Business Line of Credit for Cash Flow Gaps: The Strategic Growth Guide

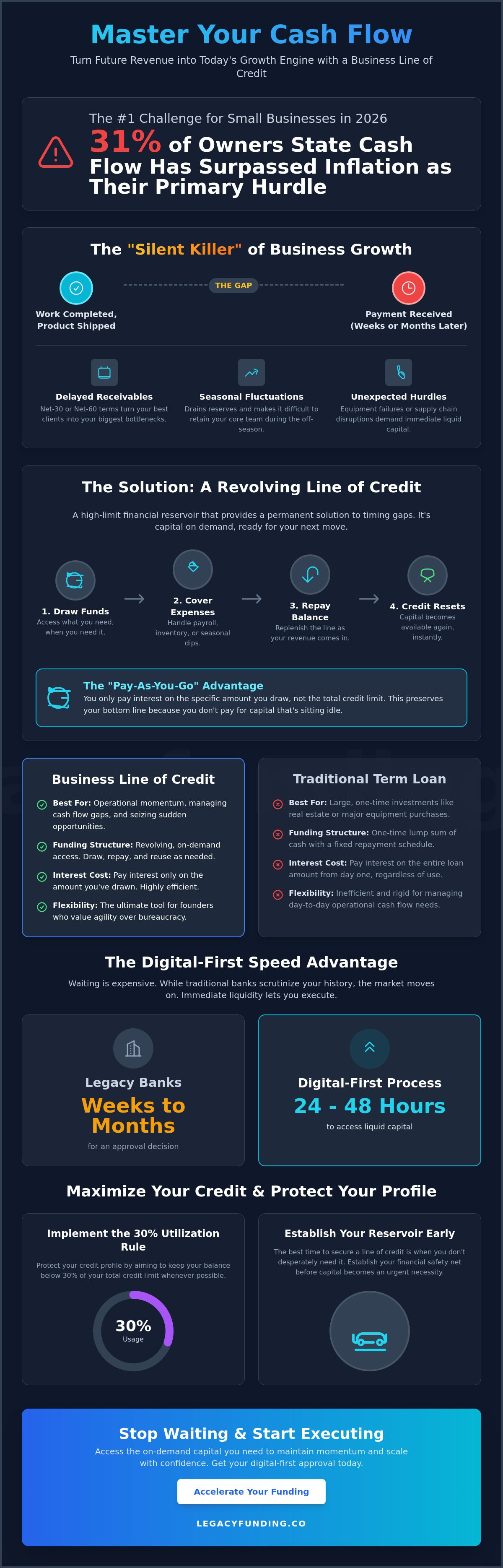

Cash flow has officially surpassed inflation as the primary hurdle for 31% of small business owners in 2026. You've likely felt the friction of waiting weeks for a bank decision while a time-sensitive inventory deal or a critical payroll deadline hangs in the balance. Traditional institutions haven't kept pace with the speed of modern commerce, leaving founders to watch opportunities slip away. Securing a business line of credit for cash flow gaps is no longer just a safety net. It's a strategic move to convert your future receivables into immediate execution power.

We know that inconsistent revenue cycles shouldn't dictate your growth trajectory. You deserve a financial partner that values speed, transparency, and results over bureaucratic red tape. This guide will show you how to master the mechanics of revolving credit to maintain operational momentum and scale with confidence. We'll break down the fast, digital-first approval process, the advantage of paying interest only on what you draw, and the steps to secure on-demand capital. Stop waiting on legacy banks and start fueling your next phase of expansion today.

Key Takeaways

- Neutralize the timing gaps between billing and collection that stall momentum by identifying the "silent killer" of small business growth.

- Master the mechanics of a business line of credit for cash flow gaps to secure on-demand capital that resets as you repay.

- Evaluate how revolving credit stacks up against MCAs and Revenue-Based Financing to find the ideal funding match for your growth stage.

- Protect your credit profile by implementing the 30% utilization rule and establishing your financial reservoir before capital becomes a necessity.

- Accelerate your funding timeline with a digital-first approval process designed to deliver liquid capital in as little as 24-48 hours.

Bridging the Gap: Why Cash Flow Inconsistency Stalls Growth

Cash flow isn't just a financial metric. It's the heartbeat of your operation. When that pulse falters, growth stops. The timing gap between billing and collection acts as a silent killer for small and medium businesses. You've delivered the service. You've shipped the product. Yet, your capital remains locked in your client's accounts while your own bills come due. This friction creates a ceiling on your potential, forcing you to play defense when you should be attacking the market.

Strategic founders don't view borrowing as a sign of weakness. They see it as a tool for momentum. There is a fundamental difference between "bad debt" used to bail out a failing model and "strategic credit" used to accelerate a winning one. A business line of credit provides the dry powder necessary to maintain speed. It transforms your future receivables into immediate execution power, ensuring that a temporary dip in liquidity doesn't become a permanent stall in progress.

The Anatomy of a Cash Flow Gap

Most cash flow crises aren't caused by a lack of sales. They're caused by the calendar. Delayed accounts receivable often turn your best clients into your biggest bottlenecks. If you're operating on Net-30 or Net-60 terms, you're essentially acting as a zero-interest bank for your customers. Seasonal fluctuations can also drain reserves, making it difficult to retain your core team during the off-season. When you add unexpected operational hurdles like equipment failure or supply chain disruptions, the need for a business line of credit for cash flow gaps becomes undeniable. It's about maintaining a baseline of stability so you can focus on the big picture.

The Opportunity Cost of Waiting

Waiting is expensive. While traditional banks spend weeks or months scrutinizing your history, the market moves on. The interest on a line of credit is often negligible compared to the cost of a missed opportunity. Immediate liquidity allows you to pull the trigger on bulk-purchase discounts from suppliers, instantly increasing your margins. It gives you the leverage to secure top-tier talent when your competitors are frozen by cash constraints. By utilizing a business line of credit for cash flow gaps, you stay agile. You aren't just surviving the gap; you're using it as a launchpad. Don't let a temporary lack of liquid capital dictate the long-term trajectory of your brand. Execution requires capital on demand, not capital on a delay.

The Mechanics of a Business Line of Credit for Cash Flow Gaps

A business line of credit for cash flow gaps operates like a high-limit financial reservoir. Unlike a traditional loan, it's a revolving credit facility with a pre-approved limit. You draw what you need. You repay the balance. The capital becomes available again instantly. It's a cycle of liquidity that mirrors the fast-paced nature of modern commerce. This structure provides a permanent solution to the timing gaps between your outgoing expenses and incoming revenue. It's the ultimate tool for founders who value agility over bureaucracy.

The system relies on two distinct phases: the draw period and the repayment period. During the draw period, you access funds as needed to cover payroll, purchase inventory, or bridge a seasonal dip. You only pay interest on the specific amount you draw, not the total credit limit. This "pay-as-you-go" interest model is a Smart Choice for Your Business because it preserves your bottom line. You don't pay for capital that's sitting idle. Once you repay the principal, your available credit resets. It's capital on demand, ready for your next move.

Revolving Credit vs. Traditional Term Loans

Term loans provide a lump sum of cash. You pay interest on the entire amount from day one, regardless of how much you actually spend. That's inefficient for managing a business line of credit for cash flow gaps. Revolving credit offers on-demand access that adapts to your daily needs. While term loans are better for large, one-time investments like real estate, lines of credit excel at operational momentum. Watch for commitment fees or annual maintenance costs in the fine print. Most annual fees stay under $200, making this a cost-effective way to keep "dry powder" in your accounts. The flexibility far outweighs the minimal overhead.

Secured vs. Unsecured Lines: Choosing Your Risk Level

Unsecured lines of credit offer high-speed access without pledging specific business assets. They're built for speed and accessibility, typically featuring APRs between 12% and 18% for top-tier online lenders. Secured lines require collateral, such as accounts receivable or inventory, to unlock higher limits and lower rates. Bank-secured lines currently range from 8% to 11% APR, but they involve rigorous appraisal processes. Legacy Funding Advisors prioritizes your real-time cash flow and growth metrics over heavy collateral requirements. We understand that your momentum is your greatest asset. If you're ready to secure a flexible reservoir of capital, explore your funding options with a partner who speaks the language of growth.

Strategic Comparison: Line of Credit vs. Other Funding Solutions

Choosing capital is like choosing a precision tool. The wrong instrument leads to wasted resources and slowed momentum. While a business line of credit for cash flow gaps is the most flexible option for daily operations, you must understand the competitive landscape. Every funding vehicle serves a specific strategic purpose. Your goal is to match the capital's cost and structure to the specific revenue event you're funding. Don't settle for the most accessible cash. Demand the most effective cash.

Consider the broader market data. In fiscal year 2023, the SBA approved over $27 billion in 7(a) loans. These are excellent for long-term stability, such as purchasing real estate or large-scale machinery. However, the barrier to entry is high. The minimum SBSS score for smaller 7(a) loans rose to 165 in March 2026. For immediate operational friction, alternative lenders offer approval rates between 26% and 33%, far outpacing large banks. This speed makes revolving credit the superior choice for managing a business line of credit for cash flow gaps when time is your most expensive asset.

When a Line of Credit Beats an MCA

Merchant Cash Advances (MCAs) are often the first choice for businesses in a panic. They offer extreme speed, but that speed comes with a high price tag. MCAs deduct a fixed percentage of your daily sales. This can suffocate your cash flow during a slow week. A line of credit provides a predictable repayment schedule. It offers a lower overall cost of capital for businesses with consistent but gapped revenue. More importantly, it builds a permanent credit relationship. You don't have to re-apply every time you need a draw. You have a reservoir, not a one-off advance.

Revenue-Based Financing: The High-Growth Alternative

Revenue-Based Financing (RBF) is the strategic choice for high-growth startups. Unlike fixed credit lines, RBF scales with your success. It allows you to access millions in growth capital without surrendering equity. The payments fluctuate based on your monthly revenue, providing a natural cushion during lean months. A savvy founder uses a hybrid approach. Utilize a business line of credit for cash flow gaps to handle payroll and inventory. Then, deploy RBF for massive expansion, such as a national marketing blitz or entering a new territory. This strategy preserves your ownership while fueling your trajectory. Pick the tool that fits your timeline and your ambition.

Maximizing Your Credit Line: 5 Rules to Avoid a Cash Crunch

Managing a business line of credit for cash flow gaps requires more than just access. It requires a playbook. You've already seen how these facilities function and how they outpace traditional term loans in flexibility. Now, you must master the execution. Strategic borrowing isn't about filling a hole. It's about building a bridge to your next revenue milestone. Use these five rules to turn your credit line into a permanent competitive advantage.

- Rule 1: Establish the line before you need it. Don't wait for a crisis to apply. Lenders prioritize businesses that show strength, not desperation. Secure your facility while your cash flow is healthy to ensure the best terms.

- Rule 2: Monitor the 30% utilization threshold. Discipline is your best asset. Keeping your balance below 30% of your total limit protects your credit profile and ensures you always have "dry powder" for emergencies.

- Rule 3: Time your draws with high-probability receivables. Match your borrowing to your 30-day outlook. Draw funds when you have a confirmed invoice arriving soon to ensure a swift repayment cycle.

- Rule 4: Use credit for ROI-generating activities. Don't use your line just to "stay afloat." Direct the capital toward bulk inventory discounts, talent acquisition, or equipment that increases your production capacity.

- Rule 5: Automate your repayments. Build a "trust bridge" with your lender. Setting up automated payments eliminates human error and proves your reliability, often leading to limit increases over time.

The 30% Utilization Strategy

Maxing out your credit line is a red flag for future borrowing power. It suggests your business is surviving on credit rather than using it for momentum. Aim to keep your utilization under 30%. This discipline protects your credit profile and signals financial health to future investors and traditional banks. Use the line as a temporary bridge for specific operational hurdles. Don't let it become a permanent floor for your daily expenses. By maintaining a low balance, you stay ready for sudden, high-value opportunities that your competitors can't afford to chase.

Forecasting for Smarter Draws

Precision in forecasting leads to efficiency in funding. Look at your 30-day revenue outlook before you touch your credit line. If you know a major client payment is arriving in three weeks, that's the perfect time to draw for inventory or payroll. You'll bridge the gap and pay down the principal quickly, which minimizes your interest costs. Avoid the "interest trap" by paying down the balance during your peak revenue weeks. Use centralized financial tools to track every dollar of credit spent. When you treat your business line of credit for cash flow gaps as a surgical tool, you maximize growth while minimizing debt. Ready to build your strategic reservoir? Secure your business line of credit and start scaling on your own terms.

Accelerate Your Capital: Accessing a Line of Credit with Legacy Funding Advisors

Traditional banking is failing the modern founder. Legacy institutions have reported stricter lending criteria for 13 consecutive quarters, creating a massive barrier for growing firms. They focus on where your business was five years ago. We focus on your current trajectory. Legacy Funding Advisors acts as the modern alternative, replacing slow committees with a tech-forward approach. When you're managing a business line of credit for cash flow gaps, you need a partner that moves at the speed of your sales cycle. We've eliminated the friction to ensure your growth remains uninterrupted.

Our underwriting is fundamentally different because it's cash-flow-centric. Your real-time performance matters more than a static credit score. We analyze your revenue metrics and receivables to unlock capital that legacy banks often overlook. Statistics show that over 76% of small businesses now bypass traditional banks in favor of alternative lenders. They do this for one primary reason: speed. We provide a 24-48 hour approval and funding window. This allows you to bridge immediate gaps before they turn into missed opportunities. You've built the momentum. We provide the fuel.

The Legacy Advantage: Speed and Transparency

We've stripped away the bureaucratic hurdles that define old-world finance. Our streamlined digital application process means no more endless paperwork or weeks of silence. We offer tailored solutions for diverse industries, from high-volume retail to complex manufacturing. You'll work with dedicated advisors who understand the specific struggle of scaling a brand. We don't just offer a transaction; we offer a partnership designed for long-term impact. You get the clarity you need to make bold moves without second-guessing your liquid reserves.

How to Get Started Today

Securing your financial reservoir shouldn't be a second job. We've simplified the path to capital into three actionable steps. You can start the process right now and have a decision in hours, not weeks. Follow this roadmap to secure your business line of credit for cash flow gaps:

- Step 1: Complete our simple online application. It takes minutes and requires only minimal documentation to get started.

- Step 2: Receive a rapid review of your business cash flow. We look at your revenue metrics to determine a limit that empowers your growth.

- Step 3: Gain immediate access to your funds. Once approved, your credit line is ready to bridge your next gap or fuel your next expansion.

Stop letting the calendar control your company's future. Secure your business line of credit with Legacy Funding Advisors now and take command of your operational momentum. Don't wait for the next revenue dip to realize you need a safety net. Build your strategic bridge today and focus on the metrics that actually matter: your growth, your team, and your legacy.

Command Your Growth and Secure Your Legacy

You've mastered the strategy. You now understand that a business line of credit for cash flow gaps is the ultimate tool for maintaining operational velocity. By establishing your credit reservoir before the need arises and maintaining strict utilization discipline, you ensure that timing gaps never dictate your trajectory. You've seen how revolving credit outpaces traditional term loans and MCAs in both flexibility and long-term cost efficiency. Execution requires capital on demand; don't settle for anything less.

Legacy Funding Advisors is ready to act as your strategic ally. We've deployed over $500M in capital to founders who value execution over bureaucracy. We prioritize your real-time cash flow performance rather than just a static credit score. Access the liquid capital you need with a funding window as fast as 24-48 hours. Stop watching growth opportunities slip away because your capital is locked in receivables. You have the vision, and we provide the fuel to reach it.

Apply for a Business Line of Credit in 24 Hours and take the first step toward total financial agility. Your next phase of expansion starts with a partner who understands the speed of your ambition.

Frequently Asked Questions

How quickly can I access funds from a business line of credit?

You can often access funds within 24 to 48 hours when working with modern digital lenders. Unlike traditional banks that take weeks for approval, alternative platforms prioritize speed and efficiency. Once your facility is established, drawing capital is nearly instantaneous. This rapid access is essential for managing a business line of credit for cash flow gaps during time-sensitive growth opportunities.

Will a business line of credit help if I have a low credit score?

Yes, because many modern lenders prioritize your real-time cash flow and revenue metrics over a static personal credit score. While traditional institutions have reported stricter lending criteria for 13 consecutive quarters, alternative providers use data-driven underwriting to evaluate your business's current health. If your revenue is strong and consistent, you can often secure a line despite a less-than-perfect score.

What is the difference between a secured and unsecured line of credit?

A secured line requires you to pledge specific business assets, such as inventory or accounts receivable, as collateral for the lender. This often results in lower interest rates. An unsecured line requires no specific collateral, offering faster access and lower risk to your assets. Unsecured options typically feature higher APRs, ranging from 12% to 22% depending on your business's specific financial profile.

How much can I borrow through a business line of credit for cash flow gaps?

Borrowing limits are typically determined by your average monthly revenue and overall financial health. Most lenders offer credit lines ranging from $10,000 to $250,000 or more for qualified businesses. The specific amount you receive depends on your ability to demonstrate consistent cash flow and a clear capacity for repayment. Your limit can often increase as you build a positive repayment history with your lender.

Are there fees for having a line of credit even if I don’t use it?

You may encounter minimal maintenance or annual fees, though many modern lenders waive these to remain competitive. Annual fees are typically under $200. You only pay interest on the specific amount you draw from the line. This makes it a cost-effective safety net for any operation. Always review the terms for draw fees or origination costs, which usually range from 0% to 3%.

Can I use a business line of credit to pay off other high-interest debt?

You can use these funds for debt consolidation, though it's most effective when the line's APR is significantly lower than your existing debt. This strategy can simplify your monthly obligations and improve your daily cash flow. However, the primary purpose of this capital is usually to fuel growth or bridge operational gaps. Ensure the move aligns with your long-term scaling strategy before committing.

What documents do I need to apply for a business line of credit?

Digital-first lenders typically require minimal documentation, such as recent business bank statements and basic tax information. You won't face the mountain of paperwork required by legacy banks. Most applications can be completed online in minutes. Lenders primarily look for proof of consistent revenue and at least six months to a year of operational history to verify your business's stability and growth potential.

How does a line of credit affect my business credit score?

A line of credit can improve your business credit score if you maintain low utilization and make consistent, on-time payments. Lenders report your activity to credit bureaus, building your profile for future, larger-scale financing. Conversely, maxing out your limit or missing deadlines can hurt your score. Keeping your utilization below the 30% threshold is a proven way to signal financial health to future investors.