Business Debt Consolidation Loan for Small Business: The 2026 Tactical Guide

Business debt consolidation is a strategic recapitalization of your company's future, not a confession of financial defeat. If you're watching your operational cash flow vanish into a relentless cycle of daily ACH withdrawals, securing a business debt consolidation loan for small business is your primary tool for reclaiming control. You likely feel the constant pressure of UCC-1 liens and the disruption of aggressive collection calls. It's a common struggle for modern founders who expanded quickly but now find their growth stalled by high-interest obligations. You want to stop the bleeding and regain control of your balance sheet.

By reading this guide, you'll learn how to eliminate daily cash flow drains, protect your personal assets, and pivot your operations toward sustainable scaling. We'll break down the 2026 tactical landscape, covering everything from SBA 7(a) rate benchmarks to the specific mechanics of folding multiple high-cost liabilities into a single, manageable monthly payment. It's time to stop managing debt and start managing your legacy. Move forward with the confidence of a partner who understands the speed of your business.

Key Takeaways

- Conduct a full audit of your current debt stack to identify which lenders hold the most leverage and calculate your true debt service capacity.

- Evaluate the strategic differences between traditional consolidation and reverse consolidation to protect your business credit score and future fundability.

- Secure a business debt consolidation loan for small business to replace high-frequency daily withdrawals with a single, predictable payment structure.

- Execute a proactive five-step plan that includes auditing lender compliance and requesting strategic forbearance to stabilize your cash flow.

- Shift your company from survival mode to growth mode by implementing a 90-day cash flow monitoring protocol to prevent future debt accumulation.

The Reality of a Business Debt Consolidation Loan for Small Business in 2026

In 2026, the financial landscape has shifted. The global market for business debt restructuring is projected to hit $52.3 billion this year. This growth isn't driven by desperation; it's fueled by tactical intelligence. A business debt consolidation loan for small business is the strategic merging of multiple high-frequency liabilities into a single, efficient facility. It moves you from defensive survival to offensive growth. Traditional lenders often fixate on APR, but modern founders know better. They prioritize cash flow velocity over minor interest fluctuations. Use this tool to prevent technical insolvency before it begins. It is a proactive recapitalization of your company's balance sheet.

Why Business Debt Differs from Consumer Debt

Business debt carries weight that personal loans never touch. Most alternative lenders secure their positions through the Uniform Commercial Code (UCC). A UCC-1 lien effectively freezes your business assets, claiming rights to your equipment, inventory, and future revenue. Many of these agreements also require a personal guarantee, placing your home and personal savings on the line. While consumer lenders look at credit scores, business lenders prioritize your debt service coverage ratio. They want to see that your operations generate enough cash to breathe, not just to pay back a principal. Secure your assets by using debt consolidation to clear these encumbrances and restore your operational freedom.

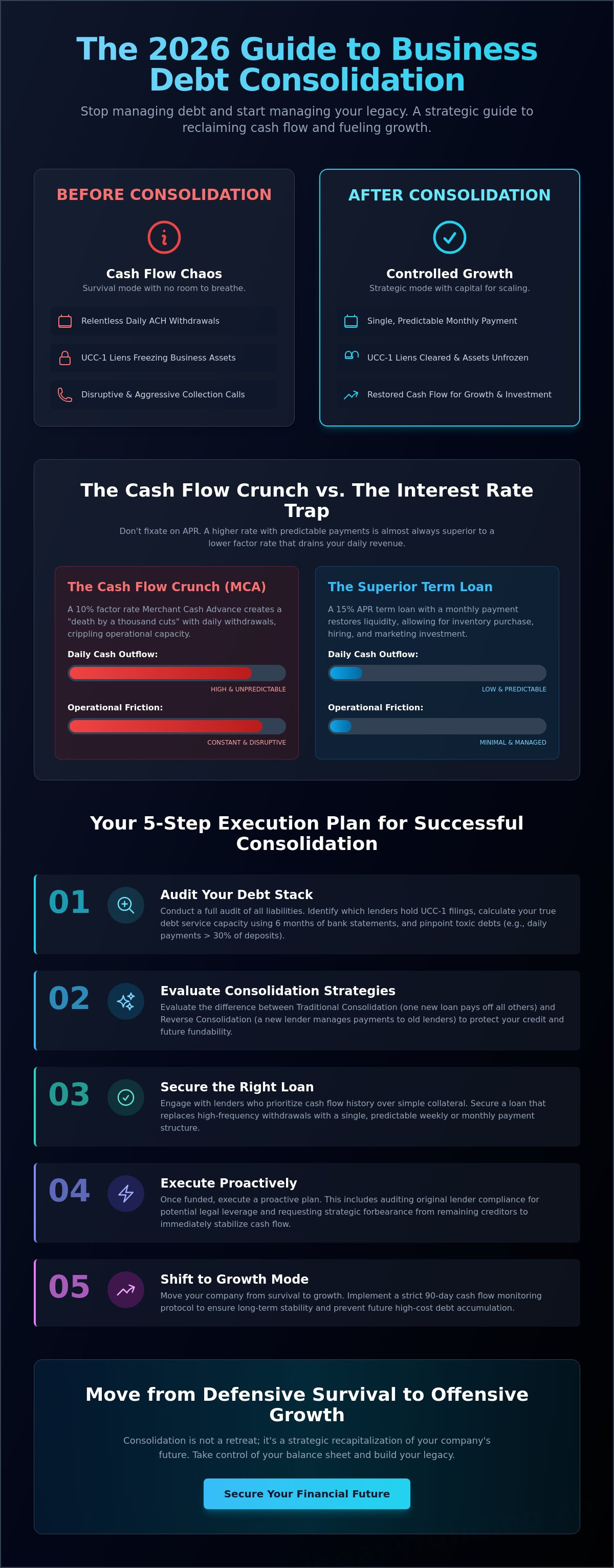

The 'Cash Flow Crunch' vs. The 'Interest Rate Trap'

Don't fall for the interest rate trap. A 15% APR term loan is almost always superior to a 10% factor rate Merchant Cash Advance (MCA) that drains your bank account every morning. Daily ACH withdrawals create a "death by a thousand cuts" scenario. This constant friction leads to payment fatigue, where you spend more time managing bank balances than managing your team. Consolidating these debts unencumbers your daily revenue. By moving to a weekly or monthly schedule, you regain the liquid capital needed to buy inventory, hire talent, and invest in marketing. You aren't just lowering a rate; you're buying back your business's future. This pivot allows you to implement a strict 90-day cash flow monitoring protocol to ensure long-term stability.

Building Your Leverage: The Financial Deep Dive Before You Consolidate

Audit your debt stack with clinical precision. You cannot fix what you haven't measured. Group every liability by its daily impact on your bank balance. Identify which lenders hold UCC-1 filings and who sits in the first position. This hierarchy determines your negotiation power. Gather six months of bank statements to calculate your true debt service capacity. This data is the foundation of any successful business debt consolidation loan for small business. It proves to new lenders that your core operations are healthy, even if your current debt structure is not. Executing a business debt consolidation loan for small business requires more than just an application; it requires a tactical strategy.

Identify toxic debt immediately. These are typically Merchant Cash Advances with factor rates that translate into high effective APRs. If your daily payments exceed 30% of your average daily deposits, you're in the danger zone. Determine your walk-away point. If consolidation doesn't lower your daily cash outflow by at least 40%, debt settlement might be the more aggressive, necessary path. When reviewing the Best business debt consolidation loans, notice how top-tier lenders prioritize your cash flow history over simple collateral value.

Identifying High-Risk Lenders in Your Stack

Differentiate between your secured bank loans and unsecured alternative funding. Rank your creditors by their ability to disrupt your daily business operations. A lender with a lockbox on your credit card processing is higher risk than one with a general lien. Understand the first-position advantage. The lender who filed their UCC-1 first often dictates terms to everyone else. If your stack feels unmanageable, it's time to speak with a tactical advisor to map your exit strategy.

Calculating Your Net Repayment Ability

Determine your unencumbered cash flow. This is the capital remaining after every vital operating expense is paid. Lenders use Net Present Value logic to evaluate your risk. They want to see that the future value of your revenue exceeds the cost of the new facility. With the U.S. Prime Rate at 6.75% as of May 2026, benchmark your expectations against current market reality. Aim for SBA 7(a) rates between 10.5% and 13% if you have the collateral to back it. Identify equipment or real estate that can be pledged to secure these better terms. This shift preserves your ownership and restores your focus on growth metrics.

Consolidation vs. Reverse Consolidation: Choosing Your Strategy

Choosing the right path requires a clear-eyed assessment of your current liquidity and long-term scaling goals. A traditional business debt consolidation loan for small business is a new, larger facility used to pay off existing creditors in full. It is an excellent move for businesses with strong credit and the patience to wait for traditional underwriting. However, many founders find themselves in a position where they cannot qualify for a new loan because their current debt stack is too heavy. In these high-stakes scenarios, reverse consolidation serves as a specialized lifeline. It focuses on immediate cash flow relief without the need for a massive new principal amount. This strategy keeps your operations running while you work toward a cleaner balance sheet.

The Power of Reverse Consolidation

Think of reverse consolidation as a tactical payment management system. Instead of you scrambling to meet multiple daily ACH withdrawals, a provider covers those daily payments for you. You then make a single, manageable weekly payment back to the provider. This mechanism stops the daily bank balance anxiety instantly. It simplifies chaotic accounting and allows you to focus on growth metrics rather than survival. This specialized service is a core expertise of Legacy Funding Advisors. It is designed for businesses that need to unencumber their cash flow today but want to avoid the credit damage associated with a default or settlement. You retain your assets and your dignity while regaining your operational momentum.

Traditional Consolidation: Pros and Cons

Traditional restructuring offers a clear path to rebuilding your long-term fundability and establishing a stronger credit profile. If you qualify for the SBA 7(a) loan program, you can consolidate your debt into a facility with terms extending up to ten years. This approach is superior for preserving your credit score and avoiding the 'scorched earth' reputation that follows debt settlement. Be mindful of the tax implications. Debt forgiveness often triggers a 1099-C, meaning the IRS treats forgiven debt as taxable income. A business debt consolidation loan for small business avoids this trap by ensuring every dollar is accounted for and repaid over a longer, more sustainable timeline. With the U.S. Prime Rate at 6.75% as of May 2026, securing a fixed-rate 7(a) loan can lock in stability for a decade. Choose traditional consolidation if your debt-to-income ratio allows for new credit; choose reverse consolidation if you need to stop the daily cash flow drain immediately without sacrificing your business reputation.

The 5-Step Execution Plan for a Successful Consolidation

Execution is where strategy meets reality. Successfully securing a business debt consolidation loan for small business requires a systematic approach to negotiation. You aren't just applying for a new facility; you're orchestrating a multi-party settlement that clears your balance sheet and restores your focus. Move with speed but maintain clinical attention to detail. Every agreement must be in writing before a single dollar of the new loan is disbursed. This is the only way to ensure that your previous liabilities are truly extinguished and your assets are protected from future claims.

Step 1: The Pre-Default Outreach Strategy

Initiate proactive outreach to your current lenders before you miss a payment. Draft a professional email directed to the Special Assets or Workout department. These teams are empowered to make decisions that standard customer service representatives cannot. Explain your cash flow crunch as a temporary operational hurdle, not a sign of unviability. Request a fourteen-day pause on ACH withdrawals to allow for the consolidation process to finalize. This creates the breathing room you need to secure your new funding without the constant drain on your daily deposits.

Step 2: Negotiating the Payoff Letter

A payoff letter is non-negotiable. It is legally distinct from a simple balance statement. This document must state the exact amount required to close the account, including any accrued interest, and must provide a clear "good through" date. Audit this letter for aggressive prepayment penalties or hidden "junk fees." If your original agreement allows for a discount on early repayment, insist that it's reflected in the final number. Ensure the letter includes a Release of Liability clause. This prevents lenders from pursuing you later for servicing fees or disputed interest amounts.

Step 3: Closing and UCC-1 Termination

Direct disbursement is the gold standard for closing. Your new lender should wire funds directly to the old creditors to ensure the chain of custody remains clean. Never take the funds into your own account to pay them manually; this can lead to accounting errors and delayed lien releases. After forty-eight hours, verify the status of your UCC-1 filings via your Secretary of State portal. In 2026, most states offer instant digital verification. Confirm that all liens are marked as terminated. Finally, monitor your business credit report to ensure it reflects the "paid in full" status for every consolidated account.

Regaining your financial independence starts with a clear plan and the right partner. If you're ready to unencumber your revenue and move toward sustainable growth, contact our tactical advisors today to begin your debt stack audit.

Beyond Debt: Securing Your Business's Financial Future

Survival mode ends the moment your previous liens are cleared. Successfully closing a business debt consolidation loan for small business marks the end of your financial defense. Now, you must pivot to offense. Implement a strict 90-day cash flow monitoring protocol immediately. This isn't just about tracking expenses; it's about identifying growth velocity. Watch your debt service coverage ratio with clinical intensity. Your goal is to move from alternative rates to prime bank rates within 12 to 24 months. With the U.S. Prime Rate currently at 6.75%, the reward for a clean balance sheet is significant. You're no longer just paying for the past; you're investing in your legacy.

Rebuild your business credit through low-risk, strategic financing. Use the breathing room created by your consolidation to boost your personal credit score toward the 720 threshold. This opens the door to conventional bank loans and the most competitive SBA products. In the 2026 market, lenders reward transparency and consistent revenue performance. Position your business to qualify for prime lending rates by maintaining a clean debt-to-income ratio. This transition is not a simple transaction. It is a generational endeavor that secures your company's role in the modern economy.

Choosing the Right Growth Partner

Traditional banks often lack the speed required for modern commerce. They operate on legacy timelines that don't match your growth goals. Contrast these rigid institutions with flexible, tech-forward allies like Legacy Funding. We understand that your business needs capital that adapts to your revenue cycles. Revenue-based financing is often safer for cash-flow-sensitive businesses than traditional term loans because it scales with your actual performance. It prevents the rigid payment fatigue that led to your initial debt stack. Ready to restore your cash flow? Contact Legacy Funding Advisors for a Consultation.

Maintaining a Clean UCC Record

Protect your first-position status at all costs. This is the key to future SBA or bank lending. A clean UCC record proves to high-level lenders that you are a low-risk partner. Audit your own business credit report every quarter for errors or outdated filings. If a lien from a satisfied business debt consolidation loan for small business still appears, demand its removal immediately. Transparency builds trust with future investors and creditors. By maintaining a pristine financial record, you ensure your business remains fundable, scalable, and resilient for years to come. Move forward with the confidence of a founder who has mastered their capital structure.

Take Command of Your Capital Structure

You now have the tactical roadmap to dismantle your debt stack and reclaim your operational freedom. By prioritizing cash flow velocity and executing a precise five-step plan, you move from defensive survival to a position of strategic leverage. Securing a business debt consolidation loan for small business is the most effective way to unencumber your revenue and protect your personal assets from aggressive collections. Don't let daily withdrawals dictate your company's potential or stall your long-term scaling goals.

Legacy Funding Advisors provides specialized solutions for businesses currently managing UCC liens or complex MCA debt. We focus on your growth metrics and future capacity, not just outdated credit scores. Our team understands the speed of modern commerce. With funding approvals possible in as little as 24 to 48 hours, you can stabilize your bank balance and start funding your next expansion phase immediately. Apply for Fast, Flexible Business Funding Today and restore your focus to what matters most. Your legacy is built on the tactical decisions you make today. Build it on a foundation of financial strength.

Frequently Asked Questions

Can I get a business debt consolidation loan with bad credit?

You can secure a business debt consolidation loan for small business even if your personal credit score is below 680. While traditional banks and SBA lenders often require scores of 720 or higher, alternative lenders focus on your daily revenue and cash flow health. In these scenarios, a reverse consolidation may be the most effective path to stop daily cash flow drains without needing a high credit benchmark. Focus on your growth metrics to prove viability.

How does a reverse consolidation work compared to a traditional loan?

A reverse consolidation provides immediate cash flow relief by covering your existing daily payments for you. Unlike a traditional loan that issues a new principal to pay off old creditors, this strategy consolidates various daily withdrawals into a single, manageable weekly payment. It's a tactical management tool designed for businesses that need to unencumber their revenue today but don't yet qualify for a massive term loan. It keeps your operations running while you rebuild.

Will consolidating my business debt affect my personal credit score?

Consolidating your business debt generally has a positive long-term impact on your personal credit score. By replacing high-interest, short-term liabilities with a structured facility, you reduce the risk of missed payments and defaults that trigger personal guarantee clauses. While the initial application might cause a minor hard inquiry dip, the resulting reduction in credit utilization and improved payment history will strengthen your overall financial profile. It's a strategic move for your generational legacy.

Can I consolidate Merchant Cash Advances (MCAs) into a single payment?

You can absolutely fold multiple Merchant Cash Advances into one manageable facility. This process stops the "death by a thousand cuts" caused by competing daily ACH withdrawals. By using a business debt consolidation loan for small business, you replace chaotic, high-frequency debits with a predictable weekly or monthly schedule. This shift allows you to reclaim your operational cash flow and reinvest in talent or inventory rather than just servicing factor rates.

What is a UCC-1 lien and how do I get it removed after consolidation?

A UCC-1 lien is a legal notice filed by lenders to claim a security interest in your business assets. To get it removed, your previous lender must file a UCC-3 termination statement once their debt is satisfied through consolidation. Always verify this filing through your Secretary of State portal within 48 hours of the payoff. Ensuring these liens are cleared is vital for maintaining your first-position status for future prime lending opportunities and SBA programs.

Is it better to settle business debt or consolidate it?

Consolidation is superior for founders who want to preserve their business credit and maintain professional relationships with lenders. Debt settlement is a "scorched earth" tactic that involves defaulting on payments to force a discount, which can damage your fundability for years. Consolidation allows you to restructure your obligations into a sustainable payment plan without the long-term stigma or tax implications of a 1099-C debt forgiveness form. Choose the path that supports long-term scaling.

How much of a discount can I expect when consolidating multiple loans?

Your primary savings come from the elimination of future interest and the reduction of daily payment friction. While some lenders offer a "payoff discount" for early retirement of the principal, the true value lies in the lower total cost of capital over time. By moving from daily factor rates to a structured term loan or line of credit, you significantly increase your net repayment ability and unencumber your revenue for immediate scaling and operational efficiency.

What documents do I need for a business debt consolidation loan application?

You need to provide a minimum of six months of recent business bank statements and your most recent two years of federal tax returns. Lenders also require a detailed debt schedule that lists every current creditor, their daily payment amounts, and outstanding balances. Having payoff letters ready for your toxic debt will accelerate the approval process. This preparation often leads to a final decision within 24 to 48 hours, allowing you to pivot quickly.