Fast Working Capital for Small Business: The 2026 Guide to Rapid Funding

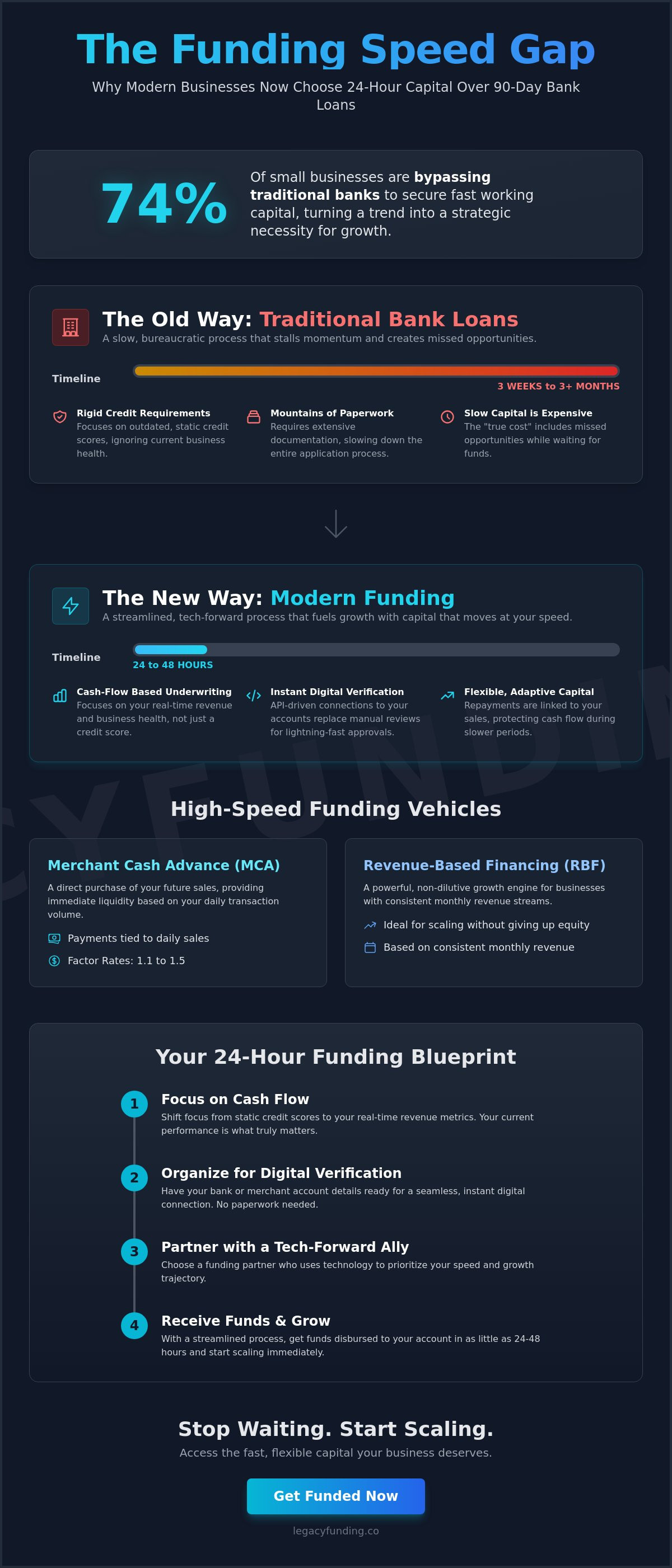

Did you know that 74% of small businesses now bypass traditional banks when seeking fast working capital for small business? This shift isn't just a trend; it's a strategic move toward survival. You've likely felt the sting of a rigid credit requirement or the exhaustion of a weeks-long approval process. Waiting for a legacy institution to recognize your potential shouldn't be the bottleneck that kills your momentum. You deserve a financial ally that moves as fast as you do.

This guide reveals how to secure capital in as little as 24 hours by leveraging your actual revenue rather than outdated bank debt. We'll show you how to trade the mountain of paperwork for a streamlined, tech-forward process that prioritizes your cash flow over a static credit score. It's time to stop begging for permission and start fueling your growth with capital that adapts to your sales. Gain the flexibility you need without the friction of traditional lending.

We'll break down the 2026 landscape of revenue-based solutions, explain how to bypass strict collateral requirements, and provide a clear roadmap to get funds in your bank within 48 hours. Discover how to transform your balance sheet into a launchpad for immediate expansion.

Key Takeaways

- Identify why traditional banks are retreating from the SMB market and how to leverage fast working capital for small business as a strategic tool for operational agility.

- Explore high-speed funding vehicles like Revenue-Based Financing and Merchant Cash Advances to fuel growth without the burden of traditional bank debt.

- Discover how to bypass rigid credit score requirements by shifting your focus to cash-flow-based underwriting and real-time revenue metrics.

- Follow a streamlined 24-hour blueprint to organize your financial data for instant digital verification and rapid fund disbursement.

- Partner with tech-forward financial allies who prioritize your growth trajectory and commit to funding cycles as short as 48 hours.

Closing the Speed Gap: Why Traditional Banks Fail Small Businesses

Speed is the new currency of the 2026 economy. For most founders, fast working capital for small business is no longer a luxury reserved for emergencies. It's a strategic lever for growth. While you're looking to capitalize on a sudden market shift or a bulk inventory discount, traditional banks are still stuck in a 20th-century mindset. They prioritize bureaucratic safety over entrepreneurial agility. This disconnect creates a "speed gap" that can stall even the most promising ventures.

The current lending environment is stark. For the third consecutive year, traditional banks have tightened their underwriting standards, leaving a vacuum in the market. While a legacy institution might take three months to process a single application, the modern commerce cycle moves in hours. You can't afford to wait 90 days for a decision when your competitors are scaling in real time. We bridge this gap by prioritizing your cash flow data over static credit reports, turning a months-long ordeal into a 24-hour reality.

Effective Working capital management fuels the critical space between your accounts payable and your accounts receivable. It's the financial bridge that allows you to pay your team and your suppliers before your customers' checks clear. Without this liquidity, your growth hits a ceiling. We provide the elastic capital necessary to keep your operations fluid and your momentum high.

The True Cost of Waiting for Capital

The "cheapest" loan isn't always the one with the lowest interest rate. If a bank offers a 7% rate but takes twelve weeks to fund, the true cost includes every missed opportunity during that window. Think about the inventory you couldn't buy, the talent you couldn't hire, or the contract you couldn't sign. These delays erode your competitive advantage. In a high-velocity market, slow capital is expensive capital. Rapid funding ensures you're always positioned to say "yes" to growth.

Defining Working Capital in a High-Velocity Economy

The technical formula is simple: Current Assets minus Current Liabilities. However, in 2026, this metric must be elastic. You need capital that expands when sales surge and retracts when things quiet down. Static loans with rigid monthly payments don't account for the natural pulse of a modern business. Working capital is the lifeblood of daily operations. By maintaining a healthy flow, you protect your business from volatility while staying ready for the next big acquisition or expansion phase.

Alternative Funding Vehicles: Maximizing Speed via MCA and RBF

Traditional financing treats your business like a risk to be managed. We treat it like an asset to be fueled. When you need fast working capital for small business, the conventional term loan model often fails because it's too slow and too rigid. Alternative funding vehicles like Merchant Cash Advances and Revenue-Based Financing solve this by linking your capital to your performance. These aren't just loans; they're strategic tools designed for the speed of modern commerce. They prioritize your future potential over your past credit history.

The core advantage of these models is their reliance on real-time data. By connecting directly to your bank or merchant accounts, lenders can verify your health in minutes. This digital-first approach is exactly why these structures allow for 24 to 48-hour funding speeds. You skip the manual reviews, the physical paperwork, and the long wait for a committee's approval. It's capital at the speed of an API call.

Merchant Cash Advances: Liquidity Based on Daily Sales

A Merchant Cash Advance (MCA) is a straightforward purchase of your future sales. Instead of a fixed monthly bill, the provider takes a small percentage of your daily credit card receipts or bank deposits. This model relies on factor rates rather than traditional interest. According to 2026 industry data, these rates typically range from 1.1 to 1.5. This means you know your total repayment amount from day one. Because the underwriting focuses on your terminal data and daily volume, the process is incredibly efficient. Payments fluctuate with your revenue, protecting your cash flow during lean periods.

Revenue-Based Financing: Growth Capital Without Equity Dilution

Revenue-Based Financing (RBF) serves as a powerful, non-dilutive growth engine for businesses with consistent monthly revenue. You receive a lump sum and pay it back through a fixed share of your monthly gross income, usually between 2% and 10%. This is the preferred choice for service providers and tech-forward founders who want to avoid selling equity. When funding your small business, RBF offers the distinct advantage of requiring no physical collateral. The repayment cap generally sits between 1.1x and 2.0x your initial funding amount. It allows you to scale rapidly while keeping 100% of your ownership intact.

The flexibility of these structures is their greatest strength. Fixed installments can crush a business during a slow month, but sales-linked payments breathe with your business. This alignment of interests is why alternative funding has become the primary choice for 74% of small businesses. If you want to explore how these options can scale your specific model, connect with our team for a tailored analysis.

Qualifying for Fast Capital: Moving Beyond the Credit Score

Your credit score is a snapshot of your past. It's not a forecast of your future. Many founders hesitate to seek fast working capital for small business because they fear a three-digit number will disqualify them. In the legacy banking world, a low score is a dead end. In the modern financial landscape, it's just one data point among many. We've moved beyond character-based lending to a model that values what actually matters: your current performance and your trajectory.

The shift to cash-flow-based underwriting is a game changer for entrepreneurs. Instead of judging you on a personal credit mishap from years ago, modern lenders look at your business's real-time health. They prioritize three key pillars: consistent monthly revenue, time in business, and industry stability. If your business is generating sales, you have leverage. A steady stream of incoming revenue is the ultimate form of collateral. It proves you have the capacity to repay and the momentum to scale.

Why Your Cash Flow is the Real Collateral

Modern underwriting engines analyze your bank statements to find the pulse of your business. They look for consistency. A high daily average balance often carries more weight than a perfect FICO score. This digital verification process identifies patterns that traditional banks miss. It sees your resilience. Your revenue history is the best predictor of future performance, providing a transparent view of your ability to handle new capital without straining your operations.

Revenue Requirements vs. Credit History

Most rapid funding options require a baseline of consistent five-figure monthly revenue. If your credit history is troubled, lead with your growth data. Recent 2026 reports show that 94% of small business owners project expansion this year. Use that optimism. Highlight your industry-specific performance to provide context for your cash flow. A strong revenue trend can easily outweigh a legacy credit issue. Lenders are looking for a clear path to repayment, often through the 2% to 10% monthly revenue share common in modern agreements. Prove your momentum, and the capital will follow.

The 24-Hour Funding Blueprint: How to Accelerate Your Application

Achieving a 24-hour turnaround isn't a matter of luck. It's the result of a deliberate, streamlined strategy. When you're hunting for fast working capital for small business, your preparation determines your pace. Traditional lending is slow because it relies on manual data entry and physical paper trails. Modern funding is fast because it uses digital bridges to verify your health in real time. If you want the capital tomorrow, you must provide the transparency today.

The path from application to deposit follows a precise four-step sequence. First, you complete a digital application that focuses on your growth goals. Second, you integrate your bank data through secure, encrypted portals. Third, an underwriting algorithm analyzes your cash flow patterns to generate an offer. Finally, you sign the digital contract and trigger the wire. This entire cycle can happen within a single business day if your data is organized and ready for inspection.

Digital bank verification is the gold standard for 2026. It removes the friction of manual uploads and the risk of human error. By providing a direct view of your transactions, you offer the ultimate proof of your business's vitality. This transparency builds immediate trust, allowing lenders to move with the same urgency that your business demands.

Essential Documentation Checklist for Instant Approvals

To hit the 24-hour mark, you need the "Big Three" ready before you click apply. This includes your government-issued Tax ID, a voided business check, and your most recent 4 to 6 months of bank statements. Most tech-forward lenders use tools like Plaid to pull this data automatically. Ensure your statements are in a clean, digital format. Having these assets at your fingertips eliminates the back-and-forth emails that often stall the funding process for days.

Avoiding Common Pitfalls That Stall Funding

Speed bumps are often self-inflicted. One of the most dangerous mistakes is "stacking" multiple advances simultaneously. If a lender sees multiple active positions on your bank statements, it signals high risk and can lead to an immediate denial. Additionally, ensure your business name matches perfectly across all legal and banking documents. Even a small discrepancy in an LLC name can trigger a manual fraud review. Maintain open lines of communication. When your funding advisor asks for a clarification, respond within minutes, not hours. If you're ready to start the clock, submit your application today and let our team accelerate your growth.

Legacy Funding Advisors: Your Partner in Rapid Scalability

Your business shouldn't be held hostage by a bank's calendar. Legacy Funding operates as a savvy, tech-forward financial ally for the modern founder. We've replaced the bureaucratic hurdles of traditional institutions with a streamlined system designed for rapid execution. Securing fast working capital for small business is no longer a complex puzzle. It's a strategic decision. We serve entrepreneurs across the United States, Puerto Rico, and Canada, providing the liquidity needed to outpace the competition. Our approach bridges the gap between high-stakes finance and the aspirational reality of scaling a venture.

We don't view funding as a simple transaction. It's a partnership. We speak the language of the modern founder, focusing on growth metrics rather than just financial obligations. By sharing insider knowledge, we position you for financial independence. Our process is bold, transparent, and slightly disruptive to the status quo. We understand the speed of contemporary commerce better than legacy institutions. We're here to help you build a business that lasts for generations.

Our 24 to 48-Hour Funding Commitment

We believe transparency is the foundation of speed. Our proprietary technology creates a direct bridge between your performance data and our underwriting team. This bypasses the manual errors and delays that plague legacy lenders. We commit to a 24 to 48-hour funding cycle for approved applicants. This isn't just a promise; it's our standard. You get the capital you need without the "fine print" fatigue. We provide the weight of professional expertise while removing the friction of traditional banking. Every step we take is designed to move you closer to your next milestone.

Tailored Capital Solutions for Every Industry

Different sectors require different strategies. From high-volume retail to project-based construction, we tailor our capital solutions to match your specific industry cycles. We don't just look at today's balance sheet. We look at your potential for generational impact. Our goal is to move beyond the transaction and become a long-term partner in your success. Financial support should be a generational endeavor that secures your business's future for years to come. We offer the tools you need to expand, acquire, and dominate your market. Take control of your trajectory now. Secure your fast working capital today and join a community of founders who refuse to wait for growth.

Fuel Your 2026 Growth Strategy Today

The lending landscape has shifted permanently. You no longer need to wait on legacy institutions that prioritize red tape over your results. By leveraging your real-time revenue data, you can unlock fast working capital for small business without the friction of traditional bank debt. You've seen how revenue-based underwriting and digital verification can compress months of waiting into a single day of action. This is the modern key to financial independence.

We're committed to your long-term impact. Whether you're operating in the US, Puerto Rico, or Canada, our team provides the tech-forward tools to help you scale. We provide quotes with no hard credit pull and deliver funding in as little as 24 to 48 hours. Don't let a temporary lack of liquidity stop your generational growth. Your vision deserves a partner that moves at your speed.

Scale your business with fast capital. Apply in minutes.

Take the first step toward rapid expansion today. We're ready to fuel your success.

Frequently Asked Questions

How fast can I actually get working capital for my small business?

You can secure funding in as little as 24 to 48 hours. Our streamlined digital application and real-time bank verification eliminate the weeks of waiting required by traditional institutions. By connecting your accounts directly, you trigger an automated underwriting process that delivers a decision in hours. Once you sign the digital contract, the wire is initiated immediately. This rapid cycle ensures you never miss a time-sensitive growth opportunity or a critical inventory discount.

Do I need a high credit score to qualify for fast business funding?

You don't need a perfect credit score to qualify for fast working capital for small business. Modern underwriting focuses on your actual cash flow and monthly revenue rather than legacy credit metrics. If your business shows consistent sales and a healthy daily average balance, your FICO score becomes a secondary factor. We prioritize your current performance and future growth trajectory. This shift empowers founders who have been unfairly sidelined by traditional banks due to outdated requirements.

What is the difference between a working capital loan and a merchant cash advance?

A working capital loan is a traditional debt instrument with fixed monthly payments and a set term. In contrast, a Merchant Cash Advance (MCA) is a purchase of your future sales. Instead of a rigid bill, an MCA provider takes a small percentage of your daily credit card receipts or bank deposits. This means your repayment scales naturally with your revenue. It provides a flexible safety net that protects your liquidity during slower periods while accelerating during peaks.

Can I get fast funding if my business is seasonal?

Yes, seasonal businesses are excellent candidates for revenue-based funding solutions. Because repayments are often tied to a percentage of your sales, your obligations naturally decrease during your off-season. This prevents the cash flow strain that fixed bank payments often cause. We analyze your annual revenue patterns to ensure the funding structure supports your peak periods without crushing you during the quiet months. Your capital should adapt to your rhythm, not the other way around.

Is collateral required for revenue-based financing?

No physical collateral like real estate or equipment is typically required for revenue-based financing. Your consistent monthly revenue serves as the primary security for the funding. This makes it an ideal solution for service-based or tech companies that lack significant tangible assets. You retain full ownership of your business while gaining the liquidity needed for immediate expansion. It's a low-barrier path to rapid scaling without the risk of losing your hard-earned personal or business assets.

How will fast working capital affect my business credit score?

Most alternative funding options don't require a hard credit pull for a quote, meaning your score stays protected during the inquiry phase. While many non-bank lenders don't report daily payments to the major bureaus, the capital allows you to stay current with other obligations. This helps you maintain a strong overall financial profile. Use fast working capital for small business to consolidate high-interest debt or improve your debt-to-income ratio. It’s a strategic move for long-term stability.

What are the typical use cases for fast working capital in 2026?

Modern founders use fast capital to capitalize on immediate growth triggers. Common use cases include purchasing bulk inventory at a discount, launching aggressive marketing campaigns, or hiring talent to fulfill new contracts. According to 2026 survey data, 56% of businesses seek financing to meet operating expenses while 46% focus on expansion. Having liquid capital ready allows you to act decisively when a market opportunity appears. Don't let a lack of cash stall your momentum when you're ready to scale.

Can I apply for additional funding if I already have an existing business loan?

You can apply for additional capital even with an existing loan, provided your cash flow can support the added obligation. We look at your total debt-to-income ratio to ensure further funding is a healthy move for your business. However, avoid "stacking" multiple advances simultaneously, as this can signal high risk to underwriters. We often help clients use new capital for debt consolidation, turning high-cost positions into a more manageable structure. Focus on sustainable growth and long-term impact.