Business Line of Credit vs. Term Loan: Choosing Your Strategic Growth Blueprint in 2026

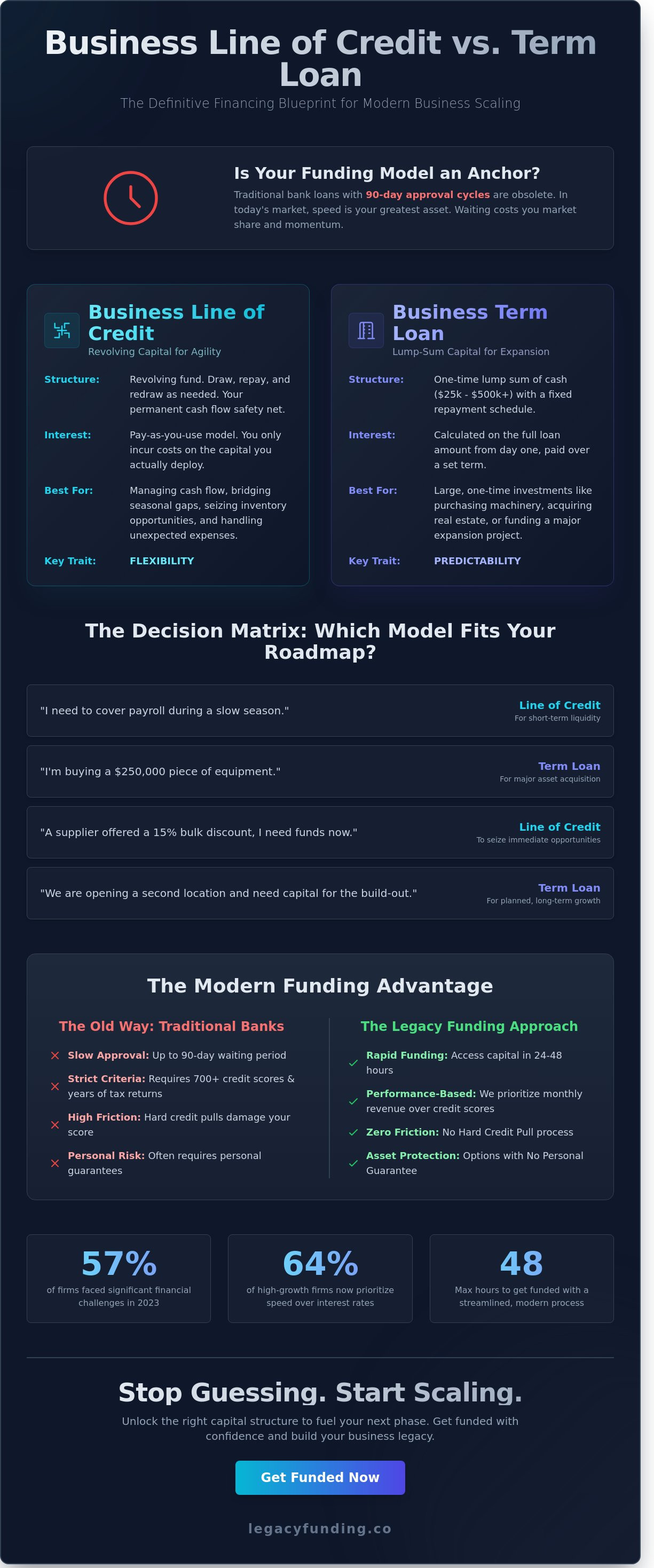

The traditional bank loan is no longer the gold standard for scaling. In 2026, it's often the anchor that drags your momentum to a halt. You already know that timing is everything in your industry. Waiting 90 days for a credit committee to review your file is a relic of the past that costs you market share. You need to understand the business line of credit vs term loan debate to ensure you don't fall behind. According to the 2023 Small Business Credit Survey, 57% of firms faced significant financial challenges. Most of those businesses failed to act because they feared over-leveraging or slow approvals.

This guide provides the definitive comparison of revolving credit and lump-sum loans to help you decide which structure will accelerate your business legacy. We'll help you unlock the right capital structure to fuel your next phase. You can secure fast access to funds in 24 to 48 hours without the friction of a No Hard Credit Pull process. Our approach is designed to remove the red tape and put you in control. Get Funded with confidence.

We'll break down the specific mechanics of these two funding models. You'll learn how to choose the blueprint that maximizes your operational flexibility while protecting your assets. We focus on minimizing personal risk through options with No Personal Guarantee. It's time to stop guessing and start scaling with precision.

Key Takeaways

- Master the strategic distinction between revolving capital and installment debt to build a financing blueprint that scales your business legacy.

- Evaluate the business line of credit vs term loan trade-offs to decide whether flexible revolving access or a structured lump sum accelerates your roadmap.

- Audit your 12-month cash flow projections using a surgical decision matrix to eliminate the risks of over-borrowing and credit fatigue.

- Discover how to unlock capital in under 48 hours with a streamlined process that protects your credit score while you scale.

- Learn why the "one-size-fits-all" lending model is obsolete and how to select the specific capital structure that maximizes your ROI.

The Capital Dilemma: Defining Your Business Funding Roadmap

Choosing between a business line of credit vs term loan isn't just a math problem. It's a strategic decision that defines your legacy. Traditional banking models from 2020 are dead. In 2026, agility is the only currency that matters. You must stop thinking about debt as a burden. Start viewing capital as a high-velocity tool for expansion. A 2025 study from the Small Business Administration indicated that 64% of high-growth firms now prioritize immediate access over long-term interest rates. This shift marks the end of the one-size-fits-all lending era. You need a blueprint that matches your specific growth trajectory. Modern founders reject the red tape of 1990s-style financing. They demand speed. They demand accessibility. They demand a partner who understands that a three-week approval process is a death sentence for a hot lead.

Identify your objective immediately. Are you capturing a fleeting market opportunity or stabilizing your core operations? Revolving capital and installment debt serve different masters. One provides a safety net for cash flow; the other builds the foundation for long-term assets. Strategic leveraging means deploying the right dollar at the right time. Don't just borrow. Accelerate. At Legacy Funding Advisors, we bridge the gap between financial theory and entrepreneurial reality. We focus on your growth metrics rather than just debt obligations. Our goal is to unlock your next level of scaling with zero friction.

The Role of a Business Line of Credit

Speed defines the modern market. A business line of credit provides the liquidity you need to pivot instantly. According to Wikipedia's definition of a line of credit, this revolving facility allows you to draw funds, repay them, and draw again as needed. It acts as a permanent insurance policy for your cash flow. In a high-interest environment, the pay-as-you-use model is superior. You only incur costs on the capital you actually deploy. This eliminates the waste associated with sitting on idle cash. Use it to bridge seasonal gaps or secure inventory at a 15% bulk discount. Legacy Funding Advisors prioritizes your momentum. With options that require No Hard Credit Pull, you can secure your liquidity without damaging your score. Get funded and stay ready for any opportunity.

The Strategic Use of a Business Term Loan

Predictability builds empires. A business term loan delivers a lump sum for massive, fixed-cost investments. Think of this as the blueprint for your long-term asset acquisition. You get a clear repayment schedule with fixed monthly or weekly payments. This structure makes budgeting simple and transparent. If you are purchasing a $250,000 piece of specialized machinery or opening a second location, the term loan is your primary weapon. It provides the stability required for multi-year projects. When comparing a business line of credit vs term loan, the latter is your choice for expansion that requires significant upfront weight. Our process removes the friction. We look at your future potential. We offer solutions with No Personal Guarantee to protect your individual assets while you build your business legacy. Get funded and scale with confidence.

Mechanics of Growth: Business Line of Credit vs. Term Loan

Capital serves as the engine of your enterprise. Choosing between a business line of credit vs term loan determines how fast that engine runs. Term loans provide a single injection of cash, usually ranging from $25,000 to $500,000. You receive the full amount immediately and begin paying interest on every dollar. This structure works best for fixed assets or long-term expansions with predictable costs. A business line of credit functions like a strategic reservoir. You only pay interest on the capital you actually deploy. This flexibility preserves your cash flow during seasonal dips or sudden inventory opportunities.

Legacy Funding shifts the focus from your past to your future. We don't rely on the outdated metrics that stall traditional banks. Most conventional lenders demand a 700+ credit score and years of tax returns. We prioritize your actual performance. By emphasizing monthly revenue over credit scores, we provide a faster path to get funded without the friction of a hard credit pull. This approach allows you to secure capital based on the strength of your sales, not just your history.

- Funding Speed: Lines of credit offer recurring access; term loans provide a one-time lump sum.

- Interest: Pay only on utilized balances with a line; pay on the full principal with a loan.

- Collateral: We offer unsecured options that protect your personal assets and business equipment.

Draw Schedules and Repayment Rhythms

Revolving draws empower you to react to the market in real time. You pull funds, execute your plan, and replenish the line. This cycle keeps your balance sheet lean and your options open. Term loans require a different discipline. You must manage the amortization carefully to ensure your monthly debt service doesn't outpace your growth. Amortization is the systematic repayment of a loan's principal and interest over a set period until the balance reaches zero.

Total Cost of Capital Analysis

Evaluate the total cost, not just the interest rate. Factor rates are common in alternative lending and represent a fixed multiplier of the total funding amount. You should also watch for origination fees that can range from 1% to 5% of the total limit. Forbes' analysis of business loans vs. lines of credit highlights that lines of credit often carry variable rates, while term loans offer the stability of fixed payments.

Calculate your projected ROI before you sign any agreement. If a $100,000 injection allows you to secure a contract worth $300,000, the capital has paid for itself three times over. Focus on the leverage. Focus on the blueprint. Focus on the growth metrics that actually move the needle for your business.

Flexibility vs. Precision: Analyzing Pros, Cons, and Risks

Choosing between a business line of credit vs term loan isn't just about the money. It's about how that capital moves through your operation. Term loans offer a massive lump sum, but they carry the risk of over-borrowing. If you take $500,000 for a project that ends up costing $410,000, you're paying interest on $90,000 of dead weight. Lines of credit present a different challenge: credit line fatigue. Keeping your utilization above 75% for more than three consecutive months can signal distress to traditional lenders, even if your revenue is scaling at 20% year-over-year.

Line of Credit: The Ultimate Safety Net

Unlock capital instantly. This product functions as a revolving door for your cash flow. You don't re-apply; you just draw. While rates can be variable, the agility is unmatched. It's the ideal tool for managing 30-day payroll gaps or 15% seasonal inventory spikes. According to the SBA's guide to business lines of credit, this flexibility helps businesses manage cyclical cash flow issues without taking on long-term debt obligations. Use it to bridge the gap while waiting for net-60 invoices to clear.

- Pro: Immediate access to funds without the friction of re-applying.

- Con: Potential for variable rates and lower initial limits than fixed loans.

- Best for: Seasonal inventory, payroll gaps, and emergency repairs.

Term Loan: The Heavy-Duty Growth Engine

Think big. Term loans provide the heavy-duty funding needed for 25% floor space expansions or acquiring a competitor. You get the full amount upfront. The downside is the lack of flexibility. You pay for the entire blueprint from day one, regardless of when you actually spend the cash. This structure is best for predictable, one-time costs where the ROI is clear and the timeline is fixed.

- Pro: Higher funding ceilings for major business expansions.

- Con: Paying interest on the full amount even if funds sit idle in your account.

- Best for: Equipment purchases, real estate, and business acquisitions.

Your credit profile needs a strategic build. Term loans demonstrate your ability to handle fixed debt over 3 to 5 years. Lines of credit prove you can manage liquidity. At Legacy Funding, we look past the red tape. We prioritize your growth metrics over outdated banking formulas. Don't fall into the personal guarantee trap. Traditional banks want your house as collateral; we want your business to thrive. Protect your assets. Build your blueprint. Get Funded. Our approach ensures No Personal Guarantee and No Hard Credit Pull, keeping your personal legacy secure while you scale.

The Decision Matrix: Which Financing Model Fits Your Roadmap?

Choosing between a business line of credit vs term loan isn't just a financial checkbox. It's a strategic move that determines how fast you can scale. You need a blueprint that aligns your capital with your 10-year vision. Follow these five steps to secure the right leverage for your business.

- Step 1: Audit your 12-month cash flow projections. Review your bank statements from the last year. Identify the valleys where revenue dipped. A 2023 U.S. Bank study found that 82% of small businesses fail due to poor cash flow management. Know your numbers to avoid becoming a statistic.

- Step 2: Define the "use of proceeds" with surgical precision. Don't settle for vague goals like "growth." Specify whether you're purchasing $50,000 in seasonal inventory or hiring three new account executives.

- Step 3: Evaluate your current debt-to-income ratio. Traditional institutions often demand a DTI below 36%. Calculate your total monthly debt payments divided by your gross monthly income. This transparency prepares you for the high-level conversation with your lender.

- Step 4: Match the funding speed to the opportunity window. If a competitor is liquidating equipment at a 40% discount this week, a 30-day bank approval process is a liability. Speed is a competitive advantage.

- Step 5: Select a partner that prioritizes your legacy over their ledger. Look for a tech-forward ally that understands the grit of entrepreneurship. You want a consultant, not a bureaucrat.

When to Choose a Line of Credit

Opt for a line of credit when you face erratic revenue cycles or "lumpy" cash flow. It's your financial safety net. Use it to bridge the gap during net-60 invoice factoring cycles or to prepare for unexpected market shifts. You only pay interest on what you draw. This flexibility allows you to pivot instantly without the weight of a full term loan. It's about staying agile in a fast-paced market.

When a Term Loan is the Superior Choice

A term loan is your tool for execution. Choose this model when you have a specific, high-ROI project with a clear end date. If you're financing tangible assets like a new delivery fleet that provides immediate revenue acceleration, the fixed monthly payment offers predictability. It's also the ideal vehicle for consolidating higher-interest debt into one manageable payment. This simplifies your balance sheet and clears the path for generational growth.

Ready to unlock the capital your business deserves? Get Funded today and accelerate your growth blueprint.

Accelerate Your Expansion: Secure Fast Funding with Legacy Advisors

Traditional lenders move at a glacial pace. They demand stacks of paperwork and weeks of your time. Legacy Funding Advisors flips the script. We streamline the approval process to deliver decisions within 24 to 48 hours. This isn't just about speed; it's about seizing opportunities before they vanish. When you're ready to scale, you can't afford to wait on a bank's committee to meet next month.

Deciding on a business line of credit vs term loan requires clarity, not a hit to your credit score. Our "No Hard Credit Pull" approach ensures your score remains protected while you explore your options. You scale your operations without the fear of damaging your financial standing for future growth. We believe your potential shouldn't be capped by a single number on a report.

We offer hybrid strategies that combine the flexibility of lines with the stability of loans. Revenue-based financing serves as our modern alternative to outdated bank hurdles. While big banks rejected approximately 86% of small business loan applications in recent years, we focus on your actual performance. Whether you're weighing a business line of credit vs term loan, our team builds a custom blueprint for your specific industry needs. This model bypasses the 2-year tax return requirement that stops most founders in their tracks. We look at your current bank deposits and growth trajectory instead.

The Legacy Advantage: Speed and Transparency

Our frictionless application process removes the red tape. You won't find endless forms or confusing jargon here. Legacy Funding prioritizes your real-time cash flow over historical credit scores to ensure you get the leverage you need. We provide capital to businesses across the U.S., Canada, and Puerto Rico, ensuring geography never limits your ambition. We focus on where your business is going, not just where it has been.

Your Blueprint for Success

Your journey from application to funding takes less than two days. You need partners who view your company as a generational endeavor, not a line on a spreadsheet. Our advisors act as high-level consultants who are personally invested in your scaling process. We understand that your business represents your family's future and your personal legacy.

Stop waiting for a "maybe" from a local branch. Unlock the capital you deserve and build your empire. Get Funded - Start your application today.

Unlock Your Capital Advantage for 2026

Deciding between a business line of credit vs term loan is the most critical strategic move you'll make this year. Lines of credit provide the revolving agility needed for daily operational pivots. Term loans deliver the structured capital required for massive 2026 expansions. Traditional banks often require 30 to 90 days for approval; we've eliminated that wait. Legacy Funding leverages revenue-based underwriting to focus on your momentum rather than just your history.

Our streamlined system delivers funds in 24 to 48 hours. We protect your score by requiring no hard credit pull for initial offers. This is the modern key to financial freedom. You don't need more red tape; you need a partner who understands the speed of your industry. Stop settling for outdated lending models that slow your progress. Get Funded: Apply for your tailored capital solution in minutes

Your legacy is built on the decisions you make today. Secure the capital you deserve and accelerate your path to scaling. The next chapter of your business starts now.

Frequently Asked Questions

Can I have a business line of credit and a term loan at the same time?

Yes, you can secure both simultaneously to maximize your capital stack. Use a term loan to fund a specific 2024 expansion project while keeping a line of credit ready for seasonal inventory shifts. This dual-funding strategy builds a robust financial blueprint. It ensures you have the leverage to scale and the liquidity to manage daily operations without friction.

Does a business line of credit require a personal guarantee?

Traditional lenders often demand a personal guarantee, but modern alternatives prioritize your business performance. Many fintech platforms now offer funding options with No Personal Guarantee to protect your personal assets. This approach allows you to unlock capital based on your company's 12 month revenue history rather than your home or savings. Secure your legacy without risking your family's future.

How quickly can I get funds from a term loan vs. a line of credit?

You can often access funds from an established line of credit in under 24 hours. Term loans typically require a longer underwriting process, often taking 3 to 7 business days for approval. When comparing a business line of credit vs term loan speed, the line of credit offers immediate agility. Get Funded quickly by choosing the path that matches your current growth velocity.

Which is easier to qualify for with a lower credit score?

Lines of credit are generally more accessible for founders with credit scores in the 600 to 650 range. We often utilize a No Hard Credit Pull process to protect your score while we evaluate your application. Traditional term loans often require a minimum score of 680 according to 2023 SBA data. This focus on revenue rather than just credit helps more entrepreneurs Get Funded and scale.

What is the maximum amount I can borrow with each option?

Term loans typically offer higher maximums, often reaching $5 million for established enterprises. When evaluating a business line of credit vs term loan for large acquisitions, the term loan provides the necessary depth. Credit lines usually cap at $500,000 based on your monthly turnover. Choosing the right amount depends on your specific blueprint for growth and the scale of your next move.

How do these funding options affect my business credit score?

Both funding options can boost your business credit score if the lender reports to bureaus like Dun & Bradstreet or Experian. Timely payments on a term loan demonstrate long term reliability to future creditors. Maintaining a low utilization rate on your line of credit shows disciplined capital management. Consistently meeting these obligations builds a legacy of financial strength that makes future borrowing even easier.

Are there prepayment penalties for paying off a term loan early?

Many traditional term loans include prepayment penalties that cost 1% to 3% of the remaining balance. Lines of credit rarely charge these fees, allowing you to pay down your balance as soon as cash flow permits. Always review your contract to ensure there are no hidden costs. We advocate for transparent terms that let you accelerate your repayment without facing unnecessary financial friction.

What happens if I don’t use the funds in my business line of credit?

You only pay interest on the capital you actually draw from your line of credit. If your balance remains at zero, you typically owe nothing, though some lenders charge a small annual maintenance fee. This makes the line of credit an ideal safety net for your business. It sits ready in the background, allowing you to Get Funded the moment a new opportunity or emergency arises.