Documents Needed for SBA Loan Application: The 2026 Master Checklist

A single missing signature or an outdated residency status can kill your expansion plans before a lender even looks at your revenue. In 2026, the margin for error has vanished. You shouldn't have to fight a mountain of paperwork just to access the capital you've earned. We know you're likely overwhelmed by the sheer volume of the documents needed for sba loan application. It's frustrating to watch your growth stall while you hunt for obscure forms or wait weeks for a bank's feedback.

You want to scale, not spend your nights acting as a forensic accountant. This master checklist bridges the gap between your current frustration and your future expansion. We've simplified the entire process so you can prepare, submit, and scale. You'll gain the confidence that your application is bulletproof and secure your funding faster. We're here to act as your financial ally, providing the insider knowledge you need to win.

We'll break down the mandatory 2026 requirements, explain the critical March 1 citizenship updates, and show you how to organize a package that commands an immediate approval. Stop guessing and start growing.

Key Takeaways

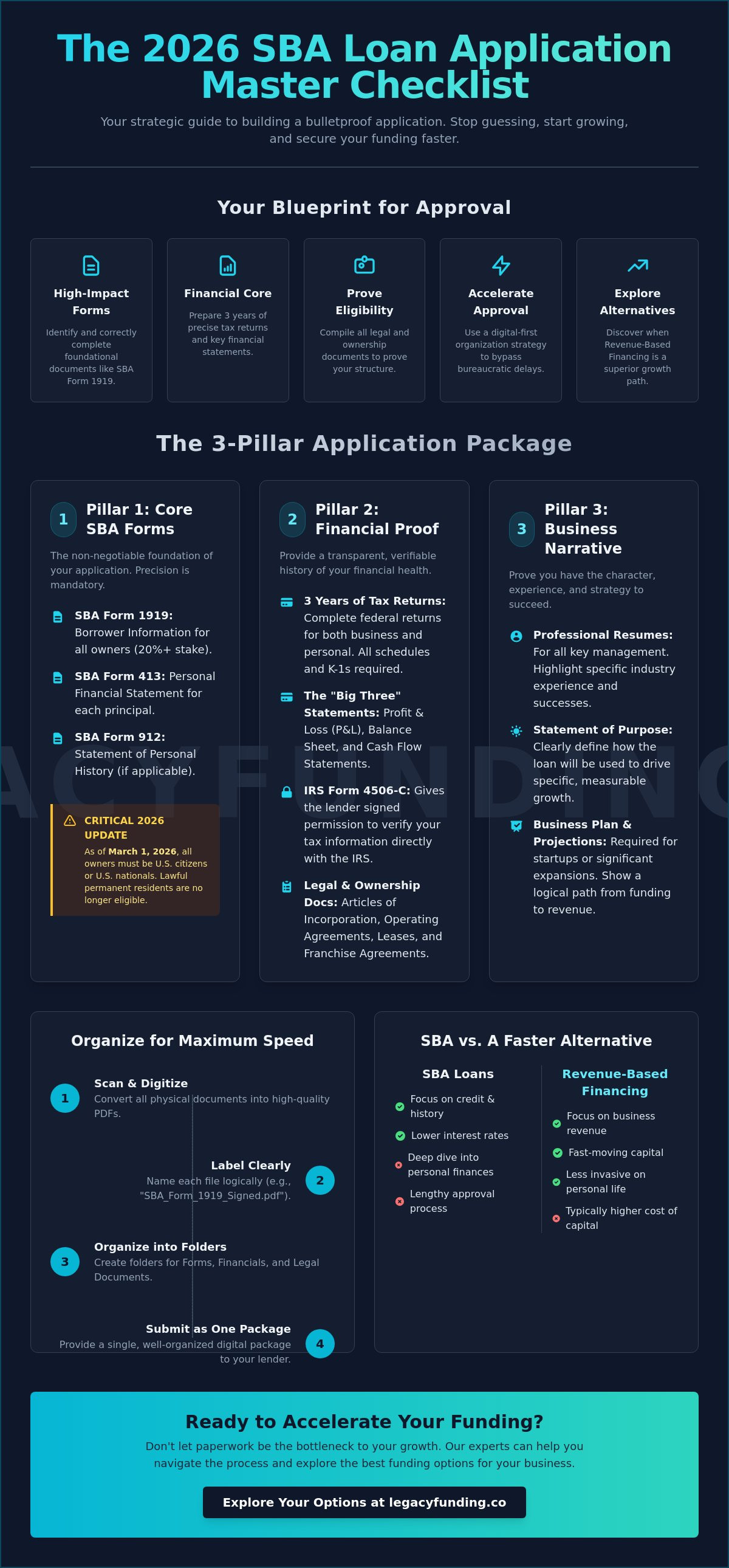

- Identify the high-impact forms that build your application foundation, starting with the critical SBA Form 1919 disclosure.

- Master your financial core by precisely preparing your "Big Three" statements and three years of federal tax returns.

- Secure your eligibility by compiling all necessary legal structure and ownership documents needed for sba loan application.

- Accelerate your approval timeline with a digital-first organization strategy designed to bypass traditional bureaucratic friction.

- Discover when a fast-moving Revenue-Based Financing model provides a superior growth path compared to the standard SBA route.

The Universal SBA Loan Document Checklist: Your Foundation for Approval

SBA approval starts with a shift in perspective. You aren't just filling out forms; you're building a strategic case for your company's future. The Small Business Administration (SBA) provides the framework for these guarantees, but your preparation provides the substance. While every lender has internal quirks, the core documents needed for sba loan application remain consistent across the federal landscape. Precision is your greatest asset here. One mismatched date or a missing signature on a federal disclosure can trigger a manual review that adds weeks to your timeline. Secure your foundation by treating every form as a high-stakes contract.

Standard SBA Forms You Must Download

The anchor of your package is SBA Form 1919 (Borrower Information). This document captures the essential data for every owner with a 20% stake or more. Accuracy is vital because it cross-references with federal databases to verify your eligibility. As of March 1, 2026, the SBA has implemented a strict citizenship requirement. Every owner must now be a U.S. citizen or U.S. national; lawful permanent residents are no longer eligible for these programs. This makes Form 1919 your first line of defense in the approval process.

You must also provide SBA Form 413, the Personal Financial Statement. This form gives underwriters a clear picture of your personal liquidity and net worth. If you have a non-standard background or past legal issues, SBA Form 912 (Statement of Personal History) is where you provide clarity. Don't hide from your history. Address it head-on with transparency to build trust with your lender. When you finalize the documents needed for sba loan application, ensure these forms are the most current versions available for the 2026 fiscal year.

The Personal Narrative and Business Resume

Numbers tell part of the story, but your resume proves you can manage the capital. Lenders look for "character and eligibility" which goes beyond a credit score. Prepare a professional resume for every key management member that highlights specific industry experience and past successes. If you are pivoting your business model or expanding into a new market, your resume must demonstrate the competency to handle that transition.

Complement this with a punchy "Statement of Purpose" for the loan proceeds. Clearly define how the capital will be deployed to drive growth. Whether you are targeting the $5 million 7(a) ceiling or a smaller SBA Express loan, the underwriter needs to see a logical path from funding to revenue. Use active verbs and concrete growth metrics. Proving your management depth is just as important as proving your cash flow. This narrative transforms a pile of paperwork into a compelling investment opportunity.

Mastering the Financial Core: Tax Returns, Statements, and Projections

Financial precision is your strongest leverage during the underwriting process. Lenders don't just look at your bank balance; they look for a consistent history of debt repayment and profitability. Your tax returns act as the verified heartbeat of your business. When gathering the documents needed for sba loan application, you must provide three full years of both personal and business federal income tax returns. Ensure every page is signed and dated correctly. This isn't a suggestion. It's a federal requirement that establishes the baseline for your eligibility.

Lenders use IRS Form 4506-C to verify your data directly with the government. This form allows the bank to pull your transcripts and cross-reference them with your provided returns. If you have filed for an extension or have late filings, provide the extension documents and your most recent year-end internal financials. Transparency builds trust. Hidden tax liabilities or unfiled returns will stop your application in its tracks. Address these gaps early to keep your momentum high.

Tax Returns and IRS Verification

Precision matters more than volume. Your returns must be complete, including all schedules and K-1s. If you own multiple entities, you'll need returns for those as well. Underwriters look for a "global" view of your financial health. They want to see that your total income can cover both your personal obligations and the new loan payments. If you find the SBA's deep dive into your personal taxes too invasive, you might explore more streamlined options that focus strictly on business performance.

Interim Financial Statements and Aging Reports

Historical data isn't enough to secure a $5 million 7(a) loan in a fast-paced market. You need to prove your business is thriving right now. Prepare your "Big Three" financial statements: the Profit and Loss (P&L), the Balance Sheet, and the Cash Flow statement. For a detailed breakdown of how these impact your specific loan type, this Forbes guide to SBA 7(a) loans offers excellent context on underwriter expectations. Your interim P&L must be dated within 90 days of your application to ensure the lender is seeing your current trajectory.

Include Accounts Receivable (AR) and Accounts Payable (AP) aging reports to demonstrate management efficiency. These reports show how quickly you collect cash and how you manage your obligations. Audit your Business Debt Schedule for absolute accuracy. Every note, lease, and line of credit must be listed. If your 2025 revenue showed a dip due to a specific one-time event, provide a clear narrative explanation. Underwriters value context. Proving that a loss was an anomaly rather than a trend can be the difference between a denial and a funded deal.

Legal and Ownership Documentation: Proving Eligibility and Structure

Your business structure is the skeletal frame of your entire loan application. Underwriters scrutinize your legal files to confirm two things: you have the authority to borrow, and your entity is in good standing with the state. This stage of the process requires absolute transparency. Missing a single operating agreement or an outdated business license can stall your file for weeks. Gather your Articles of Incorporation, bylaws, and operating agreements immediately. These are the core documents needed for sba loan application because they define who holds the power to sign for the debt.

Confirm your status with the Secretary of State by pulling a fresh Certificate of Good Standing. This proves your entity is active and compliant with state taxes and filings. If you operate under a "Doing Business As" (DBA) name, provide the recorded certificate. Additionally, provide copies of your current commercial leases or real estate deeds. Lenders need to verify your business has a legal right to occupy its space for the duration of the loan term. If your lease is set to expire soon, secure an extension or a letter of intent from your landlord before submitting your package.

Corporate Governance and Ownership Records

Ownership must be documented with surgical precision. Provide a Stock Ledger or a membership certificate summary that accounts for 100% of the company's equity. If you operate a franchise, your franchise agreement is a mandatory addition to your file. The SBA must review these agreements to ensure you maintain enough independence from the franchisor to qualify as a small business owner. Audit your records to ensure every owner with a 20% stake or more is clearly identified and ready to provide their personal disclosures.

The Affiliation Rule: Why Your Other Businesses Matter

The SBA's affiliation rule is a common trap for serial entrepreneurs. Under the 2026 guidelines, the SBA looks beyond your primary company to see what else you control. Affiliation exists when one business has the power to control another, or a third party has the power to control both. This is often determined by ownership percentage, common management, or identical business interests. If you own 50% or more of another entity, that business is likely an affiliate.

You must gather financial statements and tax returns for all affiliated entities. The SBA combines the revenue and employee counts of all affiliates to determine if you still meet the "Small Business" size standards. This calculation is vital. If your combined entities exceed the size limits for your industry's NAICS code, your application will be denied. Disclose every connection early. Hidden affiliations are a major red flag that suggests a lack of transparency, which can kill a deal faster than a low credit score.

How to Organize Your Application Package for Maximum Speed

Bureaucracy thrives on chaos. Your job is to provide order. Speed is a competitive advantage in the 2026 lending environment, and you can't afford to let a messy file structure delay your capital. Most applicants view the submission as a passive event. They wait for the lender to ask for more. You should do the opposite. Provide every file before the underwriter even thinks to ask. Organizing the documents needed for sba loan application is not just about filing; it is about narrative control. You want to present a package that is so clean it demands immediate approval.

Adopt a digital-first mindset from day one. Stop thinking in terms of paper and start thinking in terms of real-time data access. Create a secure, cloud-based data room where you and your lender can view files simultaneously. This eliminates the "email ping-pong" that adds weeks to traditional bank processing times. If you want a partner who moves at the speed of your business, connect with our team today to explore how we streamline the path to funding.

Digital Organization and File Naming

Underwriters are human. They appreciate clarity. If they have to hunt for your 2025 Profit and Loss statement, they will move your file to the bottom of the pile. Structure your digital folders into four distinct categories: Financials, Legal, Personal, and Application. This logical flow allows the reviewer to move through your package without friction. Use a standardized naming convention for every file. We recommend the [Year-Category-DocumentName] format. For example: "2025-Financials-BalanceSheet.pdf".

Quality matters as much as organization. Ensure every scan is a high-resolution, searchable PDF. Use Optical Character Recognition (OCR) technology so the underwriter can search for specific line items within your tax returns or bank statements. This small technical step shows you are a savvy, tech-forward founder who respects the lender's time. It builds immediate trust and positions you as a low-risk borrower.

The Pre-Submission Audit Checklist

Perform a pre-flight audit before you hit send. This is your final defense against avoidable delays. Check that every SBA form is the most current version released for the 2026 fiscal year. Forms change. Using an outdated version of SBA Form 1919 is a guaranteed way to get your application kicked back. Verify that your Employer Identification Number (EIN) and business address match exactly across every single document. Discrepancies here trigger fraud alerts that can take months to resolve.

Review your tax return PDFs with a critical eye. Eliminate blank pages, missing schedules, or upside-down scans. These minor errors suggest a lack of attention to detail. Ensure that all signatures are present and dated. If a document requires a wet signature, don't try to bypass it with a generic digital stamp unless your lender specifically approves it. Your goal is a bulletproof package that leaves no room for questions or follow-up requests.

Beyond the Paperwork: Accelerating Your Funding with Legacy Funding Advisors

The reality of modern commerce is that opportunities don't wait for federal approval. While you've now mastered the list of documents needed for sba loan application, you must also prepare for the administrative waiting period. A standard 7(a) or 504 loan can take anywhere from 90 to 180 days to fund. This gap is where growth often dies. Legacy Funding Advisors provides the antidote to this stagnation. We position SBA loans as a vital long-term strategy, but we utilize faster vehicles like Revenue-Based Financing for tactical, immediate wins. You shouldn't have to choose between a low-interest loan and the ability to act now.

Our process focuses on momentum. We don't view your business as a pile of historical tax returns. We see it as a living, breathing revenue engine. By shifting the focus to your current performance, we bypass the bureaucratic hurdles that slow down traditional institutions. You gain access to capital in days, not months. This speed allows you to secure inventory, launch marketing campaigns, or consolidate debt while the SBA reviews your master file. We act as your high-level consultant, ensuring your capital stack is as agile as your business model.

SBA Loans vs. Fast Funding: Choosing Your Momentum

Comparing a standard SBA timeline to our 24-48 hour execution reveals a massive gap in efficiency. Revenue-Based Financing and Merchant Cash Advances (MCAs) require approximately 90% fewer documents than a typical SBA package. Instead of three years of personal and business returns, we often only need your recent bank statements to verify cash flow. This low-doc approach removes the friction from the application process. Many savvy entrepreneurs use our funding as bridge capital. They scale their operations immediately while their long-term SBA application remains in underwriting limbo. This strategy ensures you never miss a market cycle due to a slow bank.

How Legacy Funding Advisors Streamlines Your Growth

Our tech-forward approach prioritizes your current cash flow over static credit scores. We look at the pulse of your business. This allows us to provide customized capital solutions for industries that legacy banks often avoid due to outdated risk models. Whether you need equipment financing or a flexible line of credit, we remove the barriers to entry. We understand that financial support is a generational endeavor. Your growth shouldn't be a casualty of a slow bank. Apply for fast business funding today and take control of your company's momentum. Secure your future with a partner who moves at the speed of contemporary commerce.

Secure Your Growth and Outpace the Competition

Mastering the documents needed for sba loan application is the first step toward long-term stability. You now have the roadmap to navigate federal requirements, audit your financial core, and organize a digital-first package that underwriters can't ignore. Precision beats volume every time. By aligning your corporate governance and tax records with 2026 standards, you remove the friction that stalls most founders. Your preparation transforms a complex bureaucratic process into a manageable path for expansion.

Your business moves faster than a government agency. When you need immediate momentum, look beyond the traditional bureaucratic slog. Legacy Funding Advisors specializes in rapid execution with national coverage across the US and Canada. We prioritize your actual cash flow over static credit scores to ensure your expansion never hits a wall. Don't let your growth plans sit in a bank's inbox for months while your competitors take the lead.

Secure your business funding in as little as 24 hours with Legacy Funding Advisors.

Your vision deserves capital that moves at the speed of your ambition. Start building your legacy today.

Frequently Asked Questions

What is the most important document for an SBA loan?

SBA Form 1919 (Borrower Information) stands as the most critical disclosure in your package. It captures essential data for every owner with a 20% stake or more to verify federal eligibility. This form is the primary tool lenders use to cross-reference your status with government databases. Accuracy here is non-negotiable because one error can trigger a manual review that stalls your funding for weeks.

How many years of tax returns are required for an SBA 7(a) loan?

You must provide three full years of both personal and business federal income tax returns. These returns act as the verified financial history of your company and its owners. Ensure every page is signed and dated correctly to avoid immediate rejection. If you've filed extensions for the current year, include those along with your most recent year-end internal financials to maintain momentum.

Can I get an SBA loan if I don't have a business plan?

A comprehensive business plan is mandatory for most SBA loan types, especially for startups or significant expansions. Lenders need a roadmap that proves your ability to generate enough cash flow to repay the debt. Your plan should include detailed financial projections and a clear "Statement of Purpose" for the loan proceeds. If you need capital without the heavy planning requirements, consider Revenue-Based Financing as a more agile alternative.

Do I need to provide personal documents if the loan is for my corporation?

Yes, personal documentation is required for all owners holding at least a 20% stake in the corporation. The SBA requires a "global" view of financial health to ensure the business has strong backing. You'll need to submit personal tax returns and SBA Form 413 (Personal Financial Statement) alongside your corporate files. This transparency builds the trust necessary to secure a federal guarantee for your business.

What happens if I cannot provide a specific document on the checklist?

Missing a required document typically halts the underwriting process until the gap is filled. If a specific form truly doesn't apply to your situation, you must provide a formal written explanation to the lender. Underwriters prefer clarity over silence. Proactively addressing a missing file prevents your application from being moved to the bottom of the pile while other founders secure their funding.

How long are financial statements valid for an SBA application?

Interim financial statements like your Profit and Loss and Balance Sheet are generally valid for 90 days. If your application process drags on beyond this window, the lender will likely request updated Year-to-Date reports. Keeping your books current ensures you can provide these documents needed for sba loan application without delaying your approval timeline or missing a critical growth window.

Can I submit my SBA loan application digitally?

Digital submission is the preferred method for modern lenders and the SBA's own portals. Submitting your files electronically through a secure data room significantly reduces the administrative friction that slows down traditional bank processing. Use high-resolution, searchable PDFs to make the underwriter's review as seamless as possible. Tech-forward organization shows you are a savvy founder who respects the lender's time.

What is a Business Debt Schedule and why is it required?

A Business Debt Schedule is a detailed list of all current notes, leases, and lines of credit your company carries. Lenders use this to calculate your debt-service coverage ratio and determine if you can afford the new loan payments. Every entry must match your Balance Sheet exactly. Accuracy on this schedule is vital for proving your business can handle the capital needed to scale effectively.