

Revenue-based lending typically doesn't require the same heavy collateral or personal guarantees as traditional bank loans. This is because the transaction is a purchase of future sales assets. It shifts the focus from your personal net worth to the strength of your business's revenue streams. Always review your specific agreement for clarity on all legal obligations.

What can I use the revenue-based financing funds for?

You can use the capital for any business-related growth initiative. Common uses include purchasing bulk inventory, launching aggressive marketing campaigns, or hiring key staff to manage expansion. The goal is to use the funds to generate even more revenue. It's a performance-linked injection designed to accelerate your scaling efforts immediately.

How do lenders determine my factor rate and total funding amount?

Lenders analyze your historical bank statements and merchant processing data to set your terms. They look at your average monthly revenue and industry risk to calculate a factor rate. This data-driven approach determines the total purchase amount you can access. Understanding how does revenue based lending work helps you see that your own sales data is your strongest negotiation tool.